Hepion Pharmaceuticals Shifts Focus Toward Liver Disease Diagnostics Amid Funding Strains

The company’s latest quarterly report reveals a strategic pivot from clinical-stage therapeutics to diagnostics driven by capital limitations and new licensing agreements.

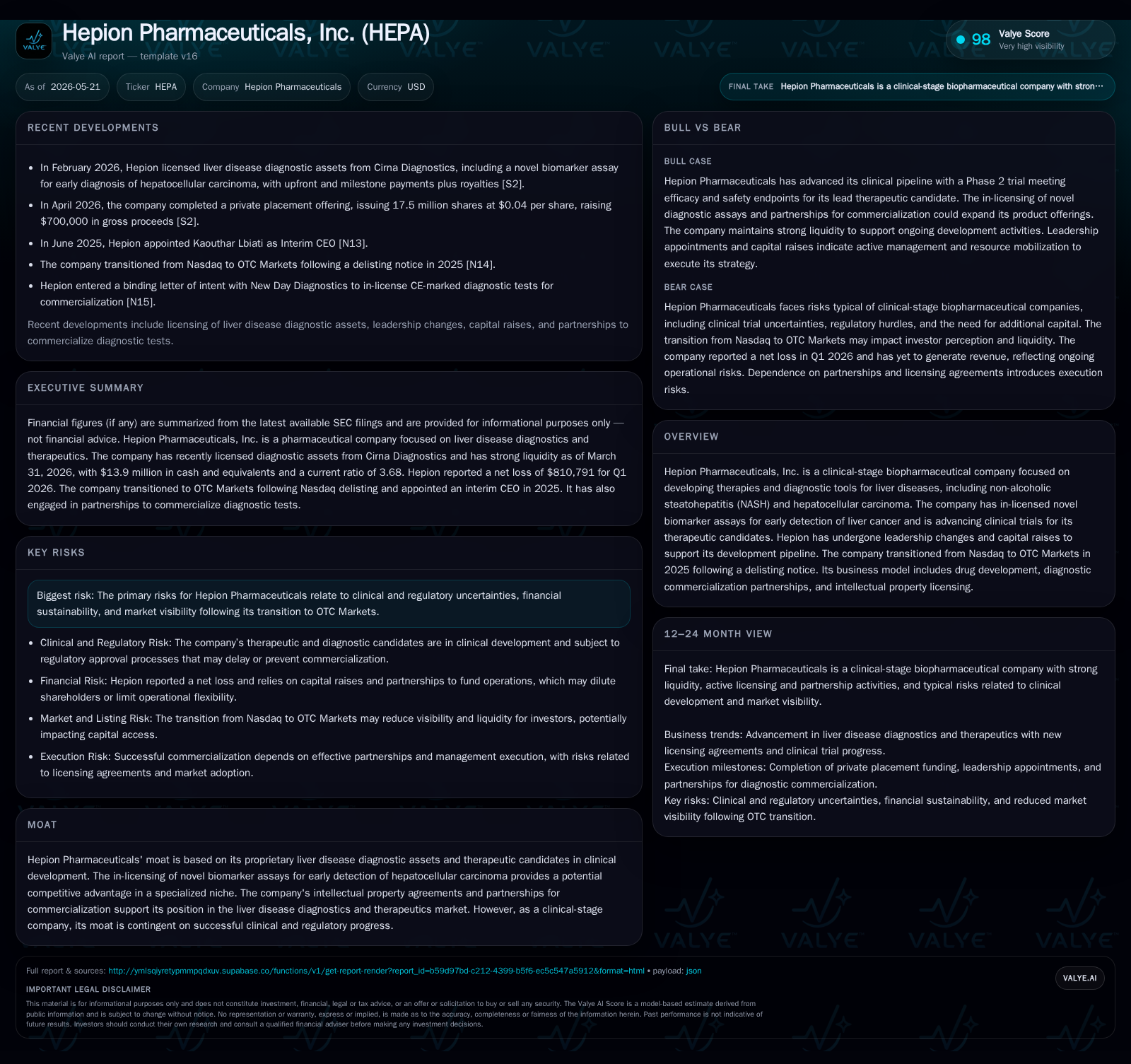

Hepion Pharmaceuticals’ May 2026 10-Q filing underscores an operational slowdown in its ASCEND-NASH trial due to funding shortages, simultaneously spotlighting recent intellectual property licensing deals targeting liver disease diagnostics. These developments reflect a deliberate shift from costly drug development toward leveraging proprietary biomarker assays for hepatocellular carcinoma detection. The company faces persistent financial challenges, with cash runway extending only into Q3 2026 despite recent capital raises. Hepion’s competitive positioning hinges on its novel diagnostic assets and partnerships, but significant risks remain tied to clinical progress, regulatory approvals, and liquidity.

Recent Quarterly Developments Signal Operational Shift

Hepion Pharmaceuticals’ latest quarterly report filed on May 14, 2026, reveals a significant operational slowdown in its ASCEND-NASH clinical trial activities attributable to constrained capital availability [S2]. The company confirmed completion of wind-down activities in the trial’s prior phases — originally halted in mid-2024 due to funding inadequacies — effectively marking cessation of therapeutic R&D efforts in the near term. Concurrently, Hepion executed securities purchase agreements on April 21, raising approximately $700,000 in gross proceeds via issuance of common stock at $0.04 per share [S3], a modest infusion insufficient on its own to resume intensive clinical development. Leadership changes have also unfolded: founder CEO Kaouthar Lbiati resigned in March 2026 for personal reasons, with Gary Stetz appointed interim CEO shortly thereafter alongside new board members [S16, S18]. This suite of events underscores a material strategic pivot emphasizing diagnostics licensing and asset commercialization over costly drug trials.

The absence of material risk factor changes in this quarter underlines continuity concerns about financial sustainability. The reported plans reflect recalibrated priorities toward preserving cash and focusing on intellectual property licensing opportunities rather than pursuing full-scale drug candidate development [S2]. Management commentary within filings suggests that these shifts respond directly to the near-term cash runway constraints that threaten going concern status.

Hepion's Business Model: From Therapeutics to Diagnostics

Historically centered on advancing rencofilstat (CRV431), a cyclophilin inhibitor molecule aimed at multiple chronic liver diseases including NASH and hepatocellular carcinoma (HCC), Hepion’s business model has fundamentally shifted towards diagnostic innovation [S1]. The company monetizes through a dual approach: internal drug candidate development balanced with intellectual property licensing agreements that grant milestone payments and royalties.

February 2026 marked a key milestone with an IP license acquisition from Cirna Diagnostics LLC granting rights to proprietary liver disease diagnostic assays including a mutant tumor RNA biomarker for early HCC detection [S16]. Payment obligations include an upfront fee ($50,000), patent expense coverage, up to $2.35 million in developmental milestones, plus sales-related milestones reaching $4.5 million and ongoing royalties in the low single digits upon commercialization [S16]. Earlier licensing deals with New Day Diagnostics broadened Hepion’s test portfolio to include assays for celiac disease and respiratory multiplex testing alongside HCC diagnostics [S1].

Revenue generation hinges heavily on achieving regulatory approvals and market adoption for these diagnostic products rather than imminent pharmaceutical sales. Given its clinical-stage status with halted therapeutics trials, immediate revenue streams remain elusive — highlighting dependence on partnering/licensing milestones. The business model involves careful cost management of patent/licensing fees against prospective royalty income buffered by judicious capital deployment during this transitional phase.

Competitive Dynamics in Liver Disease Diagnostics and Therapeutics

Hepion operates within the intersecting sectors of specialty biopharma therapeutics and medical diagnostics targeting complex liver diseases characterized by pronounced unmet needs. Clinical-stage biotech faces typical hurdles: protracted FDA regulatory pathways for drugs and diagnostics alike; intense scientific validation demands; variable payer reimbursement landscapes; and high capital intensity.

In liver disease diagnostics specifically, competition derives from next-generation biomarker innovations versus established imaging or biopsy modalities. Success requires demonstrable improvements in sensitivity/specificity coupled with integration into clinical workflows supported by physicians and payers. Pricing power is muted absent proven outcomes data; moreover, switching costs for hospitals or labs are nontrivial owing to regulatory validations required for new assays.

Peer companies often juggle similar portfolios balancing pipeline therapeutics with diagnostic adjuncts — yet many remain years away from commercial launches. Hepion’s recent license acquisitions position it distinctively within a niche focused on early HCC detection via circulating tumor RNA biomarkers — an emerging domain promising enhanced prognostic value but still needing robust external validation.

Growth Catalysts Rooted in Biomarker Innovation

Key growth determinants for Hepion encompass clinical trial progress resumption should capital permit; obtaining CE mark expansions or FDA clearances that unlock broader commercial markets; and forging strategic partnerships bolstering distribution capabilities [S1]. Revenue upside depends materially on milestone achievements tied to regulatory advancements combined with escalating royalty flows from market penetration.

Enhancements in biomarker assay performance underpin commercial desirability—higher sensitivity/specificity benchmarks correlate directly with clinician uptake potential amidst increasing awareness of NASH/HCC prevalence globally. In parallel, expanding coverage among healthcare payers represents a critical lever given diagnostics reimbursement complexities in fragmented systems. Intellectual property milestones act as discrete catalysts potentially triggering accelerated cash inflows that can stabilize finances while scaling operations.

Risk Factors: Clinical, Financial, and Market Challenges

Hepion faces acute risks primarily related to continued clinical development uncertainty after halting the ASCEND-NASH trial due to funding shortfalls [S1]. Financially, accumulated deficits tallied $246 million as of end-2025 reflecting deep operating losses characteristic of early-stage biotech [F1]. Going concern apprehensions linger given projected cash depletion by Q3 2026 unless further equity infusions occur promptly [S1]. Prolonged reliance on milestone payments introduces revenue unpredictability tied tightly to partner success.

Market-wise monitoring assay adoption across fragmented healthcare ecosystems introduces execution risk compounded by competitive innovation accelerating alternative biomarker developments. Regulatory delays or failures would stall commercialization timelines critically constraining growth runway.

Key Milestones and What to Monitor Next

Investors should track announcements regarding potential recommencement or advancement of therapeutic trial activities if additional funding is secured — though current disclosures suggest deferred priorities there [S2]. Diagnostic-related catalysts include updates on clearance processes particularly FDA approval status beyond existing CE marks for select tests licensed from Cirna and New Day Diagnostics [S1,S16].

Partnership deal updates—new collaborations or expanded commercialization contracts—could enhance distribution reach while generating milestone revenue inflections. Leadership stability remains relevant given recent executive turnover influencing strategic continuity [S18]. Moreover, any subsequent financing events or amendments to securities purchase agreements will significantly impact cash runway projections.

SEC filings provide an ongoing window into corporate governance changes or financial strategy adjustments critical for assessing execution capability amidst evolving market conditions.

Financial Position Supports Near-Term Operations but Risks Remain

At quarter-end March 31, 2026, Hepion reported approximately $2.7 million in current assets against $0.7 million in current liabilities yielding a healthy current ratio near 3.68—a standard indicator reflecting sufficient short-term asset coverage over immediate obligations [F1]. Total debt is nominal relative to cash positions at about $176 thousand indicating limited leverage burden [F1].

Despite these metrics supporting operational capacity over ensuing quarters, disclosures explicitly warn that available cash resources will be exhausted during Q3 2026 absent further capital injections [S1]. The recent private placement providing gross proceeds of $700 thousand extends runway marginally but falls short of long-term sustainability requirements without fresh financing efforts [S3,S18].

Therefore, while balance sheet health is passable currently with conservative liabilities levels underpinning solvency, the near-term path remains contingent upon executing equity offerings or other funding mechanisms vital for maintaining research activities and corporate viability.

This analysis consolidates the latest public filings complemented with sector-focused interpretation grounded exclusively on verifiable company disclosures without forward-looking conjecture or investment research views.

Financial position in context

Current assets of $3mm and current liabilities of $735572 imply a current ratio near 3.68x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments