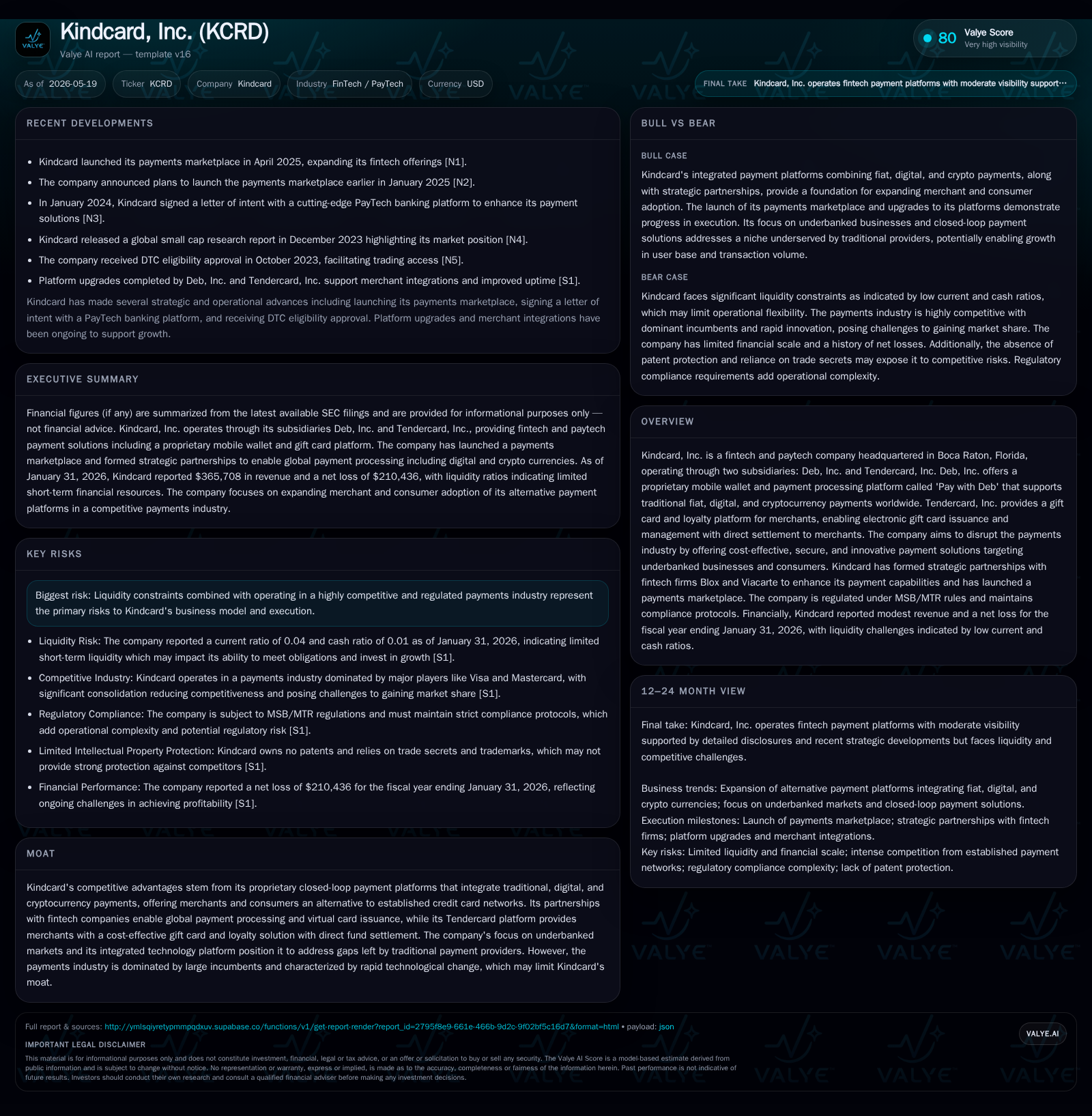

Kindcard Powers Payment Innovation with Integrated Wallet and Loyalty Platforms

Kindcard’s latest quarter reveals advancing technology integration and merchant acquisition momentum as it pursues disruption of global payments through its Deb and Tendercard platforms.

In its most recent quarterly filing, Kindcard has made meaningful upgrades to its Deb and Tendercard subsidiaries’ platforms and identified merchants ready for integration, signaling tangible progress in commercial traction. Deb’s all-encompassing payment wallet supports fiat, digital, and cryptocurrency transactions via strategic partnerships, while Tendercard expands its simple, cost-effective gift card and loyalty platform targeting merchants directly. This dual-platform approach addresses underserved underbanked markets by offering closed-loop alternatives to legacy credit card networks. Despite competitive intensity and regulatory complexities in payments, Kindcard’s innovation focus and partnership ecosystem position it to gradually scale merchant adoption. Liquidity constraints remain a significant risk amid continued investment in platform development and growth execution.

Latest Quarterly Update Highlights

Kindcard’s most recent quarter ending January 31, 2026 revealed concrete operational strides anchored on critical infrastructure improvements per its 10-Q filing dated December 22, 2025 [S2]. Notably, Tendercard completed server upgrades securing a 99.9% uptime commitment for its merchant subscribers—a foundational enhancement for reliability in payment processing. Concurrently, Kindcard identified specific merchants poised for integration with Deb’s "Pay with Deb" wallet solution as an alternative payment method accepting traditional fiat currency alongside digital assets.

These developments reflect incremental but vital progress in customer acquisition and platform stability. Tendercard’s uptime guarantees signal a maturing backend capable of supporting scalable merchant onboarding, essential given the upcoming push toward the lucrative holiday sales period in late 2026. For Deb, selectively vetting merchant partners likely improves transaction volumes once live while mitigating onboarding friction critical in fintech adoption cycles.

Business Model and Product Offering

Kindcard operates through two wholly owned subsidiaries—Deb, Inc. and Tendercard, Inc.—which generate revenue by providing distinct yet complementary fintech services integrating into the payments value chain [S1]. Deb represents a broad-spectrum mobile wallet and payment processor enabling consumers and businesses globally to transact using traditional fiat currency as well as digital currencies including cryptocurrency.

Deb's revenue arises primarily from payment processing fees charged to merchants who accept "Pay with Deb" as an alternative to conventional credit or debit cards [S7][S9]. By offering a closed-loop wallet system partnered with Blox (for wallet accounts allowing asset storage and conversion) and Viacarte (providing Virtual & Signature Black Visa cards usable wherever Visa is accepted), Deb enhances user versatility while retaining funds within a proprietary payment ecosystem that lowers interchange costs typically imposed by legacy card networks

Tendercard taps into the electronic gift card and loyalty solutions niche—a less saturated segment within paytech—providing independent merchants with a turnkey closed-loop gift card program that replaces manual paper certificates with digitally managed cards linked directly to merchant accounts. Revenue is derived from flat monthly subscription fees granting unlimited gift card issuance and acceptance plus access to proprietary back-office systems for marketing and reporting [S7][S9]. This design eliminates intermediaries holding onto merchant funds post-sale—a significant differentiator enhancing cash flow visibility for small businesses

Combined, these platforms address both consumer payment convenience via Deb’s multi-currency wallets and merchant-centric loyalty retention tools via Tendercard’s offerings.

Competitive Environment and Industry Dynamics

The payments industry continues to be dominated by incumbents—Visa, Mastercard, Discover, American Express—who control interchange fees and network processing rules. These giants benefit from entrenched adoption at the point-of-sale across both online and offline channels creating substantial switching costs for merchants who might otherwise seek alternatives. Moreover, ubiquitous fintech rivals such as PayPal, Apple Pay, Google Pay have accelerated digital payments innovation but remain anchored in legacy card rails or open-loop models [S9][S11].

Kindcard's competitive positioning stems from its focus on closed-loop payment ecosystems which sidestep some traditional interchange costs by routing transactions within proprietary wallets or merchant networks. This provides pricing leverage prospects absent in open-loop models where transaction fees are largely fixed by network operators. Furthermore, targeting underbanked businesses—a cohort often neglected or overcharged by traditional banks—allows Kindcard to capture market share through higher service customization tailored to smaller merchant pain points such as cost transparency and direct fund settlement.

However, despite these differentiators the company contends with intensive technological change requiring continual R&D investment alongside navigating complex regulatory environments governing money transmission (MSB/MTR compliance). The landscape features fragmented competition including niche players building vertical-specific payment solutions that could erode potential market share if Kindcard's pace of innovation falters.

Strategic Growth Drivers

Several explicit growth catalysts define Kindcard’s near-to-medium term outlook. First is the strategic ramp-up of merchant onboarding particularly timed around the anticipated surges in consumer spending during the late 2026 holiday season facilitated largely through Tendercard’s gift card platform expansion efforts [S8][S9]. Adding merchants directly enhances transactional volume inflows supporting topline growth.

Simultaneously, Deb leverages its technology partnerships with Blox—a fintech specializing in custody and seamless digital asset handling—and Viacarte—which enables issuance of virtual Visa cards—for broadening global reach across B2B, B2C, C2B segments including peer-to-peer payments [S7][S9]. This integration expands use cases beyond simple wallet transactions adding versatility that appeals to sophisticated users seeking crypto-to-fiat conversion capabilities embedded within one platform.

Moreover, structural trends toward greater cryptocurrency adoption—especially among younger demographics—and growing disenchantment among SMEs over high fees charged by conventional processors underpin size-of-the-opportunity expansion drivers. The company views the rise of web3/blockchain as aligned tailwinds that complement its closed-loop innovation strategy rather than existential threats.

Key Risks and Operating Constraints

Liquidity presents an acute risk vector for Kindcard with its latest balance sheet revealing a stark current ratio of approximately 0.04 due to current liabilities exceeding current assets by a tenfold margin (Current assets: ~$41.7K vs current liabilities: ~$1M) as of January 31, 2026 [F1]. Cash balances stand modest at about $13K while total debt data from earlier periods implies leverage tightness given ongoing operating losses near $250K last reported period. These conditions underscore funding sustainability challenges amid further required investment in product development and sales scaling.

Regulatory complexity also weighs heavily on operations; Deb must comply stringently with Money Services Business (MSB) / Money Transmitter Regulations (MTR) involving comprehensive anti-money laundering protocols vetted by external advisors. Failure to maintain compliance risks onerous penalties or license withdraws which would severely constrain operational viability [S10].

The competitive environment adds pressure for continuous innovation with historically limited research & development expenditures potentially limiting pace relative to better-capitalized peers deploying cutting-edge AI fraud detection or open banking integrations.

Dependency on third-party partners Blox and Viacarte also introduces concentration risk; disruption or deterioration of these relationships could materially impact service deliverability or product capability breadth necessary for market relevance.

Upcoming Catalysts and Monitoring Points

Key near-term indicators include tracking momentum around new merchant activations integrated on both the Tendercard gift card network ahead of holiday buying peaks as well as measuring increases in active wallet users transacting via Deb’s multi-currency platform [S2][S8]. Marketing campaign effectiveness aimed at resellers who bundle Kindcard offerings into their solutions suites will further indicate scaling success.

Operational KPIs such as system uptime adherence post-upgrades at Tendercard combined with transaction volume trends will reveal execution quality critical to retention given notoriously low switching costs in payments sectors.

Finally, potential regulatory shifts affecting MSB rules or Visa licensing conditions impacting virtual card issuance warrant close attention given their direct bearing on business continuity prospects.

Concise Financial Overview

As of the latest fiscal quarter ended January 31, 2026 per company facts data [F1], Kindcard reported revenue around $365K indicative of nascent commercial scale while operating losses persisted at approximately $251K reflecting ongoing investments in platform enhancements and go-to-market initiatives. Net loss stood near $210K underscoring current unprofitability typical for emerging fintech ventures.

The balance sheet reveals constrained liquidity highlighted by total current liabilities surpassing $1 million against modest current assets ($42K), yielding a critically low current ratio (0.04) [F1]

This financial backdrop frames Kindcard as an early-stage operator prioritizing strategic technology differentiation and market entry over short-term profitability while navigating competitive headwinds and regulatory demands.

This analysis is based exclusively on publicly filed SEC documents as cited plus Kindcard-specific financial snapshots without conjecture or forward-looking statements beyond documented facts.

Financial position in context

Current assets of $41686 and current liabilities of $1010854 imply a current ratio near 0.04x for 2026-01-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments