Murphy Oil Corp Faces Earnings Pressure and Talent Challenges in 2025

Murphy Oil’s sharp profit contraction contrasts with operational resilience as it grapples with workforce scarcity and regulatory uncertainties.

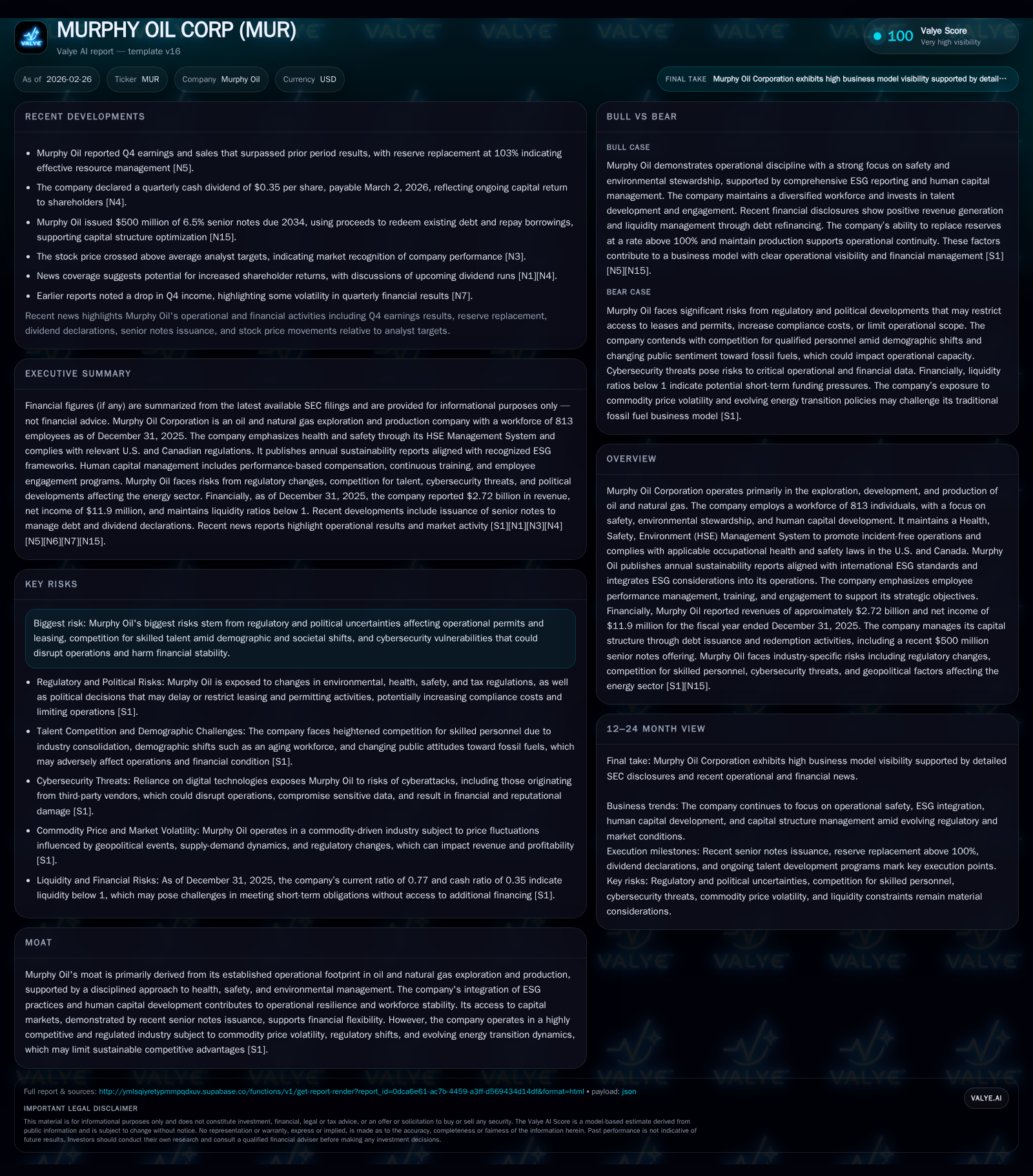

Murphy Oil reported a significant earnings decline in 2025 despite maintaining a robust reserve replacement ratio above 100%, underscoring operational discipline amid commodity price volatility. Talent scarcity driven by demographic shifts and intense industry competition is raising costs and operational risks. The company’s capital structure moves, including a $500 million senior notes issuance to refinance near-term debt, highlight strategic financial management under pressure. Murphy also faces evolving regulatory challenges and cybersecurity risks but continues to emphasize safety, ESG integration, and human capital development in its operational framework.

Earnings Review: A Steep Revenue and Profit Downturn

Murphy Oil reported revenues of $2.72 billion for FY2025, down 10.2% from $3.03 billion in FY2024 [F1]. Operating income was halved to approximately $301 million from $603 million in the prior year, while net income plunged 76%, falling from $50.3 million to $11.9 million [F1]. This pronounced profitability squeeze reflects external headwinds including weakened commodity prices impacting realized pricing for its hydrocarbons [S1][N2][N3]. Compounding pressures, a failed exploration attempt at the Civette well led to a notable share price reaction and added to near-term operational challenges [N10]. Despite these earnings pressures, Murphy sustained strong operating cash flow momentum growing 77% year-over-year relative to prior periods although exact recent figures are not disclosed [F1]. These dynamics underscore a stark divergence between near-term earnings volatility and underlying liquidity resilience.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 2.7 | 12 | 301 | -10.2% | -76.3% |

| 2024 | 3.0 | 50 | 603 | -12.5% | -56.8% |

| 2023 | 3.5 | 116 | 1042 | -12.0% | -41.6% |

| 2022 | 3.9 | 199 | 1587 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 103 | 0.2 |

| 2024 | 301 | 1.0 |

| 2023 | 150 | 2.2 |

| 2022 | 4.0 |

Source: SEC companyfacts cache [F1].

Operational Highlights: Reserve Replacement Surpassing Expectations

Murphy’s reserve replacement ratio reached an encouraging 103% in recent announcements [N2][N3], indicating that its proved reserves are being effectively replenished despite exploration misses such as Civette [N10]. This suggests that production sustainability is well supported over the medium term through disciplined capital deployment into appraisal and development activities.

Talent Competition Amid Industry Demographic Shifts

The company highlights growing difficulties in recruiting and retaining qualified personnel amid industry-wide demographic trends including an aging workforce and shrinking talent pipeline [S1]. These human capital constraints increase wage inflation pressures on operating cost structures and pose risks to future project execution timelines. Competition from other sectors for transferable skill sets further complicates talent acquisition efforts.

Regulatory Environment and Emerging Energy Transition Risks

Murphy confronts an evolving regulatory landscape shaped by climate change mandates, greenhouse gas emission policies, and fluctuating government leasing regimes [S4][S5][S6][S8]. Recent U.S. administration directives have oscillated between moratoriums on new leases and promotion of domestic energy development culminating in revisions to offshore leasing programs [S21]. Global decarbonization trends raise demand uncertainty for fossil fuels which could constrain hydrocarbon pricing power over time. Legal claims related to environmental liabilities remain extant risks though judged non-material presently [S6].

Capital Structure Actions: Senior Notes Issuance and Debt Redeployment

To manage its leverage profile prudently under constrained free cash flows, Murphy issued $500 million of senior notes at a coupon of 6.5%, maturing in 2034, with proceeds targeted to redeem existing higher-coupon notes due in 2027 and 2028 as well as repay borrowings on its revolving credit facility [N12][S9][S11][S18]. This move extends debt maturities while maintaining flexibility amid margin pressure. Credit commitments increased from $1.35 billion to $2 billion with extended facility maturity through January 2031 [S22]. Despite active capital structure optimization efforts, the current ratio remains below one at approximately 0.77 indicating near-term liquidity tightness mitigated by revolving credit availability [F1]. Share repurchases slowed sharply from $301 million in 2024 to just over $102 million in 2025 reflecting cautious cash deployment [F1].

Dividend Outlook and Share Repurchase Trends

Dividend payments continue as a shareholder return focus with market commentary anticipating increased dividend yield opportunities based on option market signals [N6][N8][N11]. However, net income weakness coupled with negative free cash flow (operating cash flow less capex) challenges capacity for aggressive buybacks or dividend hikes without eroding liquidity [F1][S23]. This conservative payout stance aligns with preserving financial flexibility while balancing stakeholder interests.

Cybersecurity and Technology Risks in Digital Operations

Increasing reliance on digital technologies across extraction operations exposes Murphy to heightened cybersecurity threats targeting IT and OT systems integral for seismic analysis, drilling control, financial data processing, and communications [S1][S7][S24]. The sophistication of cyberattacks including AI-facilitated intrusion methods mandates continuous upgrades of defense mechanisms along with vigilance over third-party supply chain vulnerabilities.

Human Capital and ESG Integration Efforts

Complementing operational challenges is Murphy’s structured Health, Safety, Environment (HSE) Management System promoting incident-free operations through consistent training aligned with OSHA regulations across U.S. and Canadian jurisdictions [S1][S28]. The company publishes sustainability reports consistent with SASB, TCFD, GRI frameworks evidencing proactive ESG disclosure practices [S1]. Its human capital strategy hinges on compensation design, performance management systems, talent development initiatives including digital learning platforms, mandatory compliance training with full utilization rates, employee feedback loops, and engagement programs aimed at enhancing workforce stability [S1][S23].

Forward-Looking: Key Milestones and Market Signals to Watch

Market participants should track forthcoming exploration updates beyond the Civette setback for revised reserve additions or potential write-downs that could recalibrate asset base valuation [N10][N2][N3]. Regulatory outcomes affecting lease availability or environmental compliance requirements will materially shape investment appetite and production scale trajectories. Capital allocation decisions balancing reinvestment against shareholder returns remain critical amid volatile commodity prices.

This analysis incorporates scrutiny of Murphy Oil Corporation's public filings along with recent market disclosures. It does not constitute investment advice but aims to present an informed review grounded strictly on disclosed data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments