IBM Expands AI and Hybrid Cloud Leadership in Q1 2026 Earnings

Q1 2026 results underline IBM's growing strength in hybrid cloud and AI software as key revenue segments accelerate.

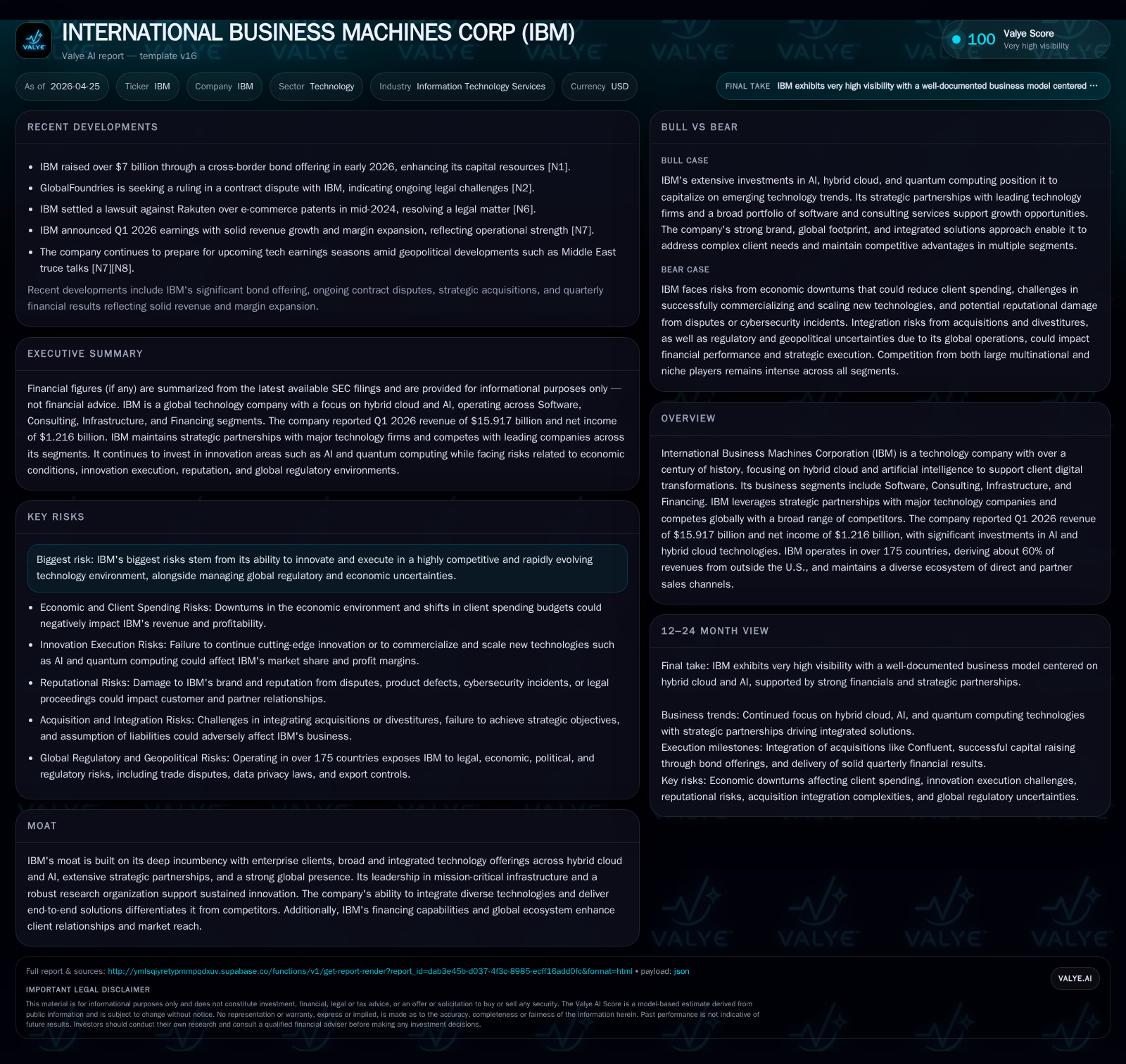

IBM reported a solid first quarter in 2026 with total revenue of $15.9 billion, driven by double-digit growth in hybrid cloud and automation software. Its integrated business model, combining software, consulting, infrastructure, and financing, continues to leverage deep enterprise incumbency and strategic partnerships. Market dynamics favor IBM’s end-to-end hybrid cloud and AI offerings, though competitive pressures and macroeconomic risks persist. The company maintains a strong global footprint with significant investments in innovation while prudently managing its balance sheet amid high leverage.

Q1 2026 Operating Highlights: Growth in Key Segments

In its latest quarterly filing dated April 23, 2026 [S2], IBM disclosed revenue of $15.917 billion for Q1—up roughly 9.5% year-over-year from $14.541 billion in the same period last year [S13]. Notably, software revenues reached $7.052 billion, climbing over 11%, fueled by strength in hybrid cloud ($1.905 billion vs. $1.687 billion) and automation ($1.741 billion vs. $1.584 billion) [S2]. These segments reflect IBM’s strategic focus on enabling enterprises to modernize application fleets and automate digital workflows via AI-enhanced platforms.

Consulting revenues also expanded to $5.272 billion (+4%) led by strategy & technology services ($2.896B) and intelligent operations ($2.376B), indicating broader client investments in transformation projects anchored by AI-driven insights [S2]. Infrastructure revenues showed meaningful growth as well, with hybrid infrastructure reaching $2.108 billion versus $1.646 billion previously—a clear sign of success penetrating hybrid cloud infrastructure deployments tailored for mission-critical workloads [S13].

The recent event filing on April 22 [S3] reaffirmed management's commitment to scaling these core businesses amid evolving market demands, citing ongoing investments into AI capabilities integrated across offerings.

This operational momentum matters as it validates IBM’s pivot toward higher-margin software and consulting services while building stickier client relationships through infrastructure solutions designed specifically for complex enterprise environments reliant on data security and scalability.

Business Model and Quality of IBM’s Technology Offerings

IBM operates a multi-segment business model encompassing Software (hybrid cloud platforms, AI tools), Consulting (digital transformation advisory), Infrastructure (servers, storage tailored for hybrid deployments), and Financing (client purchase facilitation) [S1], [S6]. This blend enables the company to address digital transformation end-to-end—spanning technology integration to business process reengineering.

Central to this model is IBM’s hybrid cloud platform combined with artificial intelligence modules that help clients reimagine workflows at scale across public clouds, private clouds, and on-premises systems [S21]. Unlike hyperscalers that offer primarily public cloud services or software vendors offering point solutions, IBM provides a tightly integrated stack with a heavy focus on regulated industries requiring security, compliance, and operational resilience.

The quality of IBM’s technology lies not only in foundational research backing its software innovations—a result of one of the world’s leading corporate research organizations—but also in its capacity to tailor solutions leveraging its deep incumbency within large enterprises globally. These enterprises often face high switching costs due to entrenched infrastructures embedded over decades.

Further enhancing value delivery is IBM’s expansive ecosystem which includes partnerships with Adobe, AWS, Microsoft, Oracle among others; these collaborations enable hybrid architectures orchestrating multi-vendor environments critical to clients’ agility goals [S21]. Additionally, IBM’s financing segment smooths acquisition hurdles for customers by providing credit facilities structured around hardware/software bundles—preserving deal flow momentum.

Competitive Position within the Hybrid Cloud and AI Landscape

Operating amid fierce competition from Amazon AWS, Microsoft Azure (especially on hybrid solutions like Azure Arc), Oracle Cloud Infrastructure (OCI), Salesforce (in CRM/automation), Alphabet (Google Cloud), and specialist players such as Splunk or Palo Alto Networks positions IBM squarely in a dense but segmented battleground [S4],.

IBM differentiates itself through breadth—offering integrated software for transaction processing combined with consulting-led digital strategy execution backed by proprietary infrastructure optimized for enterprise-grade workloads [S14]. Its recognized brand legacy engenders trust crucial in sectors like government and financial services that demand compliant solutions beyond raw performance benchmarks.

While hyperscalers aggressively pursue scalability through vast public clouds, IBM targets multi-cloud orchestration covering private clouds plus edge computing—capitalizing on rising enterprise concern over data sovereignty and resiliency.

Innovation leadership remains key; IBM’s consistent R&D investment fuels new products notably quantum computing platforms on the horizon alongside advancements in responsible AI tooling designed to meet emerging regulatory frameworks around data ethics, [S11]. However, these advantages coexist with risks from nimble startups adopting disruptive open-source models potentially eroding niche markets.

Industry Drivers and Structural Constraints Impacting Demand

Structural demand is propelled by enterprises’ pressing need to integrate AI-driven analytics across hybrid environments as they overhaul legacy IT systems toward agile digital infrastructures at scale [S6], [N1]. Growth segments such as automated workflows respond directly to efficiency mandates post-global economic uncertainty triggered cyclical spending slowdowns remain a constraint impacting overall IT budgets periodically [S15].

Demand is further influenced by complex sales cycles typical of high-value B2B contracts involving system integrators or regulatory approvals especially outside the U.S.—where approximately 60% of revenues originate—amplifying geopolitical risks such as trade tensions or local data privacy regulations that may impose barriers or delays [S21], [S11].

Moreover, reliance on third-party distribution channels introduces ecosystem risk; failure by partners to adapt swiftly may limit channel effectiveness or delay deployment plans while increasing credit exposure within financing arms of the company [S5]. Cybersecurity remains an area where innovation must keep pace with threat sophistication as failures could irreparably damage reputation or lead to costly litigations impacting client retention [S25], [S22].

Future Catalysts and Potential Challenges to Watch

Key inflection points include ongoing scaling efforts within quantum computing commercialization—a frontier opportunity offering potential long-term differentiation—as well as expansions addressing emerging AI governance demands motivated by increasingly stringent global regulations affecting data usage practices [S1], [N14].

Additionally, the integration pace of newly acquired technologies into existing portfolio streams will test execution discipline alongside sustaining momentum amidst intensifying competitor adoption of generative AI technologies bolstered by substantial capital inflows.

Forward-looking indicators include contract renewal rates within consulting engagements tied directly to transformation budgets plus announcements around expanded partner ecosystems leveraging joint go-to-market synergies. Management commentary during earnings releases will be closely monitored for revisions regarding macroeconomic outlook sensitivity or shifts in capital allocation emphasis particularly around R&D or share repurchases given balance sheet commitments [S2], [N4].

The company must also navigate risks including regulatory scrutiny linked to international tax policies influencing profitability profiles or potential operational impacts stemming from environmental compliance costs – although currently considered manageable relative to peers given IBM’s robust governance protocols [S9], [S10].

Financial Overview: Balance Sheet, Cash Flow, and Profitability Trends

Historical performance (annual)

|

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 67.5 | 10.6 | 13.2 | 1091 | +7.6% | +75.9% |

| 2024 | 62.8 | 6.0 | 13.4 | 1048 | +1.4% | -19.7% |

| 2023 | 61.9 | 7.5 | 13.9 | 1245 | +2.2% | +357.7% |

| 2022 | 60.5 | 1.6 | 10.4 | 1346 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Div ($bn) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 6.3 | 12.1 | 32.4 |

| 2024 | 6.1 | 12.4 | 22.1 |

| 2023 | 6.0 | 12.7 | 33.3 |

| 2022 | 5.9 | 9.1 | 7.5 |

Source: SEC companyfacts cache [F1].

IBM concluded Q1 2026 with net income of $1.216 billion compared to $1.055 billion the prior year quarter demonstrating both top-line revenue growth and operational leverage effects driving margin expansion as reflected in solid cash flow generation reported by depreciation at $555 million plus amortization at $719 million supporting continued investment cycles [S2].

Cash and cash equivalents totaled approximately $10.8 billion at quarter-end while total debt stood near $66.3 billion resulting in net debt around $55.5 billion implying a leveraged capital structure consistent with long-term strategic investments balanced against dividend payouts approximating $6.3 billion annually supported by operating cash flows exceeding $13 billion per fiscal year recently recorded [F1], [S12].

Equity reached about $32.6 billion showing steady book value appreciation aligned with net income gains driving an approximate return on equity north of 32% based on recent annualized results signaling efficient capital employment despite elevated leverage metrics indicative of structural funding choices tied historically to acquisitions plus technology platform innovations fueling future growth potential—while also necessitating vigilant debt servicing capacity monitoring given macroeconomic cycle uncertainty inherent within the sector highlighted risks sections [F1], [S19].

In summary, IBM's financial profile supports ongoing strategic initiatives focused on high-growth AI/hybrid cloud software coupled with consulting-led transformations — enabling margin expansion opportunities offset partially by sustained capital expenditure levels committed towards product development plus prudent maintenance of customer financing programs essential for maintaining competitive positioning worldwide.

This analysis synthesizes publicly available SEC filings dated up through April 23–24 2026 together with corroborating news sources without speculative forward-looking assertions or investment guidance. This narrative aims solely to provide an informed industry perspective grounded strictly in disclosed facts about INTERNATIONAL BUSINESS MACHINES CORP’s current operating status and strategic positioning within its market environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments