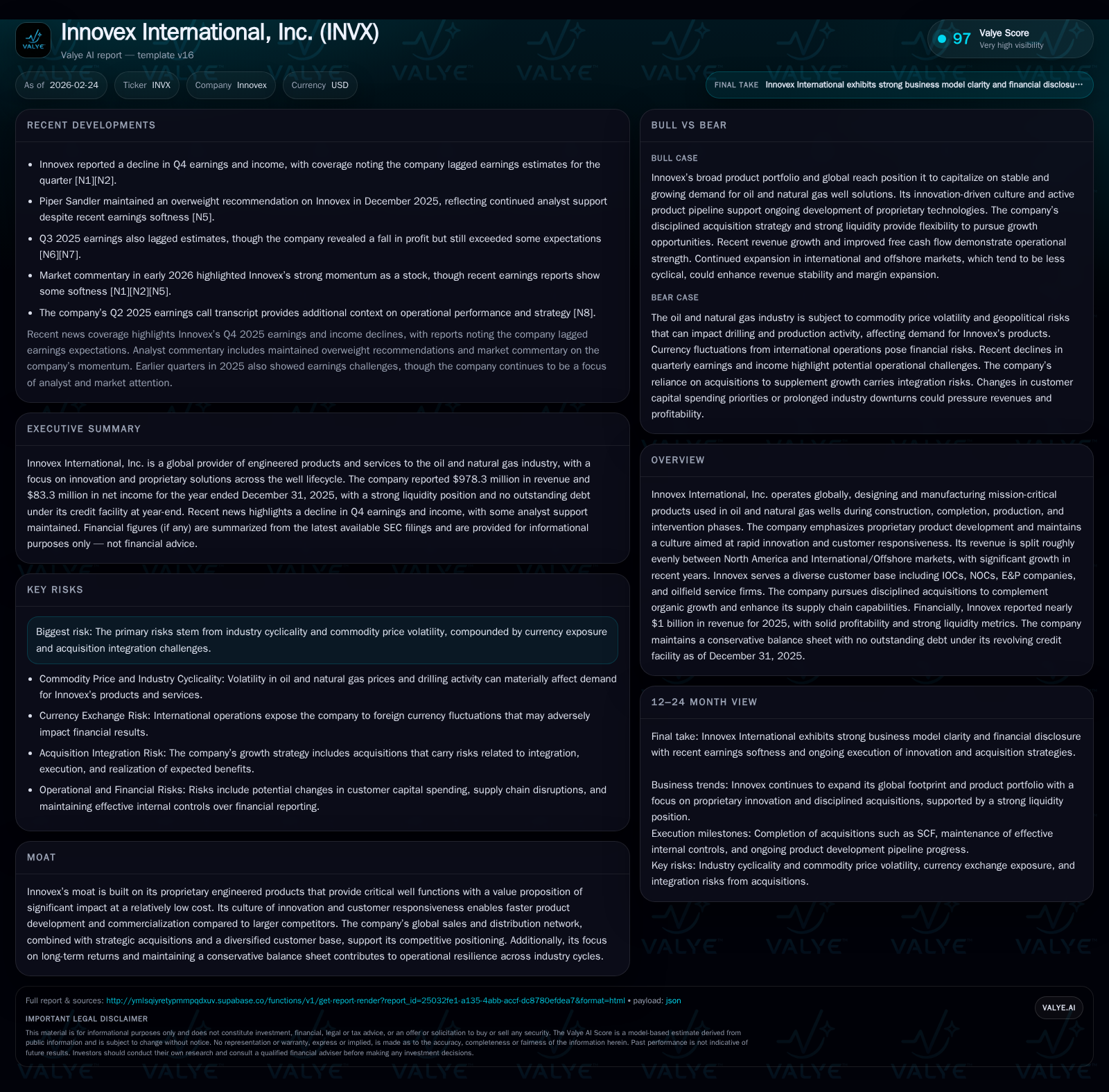

Innovex International’s Revenue Surge and Innovation Edge Fuel Competitive Global Growth

Innovex International leverages proprietary engineering and geographic diversification to drive robust revenue growth and operational resilience against sector cyclicality.

Innovex International, Inc. has demonstrated a pronounced revenue and earnings growth trajectory over the past five years, underpinned by its development of mission-critical downhole products serving both North American unconventional and international offshore markets. The company’s 'No Barriers' innovation culture accelerates proprietary product commercialization, giving it a durable competitive edge in well-centric technologies. Despite recent quarterly earnings softness linked to cyclical drilling expenditure fluctuations, Innovex maintains strong cash flow generation and a conservative capital structure with no outstanding term debt. Strategic acquisitions complement organic expansion, especially in international markets such as the Middle East. Looking forward, maintaining margin stability amid integration risks and navigating commodity price volatility remain key challenges as the company pursues growth beyond its core NAM footprint.

Steady Ascension: Historical Revenue and Profitability Growth Drivers

Innovex International’s financial history over the past five fiscal years is marked by an aggressive revenue ascent that more than tripled from approximately $323 million in FY2021 to close to $978 million by FY2025 [F1]. This impressive expansion reflects a combination of heightened global oilfield activity — especially in North American unconventional plays — alongside strategic acquisitions that expanded product breadth and geographic reach.

Operating income exhibited even more dramatic growth proportions: rising from a modest $2.5 million in FY2022 to $133 million in FY2025, representing a year-over-year increase exceeding 170% most recently [F1]. This leap illustrates Innovex's ability to scale profitability through operational leverage as it expands its proprietary engineered products platform within wells’ construction and production phases.

Net income shows greater variability; following a peak of $140 million in FY2024, it fell by about 40% to around $83 million in FY2025 [F1]. This decline partly arises from acquisition-related integration costs and cyclical market headwinds impacting short-term margins.

Operating cash flow followed a strong upward trajectory as well, doubling from roughly $93 million in FY2024 to nearly $191 million by end-2025 [F1], supporting ongoing Capital expenditures which surged close to 73% YoY to more than $35 million — indicative of investments aimed at capacity expansion and innovation funding.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 83 | 191 | 133 | -40.6% | ||

| 2024 | 140 | 93 | 49 | +23132.6% | ||

| 2023 | 424 | 1 | 8 | 5 | +17.1% | +36.3% |

| 2022 | 362 | 0 | -37 | 3 | +12.1% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 0 | ||

| 2024 | 75 | ||

| 2023 | 0 | -25 | |

| 2022 | 21 | -56 |

Source: SEC companyfacts cache [F1].

Note: CFO shown as net cash provided by operating activities; Capex is payments for property plant & equipment; Capex for FY24 incomplete due to mid-year filing timing.

These figures underscore the transformational phase for Innovex driven by both organic market penetration—particularly within North American horizontal drilling—and targeted acquisitions fueling new product rollouts and geographic market entries.

Mission-Critical Innovation as a Moat: Product Development and Commercialization Culture

At the heart of Innovex’s competitive advantage is its suite of proprietary engineered products designed specifically for well-centric applications such as drilling construction, completion stages, production optimization, and intervention tools employed downhole during well lifecycles [S1][S4]. This includes advanced consumables geared toward horizontal/unconventional wells prevalent across the US and Canadian basins.

The company frames its value proposition around "Big Impact, Small Ticket" products that deliver outsized operational improvements at relatively modest pricing — saving customers significant rig time and costs while enhancing well performance reliability.

Innovex’s R&D philosophy diverges from traditional segment incumbents through its "No Barriers" culture—a deliberate organizational effort removing internal obstacles that often slow innovation cycles within large legacy players [S4]. This culture empowers cross-functional teams toward rapid ideation, prototyping, and customer-engaged development collaborations that yield faster commercialization.

Such approaches resonate deeply given the critical nature of downhole consumables where reliability under extreme subsurface conditions (high pressures, corrosive fluids) directly impacts operational success.

The iterative feedback loops with anchor customers support tailored innovations aligned precisely with evolving industry challenges—ranging from friction reduction tools enhancing directional drilling efficiency to high-performance composite materials minimizing wear while reducing maintenance intervals.

Geographic Diversity: Balancing North America’s Unconventional Strength with International Expansion

Revenues are geographically balanced between approximately half derived from the North American Market (NAM)—dominated by U.S. land-based unconventional wells—and nearly half from International/Offshore regions encompassing longer-cycle investments offering reduced volatility exposure [F1][S4][S10].

Within NAM, Innovex maintains extensive sales-distribution networks reaching key shale basins across Texas, Oklahoma, Pennsylvania, Alberta, and British Columbia supporting widespread adoption of high-margin proprietary consumables applicable across the lifecycle of horizontal wells.

Internationally, Innovex targets regions like the Middle East (notably Saudi Arabia), Latin America (Brazil), Asia, Europe, and Gulf of Mexico offshore operations where upstream spending is characterized by multiyear project timelines less susceptible to short-term price fluctuations [S4][S17]. Saudi Arabia alone accounted for roughly $70 million in revenue in FY2025 — illustrating foothold gains outside traditional NAM geographies.

This dual-market strategy supports cyclical risk mitigation where shorter-term NAM demand slumps can be partially offset by steadier offshore capital projects with longer planning horizons.

Global manufacturing includes low-cost country sourcing initiatives such as Vietnam-based machining capacity acquired via SCF that enable cost-competitive production without compromising quality standards essential for downhole tooling reliability [S9][S10].

Earnings Volatility and Market Response: Recent Q4 Performance in Context

Recent news highlights Innovex’s Q4 earnings falling short of consensus estimates accompanied by a sequential decline in quarterly profits [N1][N2], attributed primarily to shifts in North American drilling spend patterns typical of upstream cyclicality [S3].

While headline shortfalls caused momentary stock pressure, annual full-year results retain robust upward momentum showcasing resilience amid industry oscillations.

Downturns correlate with fluctuating rig counts affecting demand for drill-through components (downhole consumables), often triggering temporary inventory adjustments or contract timing aberrations.

Investors should anticipate these periodic swings as natural within oilfield equipment cycles given their tight correlation with exploration budgets tied ultimately to oil price volatility—emphasizing importance of monitoring order book changes across NAM vs international segments closely as leading indicators.

Strategic Acquisitions Complement Organic Growth Trajectory

Complementing organic innovation efforts is a disciplined acquisition strategy targeting companies offering complementary technologies or expanding manufacturing/supply chain efficiencies [S1][S8].

Notable examples include Citadel acquisition ($69.7 million cash consideration) bringing differentiated downhole tech aimed at cycle time reduction via operational efficiencies globally; SCF acquisition bolstering exclusive manufacturing capacity in low-cost Vietnam materializing direct cost benefits alongside quality control improvements [S8][S10].

These transactions reinforce Innovex’s "build-and-buy" ethos wherein high-potential targets undergo careful due diligence against stringent investment criteria ensuring alignment with long-term returns objectives rather than reactive add-ons.

Integration risk exists but is mitigated through clear cultural fit analysis emphasizing sustained innovation cadence post-merger and deep customer relationships preserving established revenue streams whilst enabling cross-selling synergies.

Capital Structure and Allocation: Conservative Debt Approach with Cash Flow Advantage

Financially conservative policies underpin Innovex's sturdiness; notably, there was no outstanding term loan debt at December-end FY2025 following refinancing eliminating prior commitments under Second A&R Credit Agreement—replaced by an enlarged revolving credit line up to $200 million maturing February 2030 with potential increase flexibility up to $250 million subject to borrowing base calculations [S5][S6].

Cash balances were healthy at approximately $203 million accompanied by availability under revolving facility remaining strong at about $138 million providing ample liquidity headroom for working capital needs or opportunistic acquisitions.

Current ratio stood near an enviable ~4.9x highlighting robust short-term asset coverage against liabilities positioning the firm favorably relative to capital-intensive peer group norms where ratios closer to unity or below are common due to significant fixed asset loads [F1].

Capital expenditure increases denote ongoing investments into manufacturing capabilities supporting growth mandates while capital allocation eschewed dividends entirely during FY2025 — signaling prioritization of balance sheet deleveraging plus reinvestment opportunities over shareholder distributions currently [F1].

Return metrics estimate ROE at nearly 7.9%, somewhat restrained due partly to equity base expansions from recent mergers but reflective of disciplined employment of capital producing attractive operating margins (~14%) even amid cyclical softness indicating good cost absorption capacity within global operations context [F1][S20].

Looking Forward: Growth Opportunities Amid Commodity Volatility and Industry Cycles

Strategic ambitions focus on materially augmenting international/offshore revenue shares which tend to experience less pronounced cyclicality compared with NAM market tied closely to oil price-driven rig counts [N3][N4][S12][S26]. Expanding presence into markets like Middle East harnesses stable state-backed capex flows supporting deeper penetration of proprietary well-technologies addressing complex reservoir challenges common offshore or desert environments.

However, risks loom: currency volatility arising from diversified global operations could impact reported results despite natural hedging attempts; acquisition integration complexities also pose potential profit pressure until synergies fully realized.

While explicit financial guidance remains absent per SEC filings—and thus prospective investors should label growth outlooks as analysis—important performance metrics going forward include segmental revenue breakdown evolution outside NAM; margin trends particularly regarding newly integrated businesses; working capital management effectiveness; borrowing base utilization strategies within existing credit lines; any resumption plans for share repurchases or dividend initiations warrant scrutiny for indications on management confidence level regarding business sustainability amidst external uncertainties.

Investor Considerations: What to Watch Next in Financial Metrics and Market Moves

Given Innovex's positioning as a momentum stock cited by analysts emphasizing rapid upstream market recovery potential alongside inherent cyclicality awareness ([N3],[N6]), key data points worth monitoring include quarterly order intake reports segregated by geography—a proxy for drilling activity forecasts especially unconventional plays' health; margins on recently acquired product lines revealing integration progress; evolution of liquidity ratios informing risk appetite thresholds; and announcements relating to capital deployment whether accelerating buybacks or enlarging acquisition war chest signaling strategic priorities shift.

Continuous engagement with quarterly releases will provide timely insights into any accelerating headwinds or unexpectedly swift rebounds characteristic of upstream resource equipment providers whose fortunes often swing dramatically aligned historically with commodity pricing impulses blended into exploration output decisions.

Disclaimer: This report is based solely on publicly available data including SEC filings ([S#]), news sources ([N#]) and companyfacts snapshots ([F1]). It contains no investment advice or recommendations but aims solely to inform experienced market participants regarding Innovex International's financial condition, operational profile, strategic posture, and associated risks according to disclosed facts as of February 24, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments