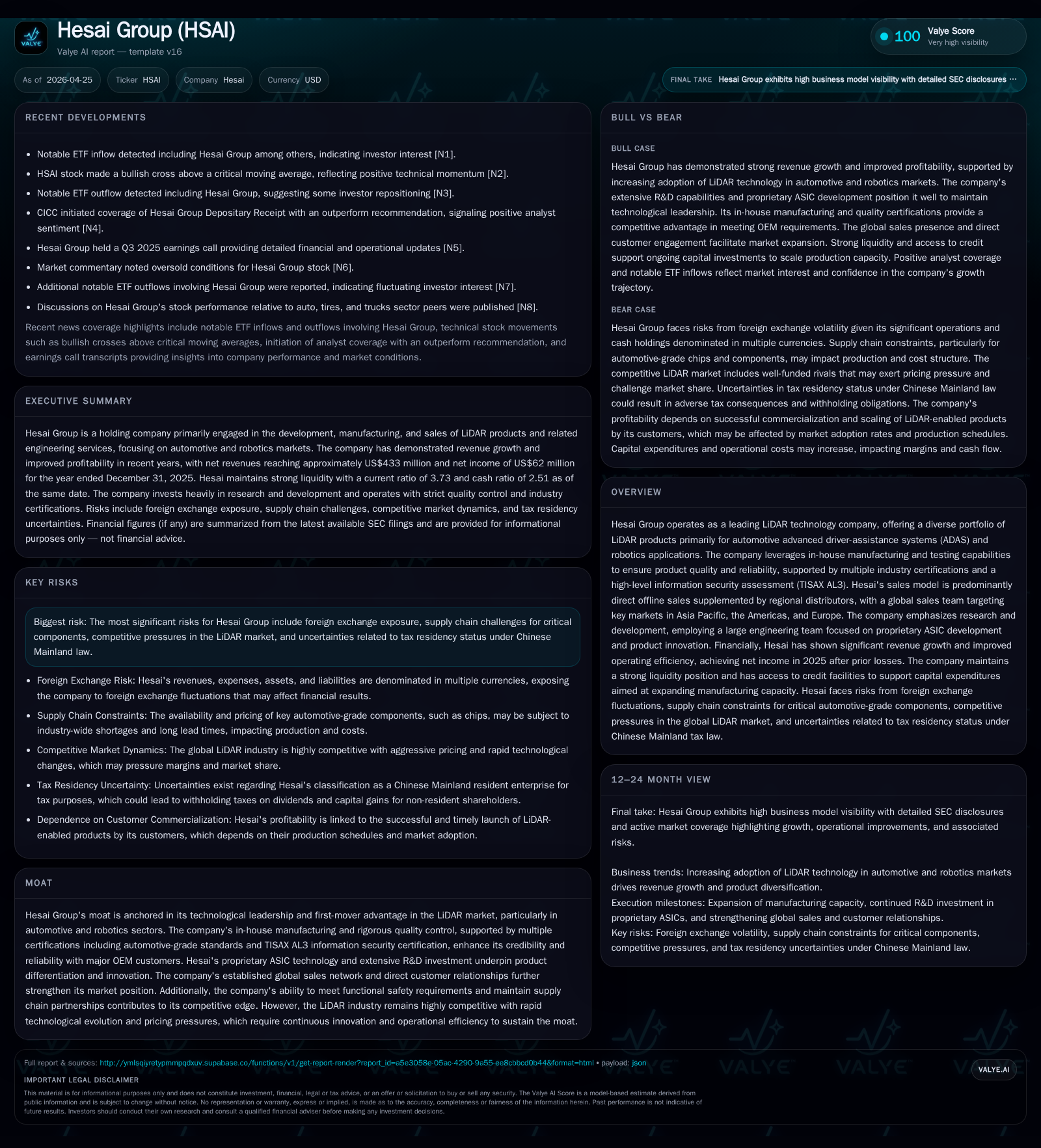

Hesai Group Expands LiDAR Shipments and Achieves Profitability on Scale and Innovation

Hesai Group’s 2025 performance underscores its leadership in automotive and robotics LiDAR through volume growth, technological edge, and cost optimization.

In its latest quarter and full-year 2025 disclosures, Hesai Group reported a sharp surge in shipped LiDAR units, driving a 45.8% revenue increase and returning to net profitability after prior losses. The company’s vertically integrated manufacturing, proprietary ASIC design, and rigorous quality controls support its competitive moat in the early-stage but fast-growing LiDAR markets for ADAS and robotics. Going forward, Hesai faces cyclical risks from pricing pressures and supply chain volatility but benefits from structural growth driven by increasing LiDAR adoption in multiple end markets and ongoing product innovation. Monitoring customer production ramp-ups, margin sustainability, and capacity expansion pacing will be critical execution points.

Recent Operating Update

Hesai Group's latest quarterly filing dated April 24, 2026 ([S2]) reconfirms the company's continuing trajectory of rapid commercialization of its LiDAR solutions globally. In full-year 2025, Hesai recognized revenues of RMB3.03 billion (US$432.9 million), marking a robust increase of 45.8% compared to RMB2.08 billion in 2024 ([S1]). This surge was powered by shipment volumes scaling up substantially to approximately 1.62 million units from just over 500,000 units the prior year — a more than threefold increase. Notably, this volume ramp culminated in a net income turnaround to RMB436 million (US$62.3 million), reversing losses reported in both 2023 and 2024.

This recent disclosure highlights two critical shifts shaping Hesai’s near-term story: accelerated adoption by automotive customers ramping ADAS deployments at scale, and improved operating leverage leveraging extensive vertical integration plus ASIC-driven product innovation that tightens cost control despite pricing pressures.

Business Model

Hesai operates primarily as a technology manufacturer developing advanced three-dimensional LiDAR sensors used in multiple segments: passenger/commercial vehicles with advanced driver-assistance systems (ADAS) and autonomous/robotic platforms such as logistics robots or last-mile delivery machines ([S1]). Its revenue primarily stems from sales of these LiDAR hardware products alongside engineering services including design validation.

The company’s differentiation arises from several pillars:

- Proprietary ASIC development enabling tighter integration and performance customization.

- In-house manufacturing coupled with rigorous quality control meeting automotive industry grade standards including functional safety compliance.

- Multiple certifications including TISAX AL3 information security certification adding credibility for automotive OEM contracts.

- A broad portfolio tailored for different end-markets allowing pricing diversification — ADAS products generally command lower average selling prices while Robotics solutions have higher ASPs reflecting specialized application needs ([S4], [S9]).

Sales are primarily conducted through direct offline channels supported regionally by distributors across Asia Pacific, the Americas, and Europe ([S20]). Customer relationships focus heavily on OEMs whose production schedules directly influence Hesai’s shipment volumes and profitability. Retaining OEM trust facilitates expansion into additional vehicle models.

Industry Structure and Competitive Position

The global LiDAR market remains at an early stage characterized by rapid technological development, fragmented competition with many emergent players ranging from Tier 1 suppliers to dedicated sensor companies (5[S1], [S11]). Hesai asserts leadership through its first-mover advantage especially within China's domestic market where it combines early R&D investments with advanced mass production capability.

Competitors often utilize aggressive pricing strategies or benefit from larger financial resources or established automotive relationships forcing Hesai into continuous innovation cycles to maintain differentiated performance versus cost trade-offs ([S11], [S24]). The company’s platform approach — reusing core components across product lines — enhances its ability to scale manufacturing efficiently while controlling costs ([S4]).

However, the evolving global regulatory environment around foreign investment security reviews particularly in China introduces operational sensitivities affecting cross-border expansions ([S18]). Currency fluctuations also expose margins due to substantial sales denominated in Renminbi but bearing costs or financing obligations tied to U.S. dollars ([S7]).

Growth Drivers and Constraints

Drivers

- Structural market expansion: Increasing penetration of LiDAR sensors in both ADAS-equipped vehicles globally and industrial/autonomous robotics fuels foundational demand growth.

- Technological innovation: Hesai’s sustained R&D investment (~26–42% of revenues historically) supports continuous product iteration enhancing detection range, resolution, reliability or power efficiency — features prized by OEMs ([S14]).

- Manufacturing scale economies: Vertical integration reduces dependency on external suppliers for key components reducing lead times and manufacturing costs per unit alongside automation progress.

- Diversified geographic footprint: Expansion beyond China into mature automotive and robotics markets in Americas/Europe broadens addressable opportunity sets while offsetting region-specific regulatory/taxation risks.

Constraints

- Pricing pressure & mix shift: ADAS segment commands lower average prices compared to robotics; rising sales here dilute average selling price but reflect higher volume leverage potential ([S24]).

- Raw material/component scarcity: Strategic inventory management attempts to mitigate disruption risk yet issues like automotive-grade chip shortages risk input cost spikes or delivery delays ([S1]).

- Capital-intensive capacity build-out: Manufacturing facility expansions entail upfront fixed costs with ramp-up periods critical for realizing scale benefits but subject to schedule slippage ([S11], [S22]).

- Foreign exchange risk: Substantial Renminbi revenue vs U.S.-denominated borrowing or cash-exposure creates earnings volatility amid currency fluctuations ([S7], [F1]).

- Regulatory & geopolitical complexities: Foreign investment security reviews under Chinese law add uncertainty to offshore holding structures affecting capital flows or operational flexibility ([S18]).

What to Watch Next

Investors should monitor quarterly shipment volume trajectories as proxies for OEM production ramp-ups especially in ADAS programs which tend to follow vehicle model launch cycles. Tracking gross margins will signal if Hesai can sustain cost discipline amid raw material inflation or pricing competition. Implementation pace of factory expansions will impact future capacity availability; delays there could bottleneck growth ambitions.

New design wins or collaborations announced would provide forward visibility on revenues given long lead times between evaluation & mass production phases for automotive sensors. Additionally, changes in foreign exchange trends or updates on tax residency status under Chinese Mainland law may materially influence reported earnings or cash repatriation abilities.

Financial Profile

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 62 | 17 | 24 | 44 | +544.4% |

| 2024 | -14 | 9 | -28 | 36 | +79.1% |

| 2023 | -67 | 8 | -81 | 57 | -53.7% |

| 2022 | -44 | -101 | -55 | 34 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -28 | 4.9 |

| 2024 | -27 | -2.6 |

| 2023 | -49 | -12.3 |

| 2022 | -134 | 9.6 |

Source: SEC companyfacts cache [F1].

The annual financial summary extracted from the latest filings confirms substantial progress toward profitability alongside scaling top-line results:

|

| FY | Revenue (RMB Mil) | Op Income (USD Mil) | Net Income (USD Mil) | CFO (USD Mil) | Capex (USD Mil) | Equity (USD Mil) | Op Income YoY % | Net Income YoY % | CFO YoY % |

|---|---|---|---|---|---|---|---|---|---|

| 2023 | 1,877 | -80.5 | -67.0 | 8.1 | 57.3 | 544 | - | - | - |

| 2024 | 2,077 | -28.1 | -14.0 | 8.7 | 35.6 | 539 | +65% | +79% | +7.7% |

| 2025 | N/A* | +24.1 | +62.3 | 16.7 | 44.2 | 1281 | +186% | +544% | +92% |

Hesai’s operating income turned positive with US$24 million recorded for FY2025 compared to negative US$28 million prior year indicating improved operational efficiency despite increased R&D investments (US$114 million) mainly focused on ASIC development ([S14]). Free cash flow remains negative given capital expenditures exceeding operating cash flow by approximately US$27 million; however, healthy cash reserves (US$238 million) support further capacity investments without immediate liquidity concerns ([F1]).

Overall return on equity was approximately 4.9%, demonstrating first signs of translating technological leadership into shareholder value after steep initial investments fence-posted during commercial scale-up phases.

Conclusion

Hesai Group emerges as a robust participant in the expanding LiDAR ecosystem supporting next-generation mobility through strategic technological control complemented by manufacturing scale advantages that enable competitive positioning across diverse end markets globally. While risk factors inherent to young high-tech hardware industries persist—including supply chain volatility, price compression risks, regulatory complexities—Hesai's demonstrated volume ramp-up combined with sustained innovation forms a compelling blueprint for continued growth.

Monitoring execution against capacity expansion plans alongside margin trends will frame the near-term outlook while regulatory developments around Chinese offshore tax residency will bear watching given potential implications for capital structuring.

Disclaimer: This analysis is intended solely for informational purposes reflecting publicly available data as of the filing dates cited herein without any investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments