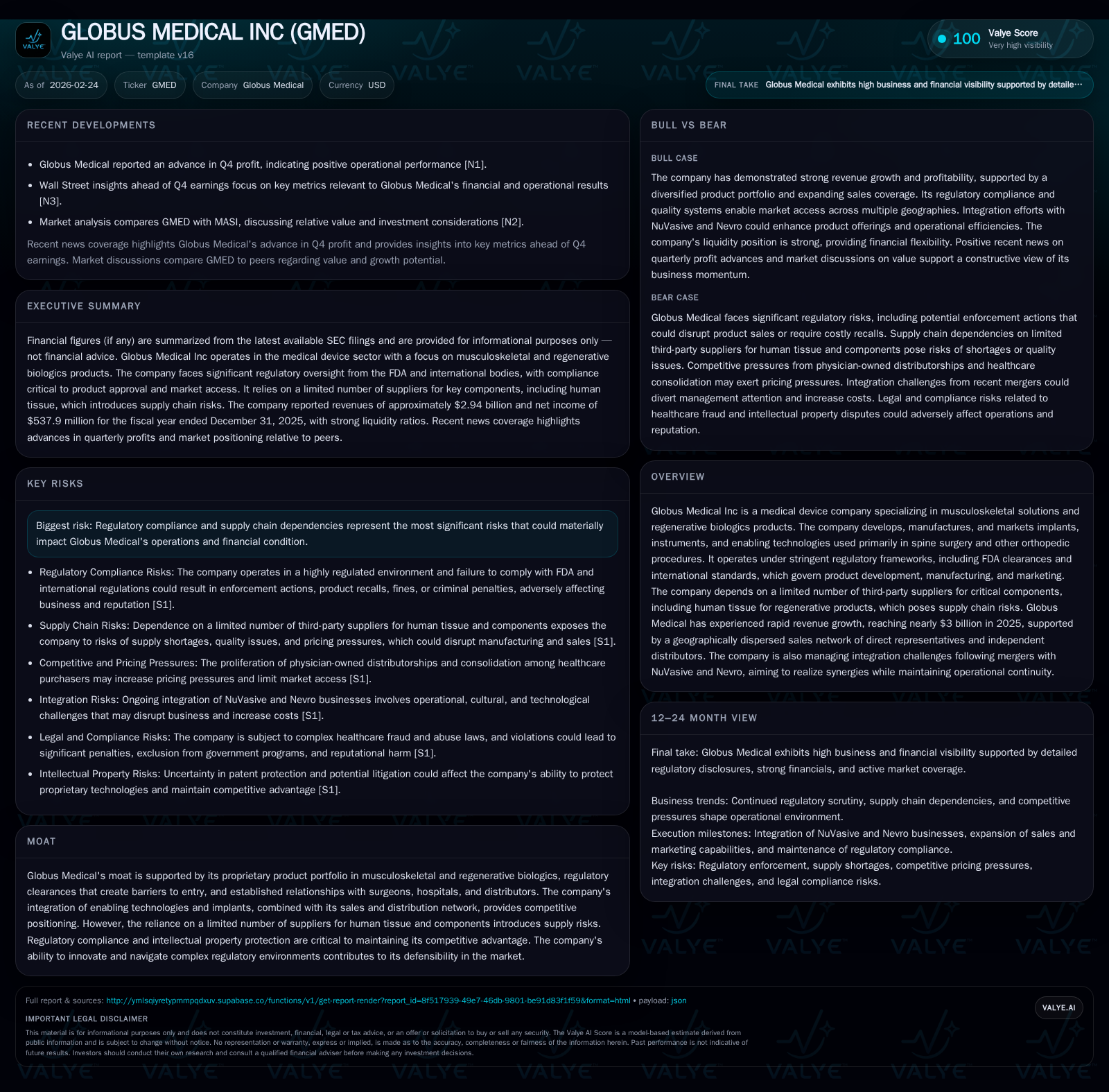

Globus Medical’s Surge to $3 Billion: Growth Fueled by Innovation and Strategic Integration

Globus Medical achieved near tripling of revenues from 2022 to 2025 through proprietary musculoskeletal technologies and targeted M&A integration, balancing robust operational expansion with regulatory and supply constraints.

From $1.02 billion in 2022 to almost $3 billion in 2025, Globus Medical's growth is driven by a combination of cutting-edge musculoskeletal implants, regenerative biologics, and enabling technologies alongside an expanding sales footprint. Integration of recent mergers has broadened market reach but imposes operational complexity. While operating income nearly tripled in the period evidencing margin expansion, net income volatility reflects evolving investment in growth and compliance. Regulatory frameworks and supplier concentration create ongoing risk considerations. Capital management is disciplined with significant share repurchases supported by strong free cash flow generation.

Historic Growth Trajectory and Drivers Behind Revenue Expansion

Globus Medical's financial trajectory over the past four years is striking: revenues surged from approximately $1.02 billion in FY2022 to nearly $3 billion by FY2025 [F1], representing a compound annual growth rate well above 35%. This outsized growth derives from a blend of organic product innovation—centered on musculoskeletal implants coupled with enabling surgical technologies—and strategic acquisitions that have been effectively integrated to increase scale.

Notably, operating income exhibited a compelling acceleration rising from $228 million in FY22 to nearly $480 million in FY25 (+110%), with a particularly sharp year-over-year gain of 189% reported in FY25 alone [F1]. The operating margin improvement reflects a combination of operational leverage as fixed costs are absorbed amid scale expansion alongside focused cost control despite escalating compliance demands.

Net income has shown more variability yet posted substantial gains—from $190 million in FY22 to over $537 million in FY25 (+182%)—indicating episodic impacts related to integration expenses, R&D investments, or non-operating items that warrant further quarterly review [F1]. The expanding top-line is thus being translated with increasing efficiency into bottom-line profits while supporting reinvestment.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2.9 | 538 | 753 | 480 | +16.7% | +422.3% |

| 2024 | 2.5 | 103 | 521 | 166 | +60.6% | -16.2% |

| 2023 | 1.6 | 123 | 243 | 133 | +53.3% | -35.4% |

| 2022 | 1.0 | 190 | 178 | 228 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 300 | 589 | 11.8 |

| 2024 | 86 | 405 | 2.5 |

| 2023 | 226 | 165 | 3.1 |

| 2022 | 144 | 104 | 10.3 |

Source: SEC companyfacts cache [F1].

*Note: Net YoY % for FY24 & FY23 reflect decreases relative to prior year despite revenue gains; CFO = Operating Cash Flow.

Innovative Product Mix and Clinical Adoption Fueling Future Opportunities

Globus Medical’s arsenal centers on musculoskeletal implants tailored primarily for spine surgery, supplemented by advanced enabling technologies that enhance procedural efficacy—a critical enabler given surgeons’ demand for integrated solutions underpinned by FDA clearances via the rigorous 510(k) process [N13][S1].

Regenerative biologics—products derived from human tissue—add a high-growth dimension but carry intrinsic supply complexity due to tissue procurement constraints from limited suppliers, increasing risk exposure while underscoring the firm's technical prowess.

The company’s clinical adoption rates benefit from tightly woven relationships with surgeons and hospitals facilitated through direct sales teams augmented by independent distributors internationally—this dual-channel approach ensures broad penetration yet requires careful calibration amid growing scrutiny over physician-owned distributorships (PODs) which may intensify price competition [S1].

Integration Progress: M&A Effects on Scale and Market Reach

Recent mergers have expanded Globus Medical’s geographic footprint and deepened its product suite beyond spine implants into other orthopedic domains, simultaneously enhancing distribution networks [N10][S1]. While synergies are materializing through consolidated sales efforts, the task of harmonizing diverse operating cultures alongside managing a broader inventory base—including high-value instrument sets loaned on consignment to surgery centers—remains formidable.

The enlarged portfolio presents cross-selling opportunities; however, it necessitates vigilant lifecycle management of product approvals given regulatory variances and periodic revalidations inherent in medical devices under evolving standards.

Regulatory Frameworks and Supply Chain Constraints as Dual Moderators

A cornerstone challenge resides in navigating an intricate regulatory environment governed chiefly by the FDA in the U.S., alongside international counterpart authorities enforcing MDR compliance (notably within the EEA). Modifications triggering new submissions—510(k)s or PMA supplements—can delay product introductions or force market withdrawals if clearances are delayed or denied [S1][S4][S5][S24].

Supply chain fragility is pronounced especially for regenerative biologics reliant on human tissue sourced via limited third parties bound by strict screening protocols amidst public sensitivity concerning donor tissues [S12][S22]. Any disruption can choke production pipelines swiftly given low inventory buffers inherent in biologic implants.

Further complicating compliance risks are intensified federal/state scrutiny over physician inducements categorized under anti-kickback statutes and recent spikes in investigations targeting healthcare payments—which may entail costly consent decrees or corporate integrity agreements if breached .

Operating Income and Net Margin Evolution: Path to Profitability Leverage

Despite revenue nearly tripling between FY22-25, operating income grew at an even faster pace (+189% YoY last reported), moving operating margins upwards markedly—a testament to improving overhead absorption across fixed costs plus selective price discipline amidst POD-driven pricing pressures [F1].

Net income experienced bouts of volatility particularly around FY23-FY24 likely due to integration expenses or one-time items but rebounded sharply in FY25 confirming earnings resilience supported by operational gains.

Capital Allocation Approach: Share Repurchases, Capex, and Cash Flow Generation

Globus Medical demonstrates disciplined capital policies characterized by meaningful share repurchases scaling from $144M in FY22 up to over $300M in FY25—a signal of confidence anchored on an absence of dividends [F1][S10]. This buyback trajectory underscores commitment to returning value while managing share count dilution prudently.

Capital expenditures surged meaningfully (+42% YoY into FY25 reaching $165M), reflecting investments into manufacturing capacity expansions including procurement of instrument sets typically loaned to hospitals—a strategic asset facilitating surgeon preference retention.

Operating cash flow has grown robustly alongside revenue gains; producing nearly $753 million in FY25 versus $178 million four years prior leaving ample free cash flow after capex (~$589 million)—fueling both internal growth initiatives and shareholder returns without notable liquidity strain [F1].

Approximate Return on Equity (ROE) computes around ~11.8% for FY25 (net income/equity), signaling moderate capital efficiency balanced against growth reinvestment unobscured by dividend payouts [F1].

Monitoring Key Milestones: What to Watch in Upcoming Earnings and Approvals

Investor focus should center on near-term developments including Q4 results anticipated shortly following February guidance preannouncements indicating continued earnings strength [N1][N6][N10].

Success or delay around regulatory filings—especially device modifications requiring additional clearances—and progress integrating new acquisitions will materially impact forward momentum.

Scaling direct sales forces further into untapped geographies or procedurally adjacent specialties also merits close tracking as this underpins incremental market share capture.

Competitive Moat: Surgeon Relationships, Enabling Technologies, and IP Barriers

Globus Medical's defense lies robustly in its proprietary IP portfolio aligning musculoskeletal implants with patented enabling technologies, delivering incremental clinical utility sought after by surgeons familiar with its platform offerings ["Valye_excerpt_moat"][S1].

Established direct sales teams backed by trusted independent distributors cement surgeon-hospital ties critical for preference generation amid an industry where switching costs from established systems are elevated.

Nevertheless, physician-owned distributorships pose competitive headwinds pushing prices lower—making intellectual property protection plus service excellence vital moats maintaining spread sustenance.

Risk Matrix: Compliance, Litigation, and Market Pressure Dynamics

Regulatory risk is omnipresent with potential FDA enforcement actions—for untitled letters up to import alerts—that could sharply restrict sales or force costly recalls impacting brand stature heavily documented within the latest Form 10-K disclosures . The volatile healthcare compliance landscape includes growing crackdowns on marketing practices scrutinized under anti-kickback laws with associated risk of multi-year monitoring agreements.

Furthermore, extensive litigation exposure exists related to intellectual property disputes, trade secret allegations particularly tied to competitive hiring practices or distributor conflicts which strain management bandwidth and could entail material damages if lost.

Supply disruptions concerning donor tissue availability remain an intermittent but critical bottleneck threatening biologic product lines directly affecting treatment availability.

Lastly, evolving reimbursement frameworks amidst healthcare consolidation pressure pricing power rendering continual innovation imperative to justify premium positioning.[S4,S5,S7]

Disclaimer: This report is based solely on publicly available information as of February 24, 2026 including SEC filings (10-K/10-Q), company releases and sector analysis without offering any form of investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments