Gemini Space Station Narrows International Focus to Strengthen U.S. Core Crypto Platform

Gemini’s latest quarter highlights strategic market exit and innovation efforts balancing competitive and regulatory pressures.

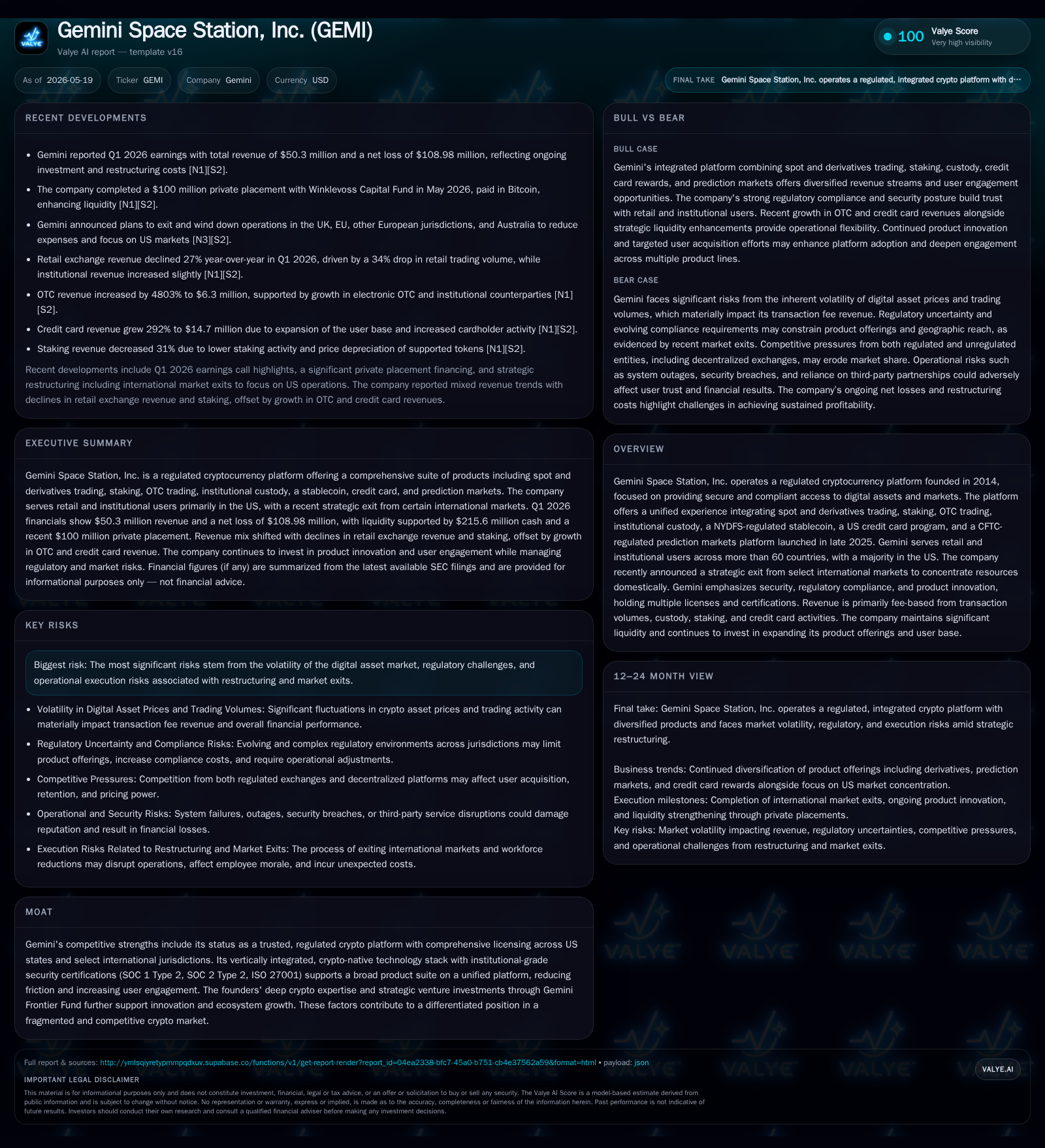

In Q1 2026, Gemini Space Station, Inc. reported revenue growth driven by its integrated cryptocurrency platform while continuing to face net losses amid industry volatility and restructuring costs. The company is executing a significant strategic pivot by exiting select international markets to concentrate on its U.S.-centric product suite including spot and derivatives trading, staking, custody, and a newly launched prediction markets platform. Gemini’s business model relies heavily on transaction fees from a diversified retail and institutional user base supported by comprehensive regulatory licenses and a vertically integrated technology stack. Key growth drivers include product innovation like event contracts and enhanced wallet solutions, while risks center on digital asset price volatility, evolving regulation, and competitive pressures from unregulated platforms. Financially, the firm maintains healthy liquidity and continues to invest in expanding assets and infrastructure with a focus on user experience and compliance.

Recent Operating Update

Gemini Space Station delivered its latest quarterly filing on May 15, 2026 ([S2]) revealing key operating metrics: total revenue rose sharply to $50.3 million for Q1 2026 compared to $35.3 million a year earlier. However, net loss remained significant at $109 million despite narrowing from prior periods due partly to restructuring costs associated with Gemini’s February decision to exit multiple international markets such as the United Kingdom, EU jurisdictions, and Australia ([S12]). This strategic retreat aims to consolidate resources toward strengthening its domestic U.S. operations where the company holds full licensing coverage enabling direct fiat banking rail access ([S1], [S2]).

Capital-wise, Gemini augmented its liquidity profile with a private placement announced on May 14 that raised $100 million through issuance of Class A shares at $14 per share to Winklevoss Capital Fund ([S3]), adding financial flexibility for further investment in product innovation and operational scaling.

Management acknowledges rising competitive pressures from both regulated players and alternative channels such as decentralized exchanges (DEXs) or DAOs that could erode fee structures ([S27]). To offset margin compression risks, the company emphasizes continuous innovation backed by a strong brand reputation as a trusted platform grounded in compliance ([S2],).

Business Model

Gemini operates primarily as an integrated cryptocurrency platform providing secure access to digital assets across retail and institutional clients worldwide. Revenue generation hinges mainly on fee-based income derived from transaction volumes on its spot and derivatives exchanges including OTC desk trades; these contributed over half of total revenues in recent years ([S1]). Customer segments break down roughly into retail users—accounting for approximately 91% of exchange fees—and institutions using advanced custody and sophisticated trading capabilities ([S1], [S2]).

Additional fee streams emerge from staking services offering yield products compliant with evolving regulations; wallet services; credit card programs tied to interchange fee revenues; withdrawal fees; advisory services; as well as the recently introduced prediction markets platform governed under CFTC licensed entity Gemini Titan LLC ([S1], [S2]).

Particularly noteworthy is the vertically integrated technology infrastructure underpinning the platform that reduces friction between products by sharing infrastructure across money (stablecoins like GUSD) and diverse market offerings (derivatives, predictions), facilitating cross-product user engagement which enhances retention and monetization potential (, [S10]).

Marginal profitability faces pressure due to intensifying competition as fee discounting proliferates among crypto exchanges amid market maturation ([S27]). Yet trust based on comprehensive licensing (including NYDFS stablecoin regulations) alongside institutional-grade security certifications (SOC1/2 Type 2, ISO27001) strengthens switching costs for higher-end clients seeking compliance certainty ().

Industry Structure and Competitive Position

The crypto exchange sector remains fragmented characterized by both regulated centralized platforms like Gemini vying for depositors’ trust vis-à-vis decentralized protocols facilitating peer-to-peer trades without intermediaries. Market entrants must navigate an evolving regulatory labyrinth compounded by cross-jurisdictional complexities affecting product availability ([S4], ).

Gemini’s competitive moat arises from its dual emphasis on rigorous compliance—holding required money transmitter licenses or equivalents across all U.S. states—and broad product breadth spanning spot trading through innovative derivatives including prediction markets lately launched in late 2025 (, [S12]). This positions Gemini strategically against newer entrants who may lack licensing depth or “fiat-on/off ramps” reliability critical for mainstream adoption.

Institutional-grade custody solutions further differentiate Gemini versus retail-focused venues lacking trust or insurance mechanisms necessary for large fund managers (). However, unregulated alternatives often undercut pricing or rapidly innovate functional features like liquidity bootstrapping or low-fee margin trading creating ongoing competitive challenges ([S27]).

Growth Drivers

Product Innovation & Market Expansion

Gemini’s roadmap centers on diversifying assets available for trading (including expanded tokens suitable for staking) alongside developing richer user engagement tools such as next-generation secure wallets acting as gateways into the blockchain ecosystem ([S6],[S10]). The deployment of Gemini Predictions™ introduces event contract trading reflecting expanded outcome-based derivatives beyond typical crypto price movements—a novel vertical potentially attracting speculative traders seeking specialized bets governed under CFTC oversight ([S12],).

Strategic Market Focus & Operational Efficiency

The recent wind-down of international operations enables Gemini to redeploy resources towards scaling U.S.-based activities where regulatory clarity benefits long-term growth prospects despite short-term revenue reduction in exiting geographies ([S12],[F1]). Complemented by ongoing cost optimization during restructuring phases including workforce reduction aims at improving adjusted EBITDA margins over time ([S11],[S14]).

Institutional Client Acquisition & Cross-Selling

Forging partnerships with asset managers, hedge funds, proprietary trading firms via advanced OTC desks and custody services creates an ecosystem sticky enough to withstand market gyrations allowing higher average revenue per client through cross-selling products such as derivatives plus custody plus stablecoins (,[S2]).

Risks / Watchpoints / Growth Constraints

Regulatory Risk: Regulatory uncertainty remains paramount especially related to staking programs which may be deemed securities offerings depending on evolving SEC interpretations; credit card interchange fees face litigation risk potentially impacting revenue; scaling new products requires continual license acquisition across jurisdictions ([S16],[S17],[S19]).

Market Volatility: Revenue highly sensitive to digital asset prices directly influencing transaction volume levels exposed Gemini earnings to inherent crypto market swings making forecasting challenging ([S13],[S27]).

Competitive Pressure: Unregulated entities potentially offer lower fees or novel products more agilely threatening user loss; regulatory arbitrage practices by competitors can distort market dynamics requiring constant innovation from Gemini (,[S27]).

Execution Risks: Restructuring efforts involve lay-offs risking operational disruptions; leadership changes alongside discontinuation of certain initiatives like NFT marketplace closure reduce diversification momentarily but refocus core competencies ([S21],[N1]). Litigation exposure including class actions adds financial unpredictability given unresolved legal claims ([S4],).

What to Watch Next

- Restructuring Impact: Monitor cadence of operational efficiencies post international market exits alongside adjusted EBITDA trends reflecting cost control effectiveness.

- User Base Dynamics: Tracking monthly transacting users (MTUs) trends especially domestically will indicate success of market concentration strategy.

- Product Adoption: Growth metrics on new offerings such as Gemini Predictions contracts volume alongside expanded staking participation rates will demonstrate effective innovation uptake.

- Regulatory Developments: Closely observe any material changes in SEC enforcement stance regarding staking/yield products or credit card fee structures that could materially affect revenue streams.

- Financial Flexibility: Evaluate capital deployment following recent $100 million placement whether directed towards acquisitions/investments or technology enhancements supporting future scaling.

Financial Profile Summary

Gemini closed Q1 2026 with solid liquidity reflected by cash & cash equivalents exceeding $215 million supported by current assets totaling approximately $1.33 billion against current liabilities near $1.05 billion yielding a healthy current ratio of about 1.27 indicating robust short-term solvency [F1], [S5]. Interest expense emerged due primarily to funding arrangements related to credit card receivables established mid-2025 but remained moderate relative to scale [S2]. Adjusted EBITDA improved slightly but remains negative at nearly -$60 million reflecting combined effects of restructuring charges plus elevated stock-based compensation conforming with strategic investments into growth initiatives plus overhead reduction efforts [S11].

This analysis focuses solely on publicly available SEC filings and company disclosures without providing investment advice or research views.

Financial position in context

As of 2026-03-31, companyfacts shows $216mm in cash and equivalents [F1]. Current assets of $1334mm and current liabilities of $1047mm imply a current ratio near 1.27x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments