KALA BIO’s Pivot to AI Platforms Highlights Post-Biotech Transition Challenges

Following clinical trial failure and cessation of biologic R&D, KALA BIO shifts focus to commercializing an on-premises AI platform for the biotech industry.

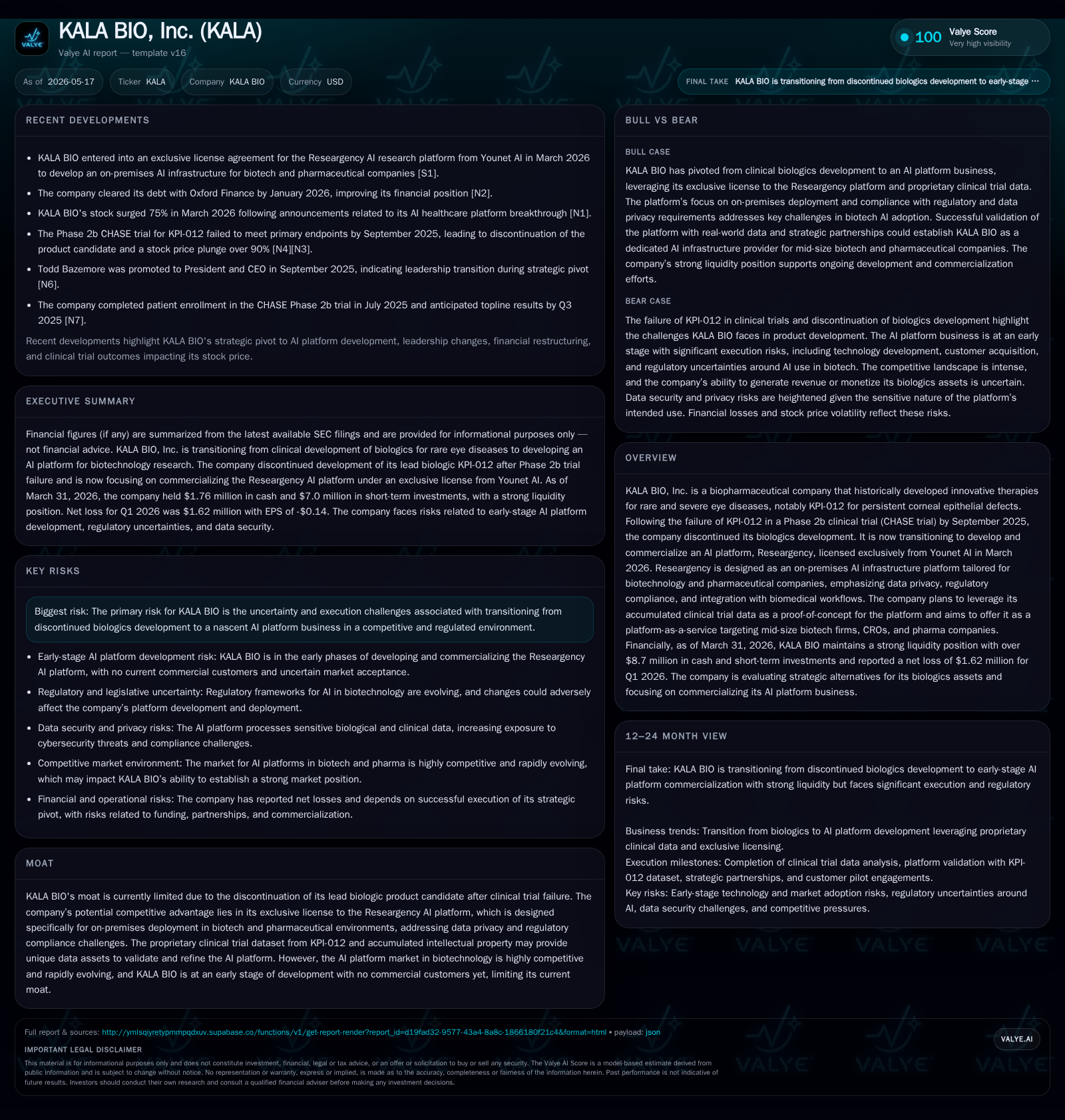

KALA BIO’s latest 10-Q filing outlines its ongoing transition from disrupted biologics development to an exclusive AI platform license targeting biotech and pharmaceutical companies. After discontinuing the KPI-012 biologic following a failed Phase 2b trial, the company secured worldwide rights to Researgency, an AI infrastructure platform emphasizing data privacy and integration with biomedical workflows. Commercial traction is nascent with no current revenues, and execution risks remain amid a competitive market. Financially, KALA faces capital constraints but retains runway to advance platform validation using proprietary clinical datasets.

Latest Quarterly Update and Strategic Shift

KALA BIO’s May 15, 2026 10-Q filing confirms its operational transformation following the failure of the CHASE Phase 2b trial for KPI-012. The trial did not meet primary or key secondary endpoints, prompting cessation of the MSC-S biologics platform development by late September 2025 [S1]. This led to a workforce reduction of approximately 51%, reflecting a substantial restructuring to align with curtailed clinical R&D activities [S1].

In March 2026, KALA entered an exclusive license agreement with Younet AI securing worldwide rights to Researgency—an agentic AI research platform tailored specifically for biotechnology applications [S6]. This represents a critical inflection as KALA shifts from traditional drug development toward commercializing an AI infrastructure service.

Leadership changes through late 2025 into early 2026 culminated in Avi Minkowitz assuming CEO and CFO roles by February 2026 [S1], [S27]. The operational focus has shifted toward building the Researgency business line while managing legacy IP monetization options.

Business Model Evolution: From Biologics to AI-as-a-Service

Previously focused on proprietary MSC-S biologics targeting rare ocular diseases via clinical development programs [S1], KALA’s suspension of clinical trials extinguished near-term biologics revenue prospects. The company now pivots toward software-driven recurring revenue through licensing Researgency under an exclusive agreement [S6].

Researgency aims to orchestrate biotechnology workflows including protocol design support, regulatory analytics, biological data interpretation, and IP management modules—all designed for secure on-premises deployment respecting client data privacy requirements [S7], [S9]. Revenue is expected from subscription licenses combined with implementation services and maintenance contracts targeting mid-tier biotech firms, CROs, and pharmaceutical companies requiring strict regulatory compliance and data sovereignty [S9]. While this represents a strategic shift away from capital-intensive drug development toward scalable software offerings, customer adoption remains unproven.

Product Offering and Differentiators

Researgency is positioned as a dedicated AI research infrastructure solution addressing unique biotech needs for secure, auditable on-premises deployment—a contrast to many cloud-centric competitors less focused on pharmaceutical regulatory constraints [S7]. Key capabilities include:

- Multi-agent orchestration supporting elements like patient stratification and site selection in clinical trials.

- Integration with laboratory information management systems (LIMS), regulatory repositories, and clinical datasets.

- Audit trails and validation aligned with FDA Good Clinical Practice standards.

- Deployment flexibility via private-cloud or fully on-premises models accommodating stringent data governance.

- Specialized modules such as Clinical Trial Intelligence agents leveraging validated historical trial data.

- Predictive analytics for regulatory pathway optimization based on FDA guidance analysis.

- Biological data pattern recognition powered by machine learning trained on internal KPI-012 datasets.

- Intellectual property management tools including patent landscape analytics and competitive intelligence monitoring.

This approach addresses common biotech challenges around confidentiality, complex regulations, and costly custom IT solutions [S7]. Utilizing accumulated internal clinical datasets provides a proof-of-concept environment enhancing credibility prior to broad commercialization [S9].

Industry Context and Competitive Landscape

The biotech AI infrastructure sector is fragmented with offerings ranging from cloud-based platforms by major tech firms to startups specializing in vertical solutions. Few competitors effectively address on-premises deployment or detailed pharmaceutical regulatory controls—areas where Researgency seeks differentiation.

Nonetheless, competition is intense with established enterprise AI vendors offering broader feature sets and deeper sales channels. Switching costs vary but entrenched bioinformatics ecosystems present adoption barriers requiring education efforts by KALA. Real-world pilot results will be critical given the novelty of agentic AI applied specifically in biotech research workflows.

KALA’s proprietary KPI-012 datasets may provide a unique content moat supporting advanced modeling capabilities not easily replicated by others [S21]; however, absence of paying customers places the firm at an early commercial stage compared to peers with established collaborations.

Growth Drivers and Commercial Pathway

Near-term growth catalysts revolve around validating Researgency using KALA’s comprehensive KPI-012 clinical datasets covering 79 patients across 37 sites along with regulatory submission materials [S21], [S9]. This internal "beta" phase aims to generate reference case studies demonstrating utility while refining product-market fit before external client engagements.

Scaling depends on securing pilot agreements with mid-size biotech companies or CROs willing to adopt specialized on-premises AI solutions—addressing a niche market sensitive to data control concerns and workflow integration complexities.

Revenue generation will hinge on finalizing subscription pricing models plus professional services fees, successful onboarding of initial clients, execution of service-level agreements, and establishing stable maintenance programs—all currently in formative stages per filings [S9]. Monitoring KPIs such as pilot conversions, contract signings, renewals, and feature uptake will be essential metrics going forward.

Risks and Operational Challenges

Transitioning from biologics R&D to SaaS presents risks including technical execution hurdles in developing robust multi-agent orchestration systems alongside market acceptance challenges within a conservative industry accustomed to traditional informatics, [S1].

Financial constraints compound these risks; persistent operating losses limit the capacity for sustained commercial ramp without additional funding. The company’s going concern status has been noted by auditors reflecting liquidity pressures [S20]. Regulatory uncertainties persist given evolving FDA digital health guidelines complicating compliance efforts.

Legacy obligations remain significant: total debt stood near $26.95 million as of September 2025 versus cash reserves of approximately $1.76 million at March quarter-end—indicating tight capital buffers during this repositioning phase without current operating revenues [F1], [S2]. Managing stakeholder expectations amid uncertain legacy IP monetization adds further complexity.

Upcoming Catalysts and Key Metrics to Monitor

Key near-term milestones include:

- Progress reports on pilot deployments using proprietary KPI-012 datasets validating algorithmic performance in real-world workflows.

- Announcements of commercial client signings or expansions signaling initial market acceptance.

- Publication or refinement of pricing/licensing frameworks aligned with customer feedback.

- Updates regarding potential sales or licensing transactions involving MSC-S biologics IP assets offering possible cash inflows.

- Strategic hires or partnerships enhancing go-to-market capabilities.

- Quarterly cash burn trends coupled with any funding announcements indicating runway extension or refinancing activity.

Close monitoring of these indicators will illuminate whether KALA successfully advances its repositioned business model towards sustainable growth or continues facing execution headwinds anchored by structural funding challenges.

Financial Overview and Liquidity Position

As of March 31, 2026, KALA BIO held cash & equivalents approximating $1.76 million against current liabilities near $1.56 million resulting in a strong current ratio of approximately 7.91 supported by current assets totaling about $12.3 million which includes non-cash components [F1]

However, total debt outstanding was reported around $26.95 million as of September 30, 2025 implying net debt close to $25.18 million after accounting for cash balances—a substantial leverage load relative to available liquidity during this transition phase absent operating revenues [F1]

Operating losses continue reflecting legacy R&D expenditures; prudent balance sheet management alongside achieving meaningful commercial traction will be vital pending successful monetization efforts. Limited financial cushion underscores urgency in securing additional capital or accelerating revenue generation consistent with strategic pivots outlined [F1]

This analysis synthesizes disclosed SEC filings through May 15th, 2026 combined with sector-contextualized industry insights without speculation beyond documented facts. It highlights pivotal operational shifts in KALA BIO's evolution from discontinued biologic therapeutics toward prospective biotech-focused AI infrastructure solutions amid inherent commercialization risks typical of transformative corporate transitions.

Financial position in context

As of 2026-03-31, companyfacts shows $1764000 in cash and equivalents [F1]. Current assets of $12mm and current liabilities of $1557000 imply a current ratio near 7.91x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments