Hamilton Beach Brands’ Transition: Growth Setbacks and Health Segment Integration

Hamilton Beach Brands is adapting its portfolio through health-tech acquisition amid recent declines in revenue and operating cash flow.

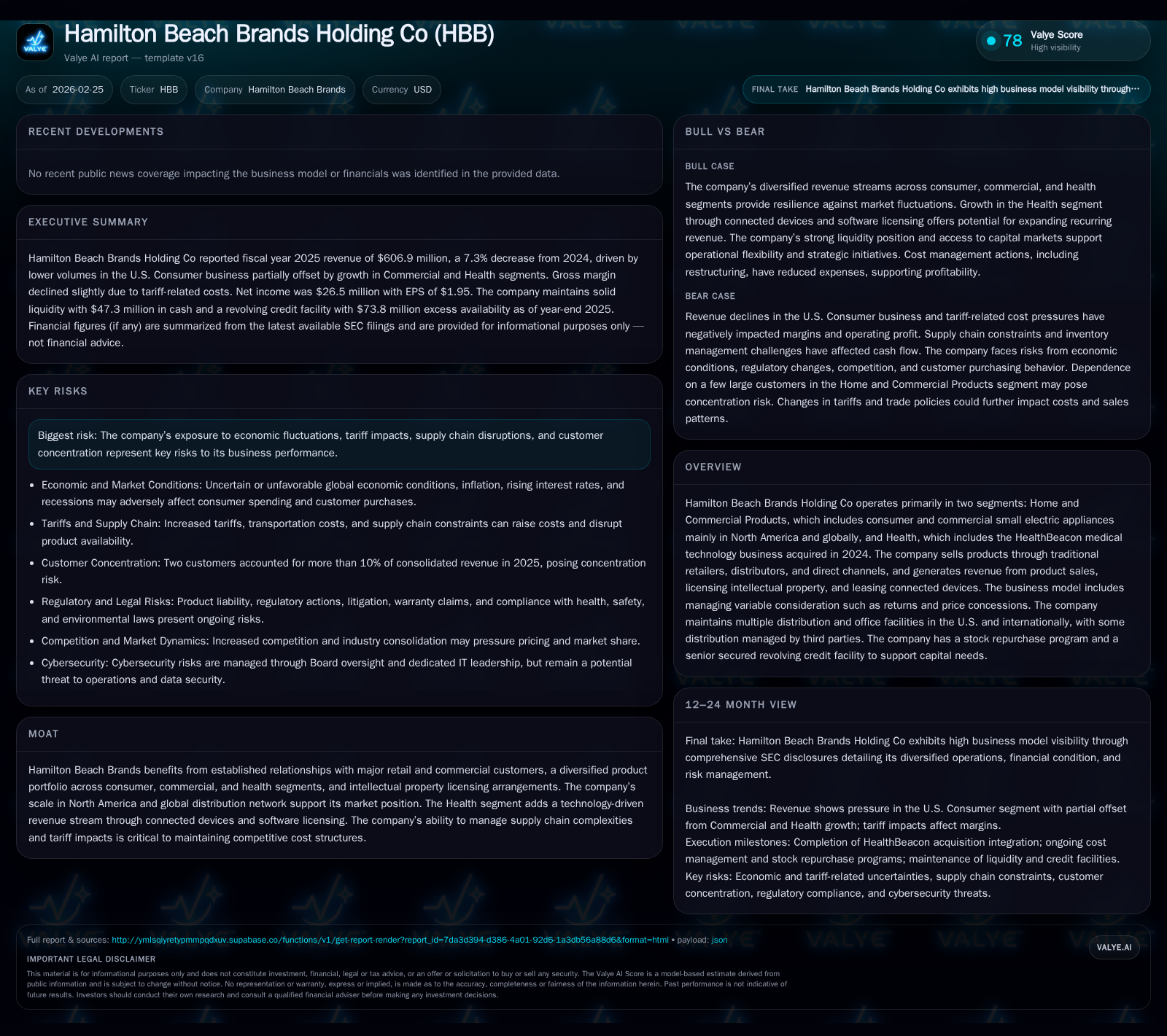

Hamilton Beach Brands experienced a notable revenue contraction of 7.3% in fiscal 2025 following years of steady growth, driven largely by headwinds in its traditional Home and Commercial Products segment. The integration of the HealthBeacon acquisition introduces a technology-based revenue stream via connected healthcare devices, signaling a strategic pivot toward diversified growth areas. Despite margin compression and working capital challenges impacting operating cash flow, the company maintains solid liquidity supported by a senior secured revolving credit facility while balancing capital returns through dividends and share repurchases. Future performance hinges on successful Health segment expansion and resolution of supply chain and tariff pressures.

Revenue and Profit Trajectory: Historical Performance Through 2025

Hamilton Beach Brands' growth trajectory over the last half-decade highlights early robust expansion followed by a marked slowdown in fiscal 2025. Revenues more than tripled from approximately $205 million in FY2019 to peak at about $655 million in FY2024, fueled by strong demand for its core small electric appliance products across consumer and commercial channels [F1]. However, this momentum reversed sharply with total sales falling to roughly $607 million in FY2025 — a decline of 7.3%. Operating income similarly contracted by 15.3%, ending the year at roughly $36.6 million versus over $43 million a year prior [F1]. Net income dropped by 14% to just under $26.5 million [F1]. This pattern reflects margin compression stemming from multiple cost pressures alongside weakening end-market demand.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 607 | 26 | 14 | 37 | -7.3% | -14.0% |

| 2024 | 655 | 31 | 65 | 43 | +21.9% | |

| 2023 | 25 | 89 | 35 | -0.1% | ||

| 2022 | 25 | 39 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 9 | 11 |

| 2024 | 6 | 14 | 62 |

| 2023 | 6 | 3 | 85 |

| 2022 | 6 | 3 |

Source: SEC companyfacts cache [F1].

This rapid deceleration after prolonged growth underscores emerging operational challenges, including supply chain disruptions and tariff-induced cost inflation that increasingly squeezed profitability.

Analyzing Segment Contributions: Home & Commercial vs. New Health Business

Hamilton Beach Brands generates its revenue through two primary segments: the longstanding Home and Commercial Products division, which offers small electric appliances mainly in North American consumer and commercial markets, and the recently established Health segment brought into the fold following the acquisition of HealthBeacon medical technology business in mid-2024 [S1,S8].

The Home & Commercial segment remains the dominant contributor but has been pressured by softer retail demand and channel shifts towards variable consideration management including returns and price concessions [S1]. The new Health segment delivers technology-enabled revenue streams through leasing connected healthcare devices as well as software licensing, representing an important strategic diversification beyond conventional product sales [S1]. While still nascent, this addition could unlock recurring revenues less sensitive to traditional appliance market volatility.

Drivers Behind the Revenue Decline and Margin Compression

Several interconnected factors drove Hamilton Beach's revenue decline and narrowing margins in FY2025:

- Supply Chain Strains: Tariff costs led to elevated inventory values requiring early Q1 purchases; however, slower-than-expected turnover slowed downstream purchasing causing cascading payables effects [S6].

- Variable Consideration Management: Increasingly dynamic pricing concessions, promotional incentives, and return allowances complicated transaction price realization, diluting reported revenues [S1,S6].

- Consumer Demand Weakness: Market saturation and macroeconomic fluctuations dampened sales volumes particularly for legacy small appliances within mature North American retail channels [S1].

- Cost Inflation: Escalating input costs from tariffs compressed gross margins directly impacting operating profitability.

This combination of tariff-induced cost inflation together with channel pressure on pricing created a tougher environment for maintaining previous margin levels.

Operational Cash Flow Challenges Amid Inventory and Tariff Pressures

Operating cash flow deteriorated significantly during FY2025, plunging almost 79% year-over-year to just under $13.8 million from upwards of $65 million previously [F1]. This sharp pullback owes principally to growing inventory balances inflated by tariff costs combined with changes in accounts payable management reflecting lower inventory-related purchasing activity later in the year [S6].

The elongation of the cash conversion cycle amid these factors undermined liquidity generation despite stable underlying earnings figures.

HealthBeacon Acquisition: A Strategic Shift with Technology-Driven Growth Implications

In late 2024, Hamilton Beach expanded into healthcare technology via acquisition of HealthBeacon, adding connected device leasing alongside associated software licensing mechanisms [S1]. This move reflects an explicit strategy to diversify beyond traditional small electric appliances into higher-margin, technology-enabled recurring revenue sectors.

Though currently contributing modestly due to early integration stages, the Health segment promises structural advantages including leveraging platform-based device maintenance contracts that could stabilize future cash flows.

Capital Structure, Liquidity, and Debt Facilities Overview

Hamilton Beach maintains a prudent capital structure anchored by a senior secured revolving credit facility totaling $125 million that matures in December 2029 . As of December end-2025, borrowings stood at around $50 million against an available borrowing base near $124 million leaving significant unused capacity ($74 million) [S4,S11,F1]. The facility accrues interest at floating rates hedged partially through interest rate swap agreements fixing cost below market volatility [S4,S7,S11].

Current ratio approximated a healthy 2.47x due to strong current assets positioning despite heightened inventory levels [F1], affirming adequate liquidity coverage for operating requirements.

The company was compliant with all financial covenants under its credit facility as of December 31, 2025 [S12].

Capital Allocation Priorities: Dividends, Share Repurchases, and Reinvestment

Amid cash flow pressures, management exhibited disciplined capital allocation maintaining dividends steady at approximately $6.4 million for fiscal year-end 2025 with a reduction in share repurchase activity down from approximately $14.1 million spend in FY2024 to about $9 million in FY2025 [F1,S14,S26,S29].

Capital expenditures remained modest near $2.8 million reflecting measured reinvestment aligned with operational scaling plans [F1]. This cautious approach evidences prioritization of shareholder returns tempered by conserving liquidity amid transitional headwinds.

Outlook and Key Monitorables for Future Growth Trajectories

Looking ahead absent explicit forward guidance from company disclosures, key investor focus should center on several critical junctures:

- Progress integrating HealthBeacon operations into consolidated financials accelerating technology-enabled revenue mix.

- Resolution of supply chain inefficiencies especially inventory turnover improvements mitigating cash flow strain.

- Recovery trajectories for profit margins as tariff impacts potentially recede or are passed through pricing mechanisms.

- Working capital optimization reducing cash conversion cycle duration may unlock incremental liquidity enhancing financial flexibility.

- Monitoring covenant compliance under revolving credit facility ensuring access to undrawn borrowing capacity during ongoing transition.

The interplay of these operational variables alongside broader economic conditions will shape Hamilton Beach’s ability to restore historic top-line momentum while harnessing new growth vectors introduced through its health sector diversification.

Disclaimer: This analysis is based entirely on publicly disclosed information as cited without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments