Interpace Biosciences Recalibrates Growth Strategy Following Fiscal 2025 Results

Latest SEC filings reveal operational stabilization and strategic capital restructuring underpinning Interpace Biosciences’ outlook.

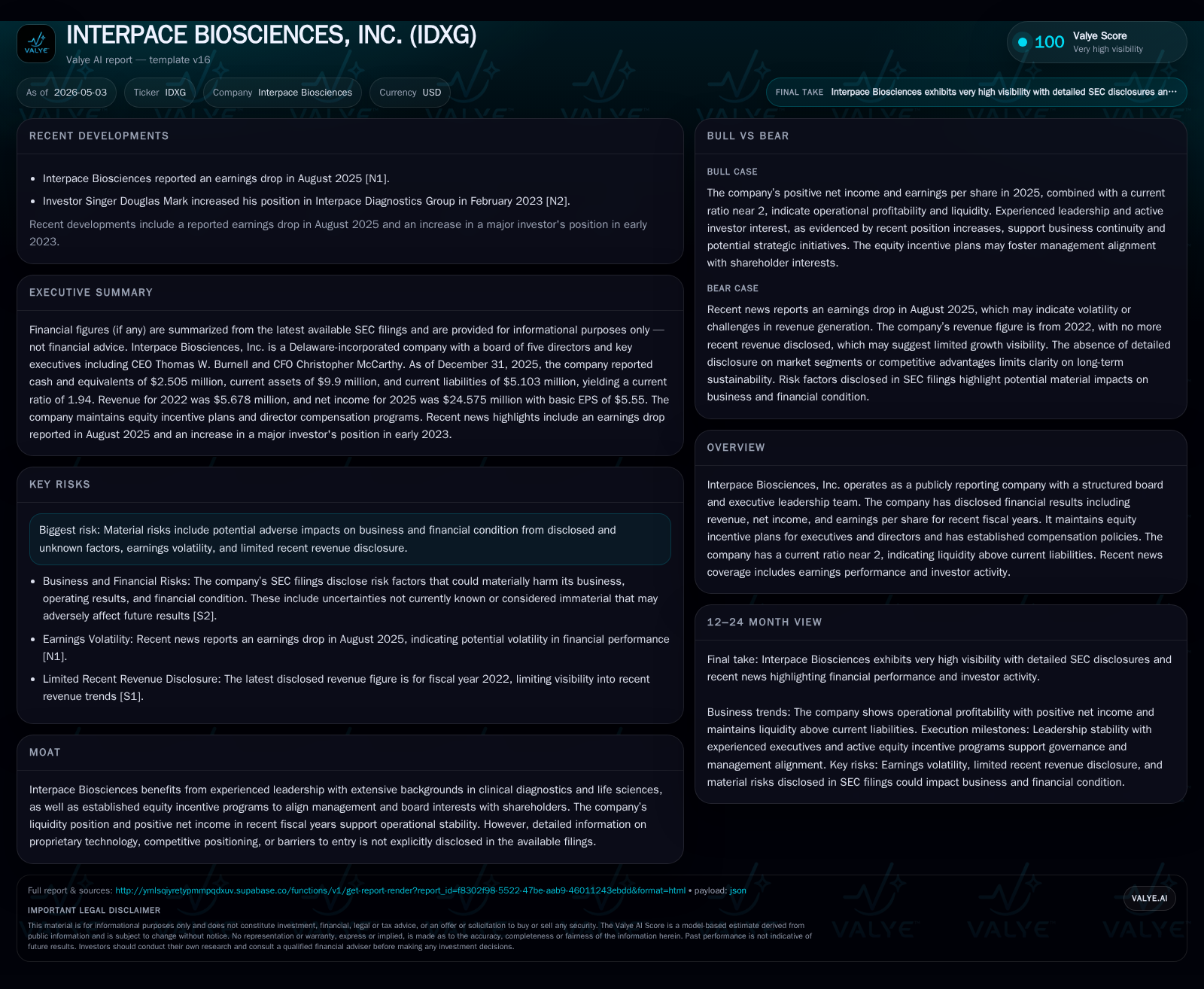

Interpace Biosciences’ recently filed 10-Q and 8-K documents for fiscal 2025 mark a pivotal step in clarifying its near-term operating and financial profile. The company completed conversion of all Series C Preferred Stock into common shares, simplifying its capital structure. Its diagnostic service business model focuses on proprietary molecular tests serving clinical pathology labs, supported by experienced leadership and equity incentive plans. While market demand shows promise amid evolving diagnostic needs, revenue visibility remains limited with risk factors emphasizing earnings volatility. Financially, Interpace maintains solid liquidity and manageable debt, positioning it to pursue growth opportunities contingent on execution fidelity and external reimbursement trends.

Latest Regulatory Filings Clarify Near-Term Operating Posture

Interpace Biosciences’ latest quarterly filing (Form 10-Q as of November 12, 2025 [S2]) provides the freshest formal update on the company's financials and risk disclosures ahead of fiscal year-end finalization. This is complemented by a March 30, 2026 current report (8-K) announcement disclosing the full fiscal-year-end results for December 31, 2025 [S3], alongside corporate actions such as the complete conversion of outstanding Series C Preferred Stock into common shares earlier that year [S7].

These filings collectively signal a recalibration in the company’s capital structure aimed at simplifying equity composition and potentially enhancing shareholder value by removing preferred stock layers.

Operationally, while detailed revenue figures are sparse—reflecting modest disclosure trends—the firm reports positive net income for FY 2025 [F1]. The new management disclosures underscore an emphasis on steady operational performance without reporting material deviations from prior quarters. Risk factors reiterated in the Q3 2025 filing caution about earnings volatility and potential unknown external threats [S2], consistent with an industry position still navigating growth phases.

Business Model Overview: Diagnostics with Clinical Impact and Quality Focus

Interpace Biosciences operates principally through providing proprietary molecular diagnostic testing services designed for specialized clinical decision-making. According to their latest annual amendment filing (10-K/A dated April 30, 2026 [S1]), revenue generation centers on delivering laboratory services that improve diagnostic accuracy on complex pathologies.

Customer segments primarily include hospitals, pathology laboratories, and specialists relying on advanced molecular insights to guide treatment. Their tests generally command premium pricing justified by expected higher specificity/sensitivity than traditional diagnostics.

The company emphasizes clinically validated workflows paired with rapid test turnaround times—key competitive differentiators in diagnostics where timeliness critically influences patient outcomes. This focus aligns the company strategically within the value chain as a provider of high-quality adjunct tests rather than commoditized panels.

Competitive Environment and Industry Positioning

The diagnostics sector is intensely competitive with multiple players ranging from large reference lab conglomerates to emerging biotech innovators. Interpace's filings do not assert a technological moat but highlight experienced leadership credentials as a stabilizing competitive parameter [S1]. The presence of structured equity incentive plans further aims to ensure strategic focus among executives and directors.

Pricing power is constrained by payer reimbursements and regulatory norms; thus, volume growth often hinges on broadening clinical adoption rather than raising prices materially. Regulatory oversight complicates entry yet also establishes quality thresholds that limit lower-cost entrants.

Industry adoption barriers include extensive validation requirements for new tests alongside entrenched physician ordering behaviors that require sustained education efforts. Consequently, diagnostic companies rely heavily on clinical utility data generation—a process both resource-intensive and iterative.

Catalysts for Growth: Incentives, Market Dynamics, and Operational Improvements

Interpace’s primary growth drivers involve expanding penetration of their diagnostic panels amid clinician preference shifts towards precision medicine paradigms. Equity-based compensation programs disclosed in their latest annual filing link management rewards to financial metrics such as revenue growth and adjusted EBITDA targets [S1], incentivizing performance aligned with shareholder interests.

Market dynamics include increasing prevalence of diseases requiring precise molecular characterizations—creating sustained demand ramps structurally distinct from cyclical healthcare spending patterns typically seen in elective services.

Operationally, potential margin enhancement could stem from scaling lab throughput efficiencies or optimized reagent procurement strategies. Additionally, monitoring shifts in reimbursement policies will be crucial as favorable coverage decisions can materially advance demand trajectories.

Risks and Constraints: Earnings Volatility and Revenue Visibility

Consistent across Interpace’s SEC risk disclosures (Q3 2025 Form 10-Q Item 1A Risk Factors) is the emphasis on earnings volatility stemming from limited revenue visibility [S2][S5]. The company admits exposure to multiple uncontrollable variables including payer reimbursement changes, competitive innovation pressures, regulatory interventions, or rapid testing technology commoditization.

The acknowledged "unknown factors" clause reflects prudence given ongoing sector flux. This lack of granular recent revenue data constrains the ability to definitively assess traction or underlying demand momentum post-2022 figures [F1].

Competitive forces compelling continuous innovation and cost discipline further temper margin expansion hopes absent clear-scale breakthroughs or exclusivity deals.

Key Metrics and What Investors Should Monitor Next

Going forward, stakeholders should track quarterly top-line updates for signals of accelerating test adoption or market share shifts as these metrics directly correlate with revenue momentum. Additional quantitative indicators include order volume growth metrics if disclosed alongside pricing trends.

Contractual wins or renewals with major pathology networks would also act as tangible evidence supporting scaling hypotheses. Management commentary regarding revised incentive program targets or explicit guidance adjustments can shed light on confidence levels concerning future performance.

Regulatory developments impacting coverage decisions or FDA/CLIA compliance issuances influencing test availability will be critical external catalysts warranting close observation.

Financial Snapshot: Liquidity, Profitability, and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3mm | |

| 2025-12-31 | ||

| Current assets | $10mm | |

| 2025-12-31 | ||

| Current liabilities | $5mm | |

| 2025-12-31 | ||

| Current ratio | 1.94x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Cash & Equivalents | $2.51 million | |

| 2025-12-31 | ||

| Total Debt | $1.75 million | |

| 2023-03-31 | ||

| Current Assets | $9.90 million | |

| 2025-12-31 | ||

| Current Liabilities | $5.10 million | |

| 2025-12-31 |

Interpace Biosciences sustains a current ratio of approximately 1.94 ([F1]), indicating readily available liquidity above short-term obligations—a positive signal amid ongoing investments in operational capabilities.

Total debt reported at $1.75 million (as of Q1 2023) relative to cash reserves suggests modest leverage allowing room for flexible capital deployment without immediate refinancing concerns ([F1]). The strategic conversion of preferred stock into common likely further enhances equity base clarity while mitigating dividend or redemption liabilities ([S7]).

This analysis summarizes publicly filed information up to May 2026 without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments