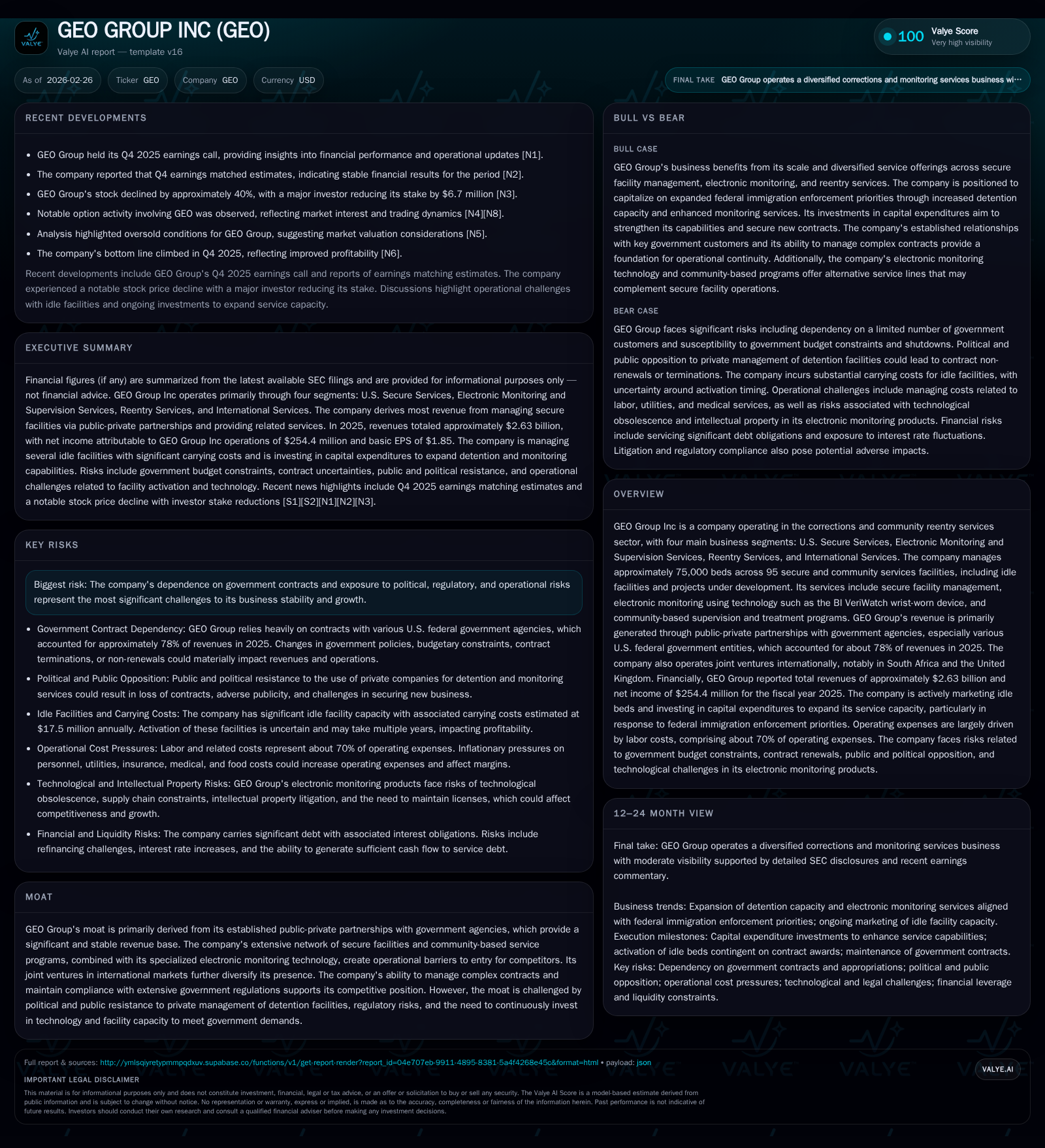

GEO Group's Recovery Efforts: Balancing Growth with Rising Costs and Regulatory Challenges

Examining GEO Group Inc’s recent financial trajectory, growth drivers in federal detention services, regulatory risks, and capital management strategy.

GEO Group Inc posted a 3.9% revenue increase in 2025 while operating income declined due to rising operating expenses and substantial capital investments. The company is capitalizing on expanded federal immigration enforcement priorities, supporting growth opportunities through facility expansions and electronic monitoring technology upgrades. However, near-term cash flow pressures and political/regulatory headwinds remain significant challenges. Amendments to credit agreements provide enhanced liquidity and flexibility amid aggressive share repurchases and a steady dividend policy, reflecting a nuanced recovery approach amid broader industry uncertainties.

Historical Financial Performance Trends and Margin Dynamics

GEO Group Inc exhibited a mixed financial performance in FY2025 characterized by top-line growth juxtaposed against margin compression. Revenues rose modestly by 3.9% year-over-year reaching approximately $2.57 billion [F1]. However, operating income declined notably by 16.9% to about $257 million driven largely by escalating operating expenses including labor inflation and costs related to unoccupied facilities [S1][S2]. Despite the operating income contraction, net income improved dramatically by nearly seven times to roughly $254 million compared with FY2024 [F1], reflecting favorable non-operating impacts documented in the annual report [S1]. Notably, operating cash flow contracted steeply by about 70% to just $72.6 million as substantial capital expenditure outlays intensified cash demands [F1].

Margins faced pressure from wage inflation—labor comprises approximately 70% of operating expenses—and higher consumable costs like food, utilities, insurance, and medical services also weighed on profitability [S1][S2]. Idle secure beds totaling nearly 6,600 across segments contributed an estimated $23.4 million in carrying costs during the year [S1], further diluting overall margins amid transitioning or start-up operational expenses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 254 | 73 | 257 | 198 | +695.8% |

| 2024 | 32 | 242 | 310 | 79 | -70.2% |

| 2023 | 107 | 285 | 352 | 73 | -37.5% |

| 2022 | 172 | 296 | 383 | 90 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 91 | -125 | |

| 2024 | 164 | ||

| 2023 | 30 | 212 | |

| 2022 | 30 | 9 | 206 |

Source: SEC companyfacts cache [F1].

Table: Key annual financial metrics illustrating revenue growth contrasting margin compression and cash flow decline due to increased capex.

Shifting Revenue Mix and Operational Cost Drivers

GEO’s operations span U.S Secure Services, Electronic Monitoring & Supervision Services, Reentry Services, and International Services [S1][S10]. The foremost revenue contributor continues to be U.S.-based secure detention facility management under long-standing public-private partnership contracts with federal agencies—predominantly immigration enforcement bodies—which accounted for roughly 78% of revenues in 2025 [S1][S10]. This heavy dependence ties GEO's top line closely to federal government policy shifts.

Labor expenses represent approximately 70% of total operating costs—a typical feature given the labor-intensive nature of facility management involving guard staffing and operational personnel [S1][S2]. Inflationary pressures throughout the year impacted wages but also increased ancillary costs such as utilities consumption rates (electricity heating/cooling), insurance premiums reflective of the risk profile inherent in corrections operations, medical expenditures for detainees including emergent care requirements, and food service inflation [S1][S2].

The company's operational leverage is nuanced: while fixed costs dominate certain segments—evident in ongoing carrying costs related to idle beds (~6,600 empty beds representing millions annually)—the incremental revenue from activating currently unused capacity can benefit profitability if labor scaling is managed efficiently [S1]. This dynamic underscores the importance of contract renewals for idled facilities.

Electronic Monitoring employs proprietary technology including BI VeriWatch wristbands which are central to community-based supervision programs offering alternatives or complements to incarceration [S1][N1]. Investment momentum here aligns with broader justice system trends emphasizing rehabilitation over detention.

Market Outlook and Growth Catalysts in Federal Detention Services

GEO is actively preparing for what it characterizes as an "unprecedented opportunity" stemming from expanded immigration enforcement priorities under current administration directives reversing prior bans on private detention contract renewals [S1][S2][N1]. Early executive orders have validated a renewal-positive environment which supports signing new contracts or reactivating previously idle bed capacities.

However, this optimism is tempered with caution—risks persist around potential government shutdowns impacting budgets or delays in contract renewals/rebids [S1][S2]. The company also acknowledges threats from political resistance to privatized corrections services which could influence future public-private partnership growth trajectories negatively.

To capitalize on these prospects, GEO is investing heavily in increasing detention capacity infrastructure as well as expanding secure transportation services integrated with electronic monitoring capabilities [N1][S2]. These strategic moves aim to broaden service offerings beyond static bed management into comprehensive correctional logistics.

Regulatory Risks and Legal Proceedings Impacting Business Stability

The regulatory landscape presents material uncertainties. The Company faces ongoing class action litigation primarily related to detainee work programs alleging violations under the Federal Trafficking Victims Protection Act claims filed since 2014 with unresolved appeals extending through early 2025 filings seeking Supreme Court review [S1][S8]. Such litigation could lead to significant liabilities or contract modifications affecting revenues.

Additionally, political scrutiny over managing private detention facilities remains a reputational risk that complicates contract renewals with public agencies wary of community sentiment [S8]. Conditions imposed via evolving regulations may increase operational compliance burdens or constrain flexibility.

Capital Spending Focused on Expanding Detention Capacity and Tech Investments

Capex surged by more than 150% year-over-year in FY25 to nearly $198 million driven largely by facility expansions aimed at addressing expected demand growth plus significant upgrades in electronic monitoring systems such as the BI VeriWatch platform [F1][S1][S2]. This capital intensity spike corresponds with strategic expansion but exerts near-term pressure on free cash flow which turned negative by approximately $125 million last year given depressed operating cash flows [F1].

Management highlights that investments focus not only on physical bed capacity but also bolster capabilities delivering secure transportation logistics and community-supervision technologies supporting state-of-the-art correctional service delivery models [N1][S2].

Liquidity, Debt Profile, and Credit Agreement Amendments

At end-2025 GEO held about $69 million in unrestricted cash equivalents providing a solid liquidity buffer alongside an amended revolving credit facility commitment increased from $310 million to $450 million with maturity extended through mid-2030 [S4]-[S7][S13]. This amendment included covenant relaxations especially regarding leverage limits enabling enhanced restricted payment flexibility such as dividends or share buybacks.

Total debt comprises senior secured notes at an 8.625% fixed coupon due in 2029 alongside unsecured notes maturing in 2031 at above 10%, consistent with sector risk profiles given ongoing legal exposures [S6][S7]. Weighted average interest rate stood near 8.61%, manageable but necessitating diligent coverage amid earnings volatility [S19].

These refinancings extend funding runway critical for absorbing heavy capex spend while maintaining shareholder return programs.

Capital Allocation Strategy: Dividends, Share Repurchases, and Returns Analysis

The company maintained an estimated ROE of roughly 16.9% based on net income over shareholders’ equity despite operational challenges last year [F1]. Consistent dividend payouts persisted though modest relative yield shifts occurred given stock price fluctuations [F1][S17].

Share repurchase activity accelerated substantially with almost $91 million spent buying back shares during FY25 compared with smaller buybacks pre-2023 linked to Board authorization expansions raising repurchase authorization from $300 million up to $500 million lasting through end-2029 [F1][S17]. These buybacks align with efforts to restore investor confidence following volatile market reactions after earnings announcements caused sharp share price declines noted in recent news flows [N4].

Capital allocation balances returning value against retaining flexibility for ongoing investment needs given regulatory constraints embedded within credit agreements limiting excess cash deployment without covenant compliance.

Key Milestones and Indicators to Monitor in 2026

Critical metrics moving into calendar year '26 include new or renewed contracts activating idle beds—a significant source for incremental revenue growth—as well as the company’s ability to contain operating expense escalation amid inflationary pressures detailed during earnings briefing calls [N1],[N7],[S3].

Capital project completion timelines will serve as leading indicators of management’s ability to convert investment spend into scalable service delivery capabilities enhancing onboarding potential governmental clients.

Monitoring regulatory developments regarding private prison legislation or additional executive orders impacting public-private partnerships will remain essential given their direct influence on contract stability or termination risks per disclosed risk disclosures ([S8]). In parallel litigation outcomes especially relating to detainee work programs pending before high courts could materially affect long-term risk provisioning.

This analysis synthesizes disclosures filed by GEO Group Inc up through February 26th 2026 combined with recent earnings call commentaries and prevailing sector dynamics relevant for understanding company performance without offering investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments