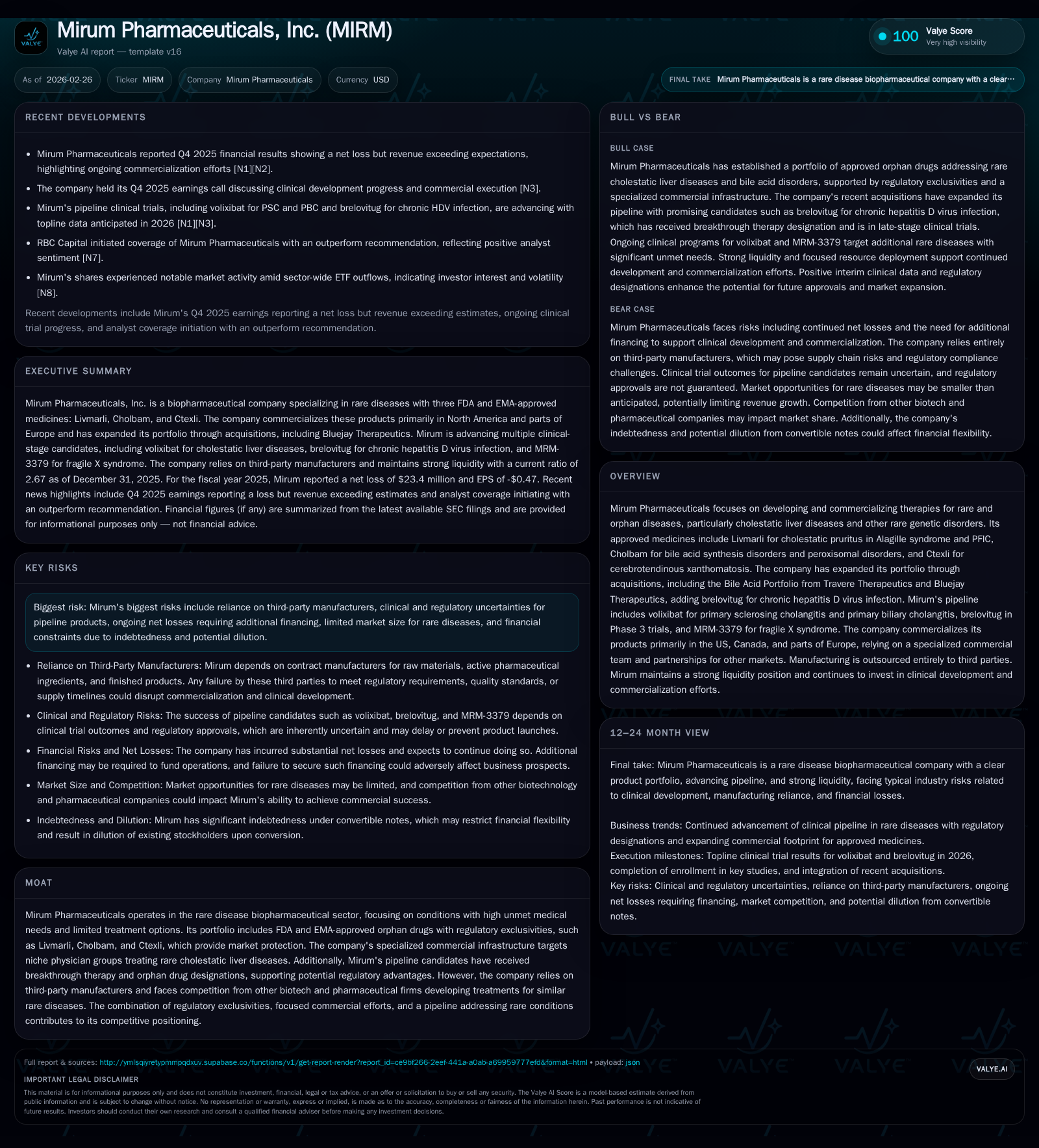

Mirum Pharmaceuticals’ Rare Disease Focus Drives Revenue Growth Despite Persistent Losses and Regulatory Hurdles

Specialized orphan drug portfolio and pipeline expansion underpin financial and operational developments.

Mirum Pharmaceuticals has grown revenue primarily through commercializing orphan drugs targeting cholestatic liver diseases and rare genetic disorders, enhanced by strategic acquisitions such as the Bile Acid Portfolio. Despite top-line growth, the company continues to report net losses driven by high operating expenses associated with sales expansion, R&D, and legal proceedings over patent protections. Mirum’s future growth hinges on advancing late-stage candidates like brelovitug and volixibat and expanding geographic reach while navigating complex regulatory and pricing environments. Robust operating cash flow improvement underpins operational resilience, but ongoing reliance on third-party manufacturers and the limited patient populations of its rare disease indications remain key constraints.

Historical Financial Performance

Mirum Pharmaceuticals has demonstrated a clear trajectory of revenue growth fueled by commercialization efforts for its suite of orphan drugs targeting rare cholestatic liver diseases and genetic disorders. While exact annual revenues are limited to a 2021 figure of approximately $19.1 million [F1], recent SEC filings report narrowing operating losses, evidencing improved operational leverage.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -23 | 56 | -22 | 954000 | +73.4% |

| 2024 | -88 | 10 | -88 | 993000 | +46.2% |

| 2023 | -163 | -71 | -109 | 109000 | -20.5% |

| 2022 | -136 | -120 | -131 | 278000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 55 | -7.4 |

| 2024 | 9 | -39.0 |

| 2023 | -71 | -65.7 |

| 2022 | -120 | -95.5 |

Source: SEC companyfacts cache [F1].

Despite limited disclosed revenue data post-2021 [F1], operational results show a consistent reduction in losses: operating income improved by roughly 75% year-over-year in 2025 vs. 2024. This reflects Mirum’s scaling commercial operations coupled with cost discipline initiatives. The company’s net loss reduction of over $64 million year-over-year further underscores these trends.

Crucially, operating cash flow swung from deeply negative levels (-$120 million in 2022) to $55.8 million positive in FYE2025 [F1], representing a dramatic turnaround indicative of better working capital management and revenue scaling with contained operating expenses. After factoring capital expenditures under $1 million annually—which remain modest given the company’s primarily biopharma service model—free cash flow stands at approximately $54.9 million for FY25.

Shareholder equity expanded significantly to nearly $315 million by end-2025 from approximately $226 million a year prior [F1], indicating strengthened capitalization amidst ongoing investment in pipeline development.

Business Overview & Strategy

Mirum Pharmaceuticals centers on developing therapies for rare diseases with high unmet needs: notably cholestatic liver conditions like Alagille Syndrome (ALGS) and Progressive Familial Intrahepatic Cholestasis (PFIC), alongside other genetic disorders such as cerebrotendinous xanthomatosis (CTX). Its commercial portfolio comprises three approved medicines:

- Livmarli (maralixibat): an oral ileal bile acid transporter inhibitor indicated for cholestatic pruritus associated with ALGS and PFIC across multiple regulatory jurisdictions including U.S., EU, Canada, and Japan.

- Cholbam (cholic acid): indicated for bile acid synthesis disorders due to single enzyme defects and adjunctive treatment for peroxisomal disorders.

- Ctexli (chenodiol): approved for CTX treatment following FDA approval in February 2025.

The company expanded its product set via acquisition of Travere Therapeutics’ Bile Acid Portfolio in August 2023 [S1], incorporating Cholbam and Ctexli under its commercialization banner. Mirum manages commercial activities through a focused sales force predominantly covering the U.S., Canada and selected European countries while leveraging partnerships for additional markets.

Pipeline development remains active with several investigational programs:

- Brelovitug: acquired with Bluejay Therapeutics assets targeting chronic hepatitis D virus infection; currently in Phase 3 trials.

- Volixibat: an oral IBAT inhibitor in development for primary sclerosing cholangitis (PSC) and primary biliary cholangitis (PBC), granted FDA breakthrough therapy and orphan drug designation.

- MRM-3379: program targeting fragile X syndrome expands Mirum's pipeline into neurodevelopmental rare diseases.

Growth strategy emphasizes broadening indications for Livmarli via clinical studies like EXPAND addressing other cholestatic pruritus etiologies [S1]. Moreover, Mirum evaluates partnerships globally to extend market access while internally scaling commercial capabilities where feasible.

Future Growth Prospects

Prospective growth drivers rest principally on pipeline maturation—approval of brelovitug would add a novel therapeutic addressing an underserved viral indication. Similarly, volixibat’s regulatory progress could anchor future revenue if approved given PSC/PBC’s severe disease burden without effective treatments.

Additional indications or label expansions could leverage existing marketing infrastructure to deepen penetration within known patient pools or adjacent rare disease subsets presently underserved.

Geographically expanding distribution networks beyond current North American and European footprints remains critical but contingent on regulatory approvals and partner collaborations.

Conversely, persistent challenges include the relatively small patient populations typical with orphan diseases which inherently cap total addressable market size [S1]. Competition emerges from both established biotech/pharma actors exploring similar rare liver conditions plus the threat of generic or compounded alternatives affects pricing power [S6].

Regulatory uncertainty—particularly surrounding patent litigations filed by generic manufacturers challenging exclusivity over Livmarli scheduled through March 2029—adds complexity to forecasting commercial longevity [S1],[S3]. Additionally regulatory requirements impose ongoing post-marketing surveillance costs with financial implications [S7],[S15]. Pricing pressures fueled by healthcare reform such as the Medicare Drug Price Negotiation Program may constrain reimbursement ceilings undermining profitability despite market demand [S9],[S19].

Returns & Capital Allocation

While Mirum remains unprofitable on a net income basis with losses narrowing to approximately $23.4 million in FY25 [F1], its improving operating income and substantial positive operating cash flow ($55.8 million in FY25) demonstrate advancing operational efficiencies alongside revenue gains.

The company's approximate return on equity stands at -7.4%, reflecting historical losses relative to shareholder equity buildup primarily funded by financing activities rather than retained earnings [F1]. No dividends or share buybacks are reported given prioritization of reinvestment into R&D and commercialization efforts.

Capital expenditures remain minimal (~$954k in FY25), consistent with a business model that outsources manufacturing while emphasizing clinical development investment internally or through partnerships.

Capital allocation decisions focus on advancing late-stage clinical programs while cautiously expanding commercial reach given limited scale economies inherent to niche rare disease markets [S1].

Regulatory & Market Risks

Mirum faces multifaceted risks typical of the biopharmaceutical industry specializing in orphan drug development:

- Patent Litigation: Multiple lawsuits contest patent validity for Livmarli launched under Hatch-Waxman procedures have resulted in stays preventing generics until at least March 29, 2029; counterclaims continue adding legal costs while adding uncertainty to market exclusivity duration [S1],[S6],[S17].

- Manufacturing Reliance: Dependence on third-party manufacturers introduces supply chain vulnerabilities impacting commercial availability if not adequately managed [S1].

- Compliance Complexity: The company navigates extensive U.S., EU regulations affecting marketing claims (prohibiting off-label promotion), pharmacovigilance obligations including Risk Evaluation Mitigation Strategies (REMS) or Risk Management Plans (RMPs), pricing transparency laws (Sunshine Act), anti-kickback statutes among others which collectively increase compliance costs and litigation exposure risk ,,[S20].

- Pricing Pressures: Healthcare policy reforms globally impose downward pressure on reimbursement prices through government negotiations like the Inflation Reduction Act's Medicare Drug Price Negotiation Program or health technology assessments affecting product profitability [S9],[S19].

- Market Size: Small patient populations limit peak sales potential despite high unmet need; payer coverage policies may restrict access or impose step edits limiting usage [S21].

- Financing Needs: Given ongoing losses despite margin improvements additional capital raises may dilute shareholders or increase debt burdens constraining financial flexibility [S6].

What To Watch Next (Analysis)

Key milestones include:

- Clinical trial readouts particularly Phase 3 outcomes for brelovitug impacting future launch timing;

- Progress/regulatory feedback on volixibat's dossier influencing label extension opportunities;

- Resolution or progress updates regarding Livmarli patent litigations impacting generic competition timelines;

- Expansion of commercial geography through partnerships or direct investment assessing cost-benefit tradeoffs;

- Evolving payer coverage/reimbursement policies under healthcare reform affecting realized price points.

Near-term quarterly earnings will be informative about whether the strong operating cash flow trajectory sustains alongside narrow net losses supporting longer-term path toward profitability [N1],[N2],[N3].

Conclusion

Mirum Pharmaceuticals represents a focused yet complex biopharmaceutical player intensely devoted to rare disease therapies. Strong growth emanates from its proven orphan drug portfolio combined with strategic acquisitions that bolster breadth across hepatology-related indications. While profitability remains elusive due to persistent operating investments coupled with legal defense obligations against patent challenges improving margins highlight scalability benefits beginning to emerge. The robust shift into positive cash flow underscores operational progress enabling pipeline funding without excessive capital deployment. However significant regulatory surveillances including litigation risk coupled with challenging reimbursement landscapes temper near-term visibility beyond incremental indication advances. Ultimately Mirum’s evolution will depend heavily on execution strength progressing advanced clinical candidates complemented by judicious geographic expansion within highly specialized medical communities treating these ultra-orphan conditions.

This analysis is based solely on publicly available information through official filings as of February 26th, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments