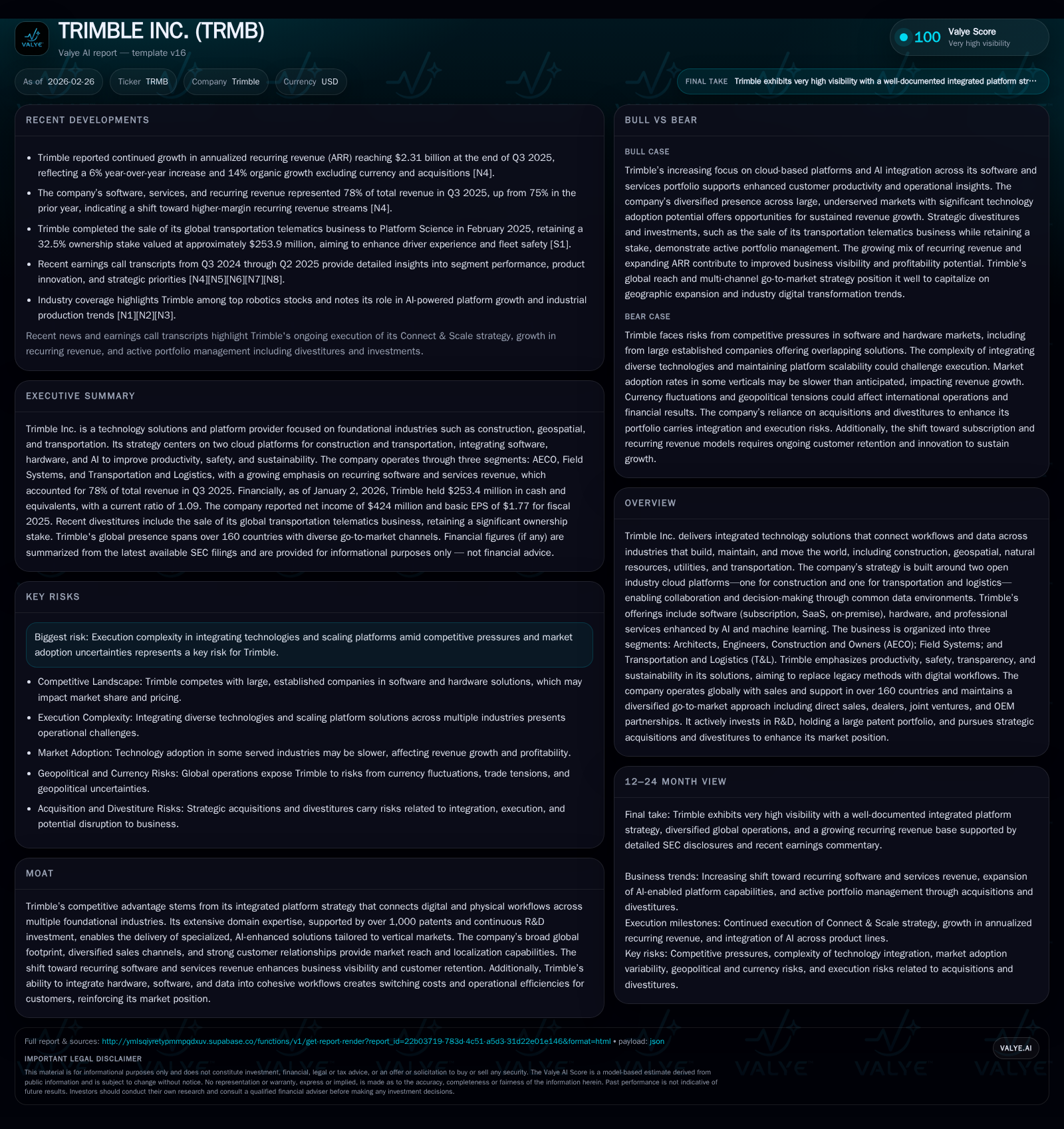

Trimble Inc. Strengthens Platform Strategy While Managing Integration and Market Risks

Trimble advances its integrated technology suites across construction and transportation sectors with a growing focus on subscription revenue and AI-powered workflows.

Trimble Inc. has progressively grown its revenues and operating income through strategic shifts toward recurring software and services, augmented by investments in AI and platform integration across construction and transportation industries. Despite a modest revenue growth of 3.3% in FY2023 and a substantial 28.5% boost in operating income by FY2025, net income volatility and declining cash flow indicate transitional challenges amid divestitures and platform scaling. The firm’s capital allocation favors share repurchases, supporting equity base expansion, while navigating global supply chain risks and competitive pressures.

Historical Performance

Trimble Inc.'s financial trajectory over recent years highlights steady advancement in top-line figures accompanied by positive operating leverage. FY2023 revenue stood at approximately $3.8 billion (USD) [F1], marking a modest increase of about 3.3% from FY2022's $3.68 billion. This reflects the company's ability to sustain sales momentum amid evolving market conditions and strategic portfolio realignments.

Operating income experienced robust growth reaching $592 million in FY2025 from $460.7 million in FY2024—an almost 28.5% uplift demonstrating improved operational efficiency [F1]. This uptick was driven by favorable revenue mix shifts towards higher margin recurring software subscriptions plus cost realignment following divestitures such as the Mobility business sale in early 2025 [S16][S21].

However, net income showed high variability; for instance, a sharp decline of approximately 71.8% was recorded as $424 million in FY2025 versus $1.5 billion in FY2024 [F1]. The prior year's spike included a significant pre-tax gain (~$1.7 billion) arising from equity method accounting upon divestiture transactions [S21]. Such non-operational gains impacted comparability.

At the cash flow level, while operating cash flow remains strong at $386 million for FY2025 it declined about 27% from prior year ($531 million), partially reflecting working capital changes linked to transformation initiatives [F1]. Capital expenditures have correspondingly receded near $25-30 million annually maintaining a conservative asset reinvestment approach.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 424 | 386 | 592 | -71.8% | ||

| 2024 | 1504 | 531 | 461 | +383.3% | ||

| 2023 | 3.8 | 311 | 597 | 449 | +3.3% | -30.8% |

| 2022 | 3.7 | 450 | 391 | 511 | +0.5% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 863 | 361 | 7.3 |

| 2024 | 175 | 498 | 26.2 |

| 2023 | 100 | 555 | 6.9 |

| 2022 | 395 | 348 | 11.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue data available only through FY2023 [F1]. Operating income and net figures for FY2024/25 reflect continued improvements albeit influenced by divestiture accounting.

Business Model and Segment Analysis

Trimble operates via three distinct segments: Architects, Engineers, Construction and Owners (AECO), Field Systems, and Transportation & Logistics (T&L). Each serves specialized verticals with tailored hardware, software, and professional services predominantly aiming to digitize workflows that span design to execution phases [S1][S7].

- AECO focuses mainly on software solutions enabling design collaboration, asset lifecycle management, civil project planning, with primary sales through direct channels emphasizing integration with construction clients' operational lifecycles [S7][S9].

- Field Systems comprises hardware-intensive geospatial instruments coupled with proprietary software sold mainly through independent global distributors servicing surveyors, civil engineers, construction fields [S6][S7].

- Transportation & Logistics delivers SaaS enterprise transport management systems (TMS), mapping applications (e.g., PC*Miler), dock yard management delivered principally by direct sales targeting truckload freight markets worldwide [S13][S16].

The company has increasingly shifted toward subscription-based revenues representing around 78% of total revenues as of late-2025 quarters [S8][S11]. Annualized Recurring Revenue (ARR) reached approximately $2.31 billion growing organically at ~14% excluding currency effects and acquisitions/divestitures [S11], signaling strong adoption of recurring software services.

Innovation remains central; Trimble leverages AI-powered enhancements within their platform solutions including autonomous logistics agents that improve decision making via predictive analytics—a differentiator relative to more transactional point-solution competitors [N5][S16].

Growth Prospects and Constraints

Growth is primarily anchored on several vectors:

- Platform Expansion: The two open industry cloud platforms aimed at construction and transportation unlock opportunities for ecosystem network effects facilitating collaboration among stakeholders leveraging common data environments [S9].

- AI & Machine Learning: Embedding AI agents within TMS workflows offers operational automation potential expected to expand market penetration especially in trucking fleet management [N4][N5].

- Recurring Revenue Momentum: Continuing subscription ARR growth translates to improved visibility on future revenues amidst shifting industry preference from hardware point products toward integrated digital workflows [S8][S11].

- Geographic Diversification: Robust international footprint spanning over forty countries aids localized market penetration minimizing risks of regional economic downturns or regulation shifts [S10].

- Strategic Acquisitions/Divestitures: Recent Mobility business sale positions Trimble as an ecosystem partner while focusing capital on core segments; targeted acquisitions complement innovation pipeline [S21].

Constraints potentially capping growth include:

- Execution complexities integrating new technologies into cohesive platforms while managing legacy customer transitions.

- Supply chain vulnerabilities stemming from reliance on limited contract manufacturers could impact delivery timelines amidst global disruptions [S1].

- Competitive pressure from entrenched incumbents offering deep vendor relationships or specialized niche software solutions requiring continued domain differentiation.

- Macroeconomic uncertainties including tariff impacts, inflationary cost pressures, fluctuating currency rates affecting both costs and international demand dynamics [S28].

Key Forecasts and Milestones to Monitor

While explicit forward guidance is not provided within the filings reviewed,[N6][N7], notable milestones include:

- Successful scaling of AI-enabled modules within Transportation & Logistics cloud platforms.

- Achieving sustained organic ARR growth above mid-teens percentages sequentially.

- Execution of ongoing share repurchase programs delivering shareholder capital returns without undermining balance sheet flexibility.

- Expanding software penetration within Field Systems replacing legacy hardware-bound methods with integrated digital workflows.

- Managing divestiture-related transitions without materially disrupting customer retention metrics.

Market observers should track quarterly disclosures around ARR progression, platform adoption metrics particularly within T&L segment enhancements post-new product introductions announced during late-2025 periods [N4][N5], as well as any commentary regarding supply chain or geopolitical trade shifts impacting operations.

Capital Allocation Strategy and Financial Returns

Trimble demonstrated a clear preference for shareholder capital returns through stock buybacks highlighted by approximately $863 million repurchased during FY2025—substantially larger than the prior year’s modest ~$175 million activity demonstrating confidence amid ongoing repositioning [F1][S12].

Capital expenditures remain disciplined falling under $30 million annually reflecting efficient operations without aggressive infrastructure investments that could strain free cash flow generation [F1].

Return metrics suggest an approximate return on equity near ~7.3%, reflecting moderate profitability relative to equity base expanded partially through retained earnings plus share repurchase accretive effects [F1]. Cash flow generation remains positive but moderated compared to historical peaks tinged by integration costs associated with portfolio streamlining.

Debt levels approximate $1.39 billion in senior unsecured notes alongside available revolving credit facilities providing liquidity flexibility that aligns well with the company's scale without excessive leverage risk exposure—debt covenants are currently maintained comfortably [S15][S17].

Industry Context Analysis

Trimble operates within foundational industrial sectors transitioning toward digital transformation though adoption curves vary widely due to entrenched traditional practices especially within construction trades. Covered markets exceed trillions globally but characterized by fragmented customer bases necessitating scalable yet customizable solutions that Trimble seeks via its platform strategy. In transport logistics, technological evolution driven by regulatory mandates related to safety/emissions alongside efficiency demands fuels interest in connected telematics—an area ripe for AI powered automation as pursued by Trimble.

The successful integration of AI-enhanced workflows into expansive platform ecosystems can create switching costs strengthening competitive moats beyond basic product features.

Risks Summary

The foremost risk cluster involves execution complexity ensuring newly integrated platform features scale effectively across heterogeneous markets while sustaining legacy client trust which is compounded by rising competitive intensity from established ERP/software players plus nimble startups focusing solely on digital freight or BIM niches.[S29] Supply chain dependencies exacerbate vulnerability given limited contract manufacturing arrangements combined with tightening global tariffs posing potential cost inflation or delivery delays.[S28] Geopolitical tensions risk disrupting cross-border sales or access—as significant portion of revenues emanate internationally—and invite local competitors protectionism responses.[S1] Currency volatility combined with regulatory compliance burdens add layers of financial forecasting uncertainty potentially impacting margins or price competitiveness.[S28] Finally shifting channel dynamics amid evolving go-to-market strategies demand precise coordination with dealer networks preventing market coverage gaps or channel conflicts harming sales effectiveness.[S25]

Conclusion

Trimble Inc.’s ongoing evolution reflects a deliberate shift from hardware-dominant legacy toward integrated SaaS platforms augmented by advanced analytics targeting critical workflows in construction and logistics verticals. Financial performance trends underscore this transition’s early benefits yet also highlight episodic net income swings tied to strategic divestments. The robust portfolio mix enriched by continuous R&D investment leverages valuable patents supporting proprietary advantages while dedicated investment in AI-enabled automation gives Trimble distinctive positioning amidst intensifying competition. Future vigilance will be warranted regarding execution risks associated with platform scaling alongside macroeconomic challenges globally affecting supply chains and market demand dynamics. Meanwhile, shareholder value is bolstered through decisive capital return programs balanced against judicious operational spending reflecting mature corporate stewardship. This profile situates Trimble as a compelling case study of industrial technology digitization balancing legacy operational realities with the promise embedded software-centric ecosystems offer for productivity gains across multiple industries shaping modern infrastructure development.

This report is intended solely for informational purposes without providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments