Kiniksa Pharmaceuticals’ Turnaround Fuels Growth and Profitability in Immunology

Kiniksa reversed prior operating losses to achieve profitability in 2025 through strong product sales and strategic partnerships.

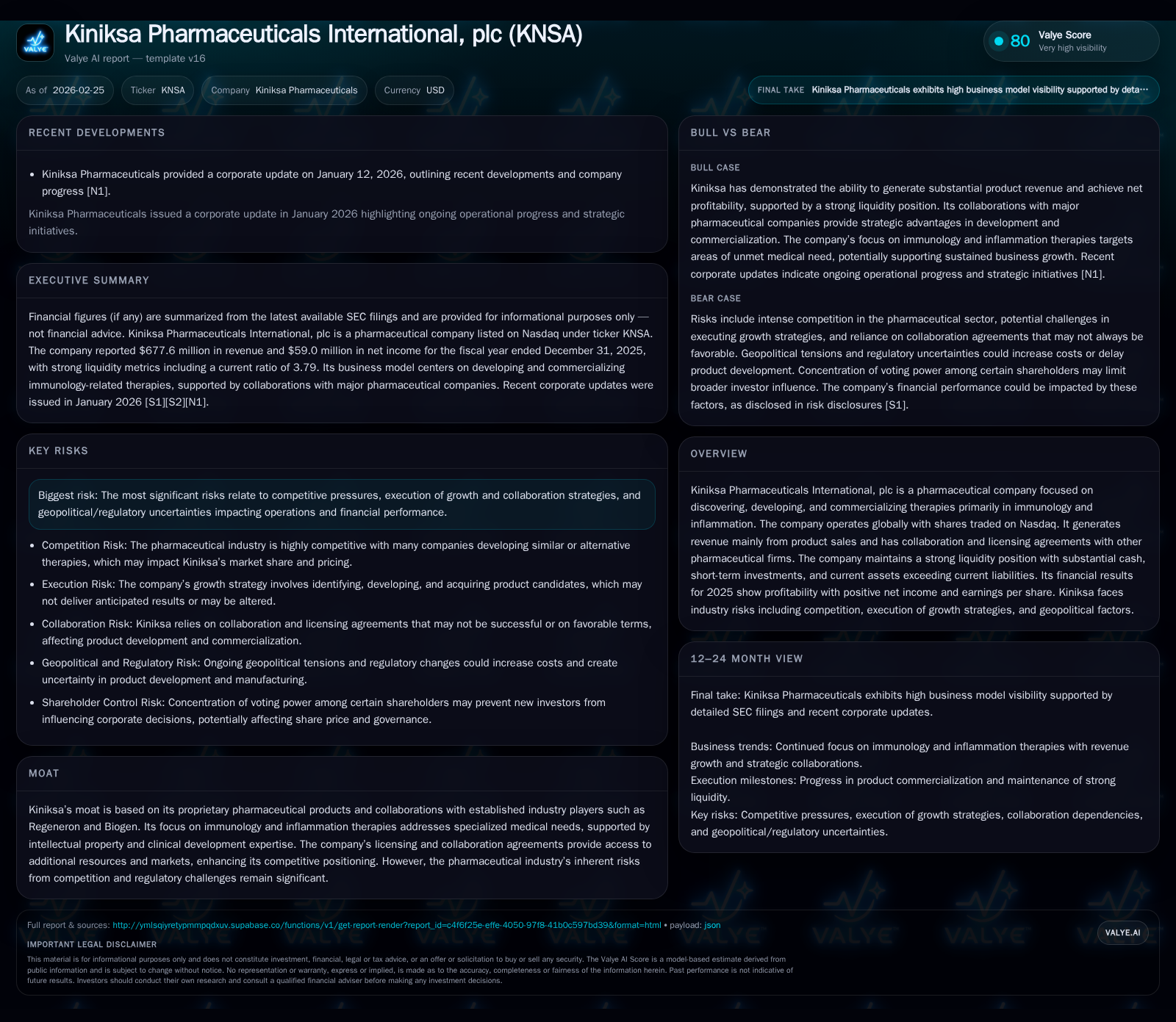

Kiniksa Pharmaceuticals International has transformed its financial trajectory by leveraging its immunology and inflammation product portfolio alongside key collaborations with Regeneron and Biogen. In 2025, the company reported over 60% revenue growth year-over-year and swung from operating losses to $77 million in operating income. Robust cash flow generation underpins capital efficiency, although execution risks and geopolitical factors remain noteworthy challenges. Future growth hinges on continued product commercialization and pipeline advances, supported by a strong liquidity position.

A Financial Rebound: Kiniksa’s Journey from Loss to Net Income

Kiniksa Pharmaceuticals International’s financial performance in recent years illustrates a compelling turnaround. After several years of operating challenges—including sustained operating losses in both 2023 ($-25M) and a more significant downturn in 2024 ($-46M)—the company reported a sharp reversal in 2025. Revenues soared to approximately $678 million, up over 60% from $423 million in the prior year [F1]. This top-line momentum cascaded into profitability with operating income climbing to $77 million in 2025, contrasted against negative figures the previous two years.

Net income swung dramatically from a loss of $43 million in 2024 to a positive $59 million in 2025 [F1]. This earnings inflection underscores improved operational leverage and cost management alongside enhanced revenue quality. Margin improvement was evident as cost structures aligned better with expanding sales volumes.

This transformation signals Kiniksa's ability to execute commercial strategies effectively within its specialized immunology segment, marking a durable shift towards sustainable profit generation [N1][N2].

Revenue Drivers: Product Growth and Collaborative Revenues in Immunology

Kiniksa’s revenue surge is largely attributable to the successful commercialization of its specialized therapies targeting immunological and inflammatory diseases. The company benefits significantly from licensing arrangements and collaboration agreements with major pharma players such as Regeneron and Biogen [S10][N1].

These collaborations provide recurring licensing fees, milestone payments, and shared royalties — crucial for mitigating R&D investment risks inherent to drug development cycles. At the same time, product sales have gained traction driven by market adoption of Kiniksa’s proprietary assets addressing orphan indications with limited competitive alternatives.

Combined, product commercialization and collaborative revenues undergird the company’s high-growth profile within targeted niches of immunology [S10]. This dual revenue stream structure helps stabilize cash inflows even amid clinical development uncertainties.

Strategic Partnerships Enhancing Competitive Moat and Innovation Pipeline

A central element of Kiniksa’s moat derives from its strategic alliances. Collaborations leverage external capabilities for clinical trials, regulatory pathways, manufacturing scale-up, and commercialization channels [S1].

By partnering with Regeneron on vixarelimab licensing or Biogen on inherited rare diseases assets, Kiniksa shares development costs while accessing expanded geographic markets [S1][N8]. Such partnerships also facilitate cross-licensing rights that support pipeline diversification.

The resultant risk-sharing model reduces standalone R&D expenditure volatility while accelerating clinical advancement—an approach critical in immunology where trial complexities and patient recruitment pose challenges. Thus, these alliances constitute both financial shields and innovation accelerants for pipeline maturation.

Capital Efficiency: Robust Cash Flows and Prudent Investment Patterns

Operating cash flow (CFO) reflected Kiniksa’s renewed operational strength with a substantial increase to nearly $138 million in fiscal 2025 from roughly $26 million the prior year—a greater than fivefold rise [F1]. More importantly, this cash influx comfortably exceeds capital expenditures which remained modest at approximately $1.6 million despite a notable sequential rise from prior years.

The resulting free cash flow approximates $136 million—demonstrating exceptional internal funding capability without dependence on external equity or debt issuance [F1][S8][S24]. The company's liquidity posture is reinforced by current assets well over current liabilities (current ratio ~3.79), further supporting agility for organic initiatives or opportunistic acquisitions.

Notably, Kiniksa has not paid dividends nor engaged significantly in share repurchases yet, preserving capital for reinvestment into pipeline progression or commercial expansion [F1][S24]. This careful balance reflects prudent stewardship aimed at long-term value creation amid growth phases.

Risks in Execution and Market Dynamics: What Could Impact Forward Growth?

Despite promising progress, Kiniksa faces multifaceted risks common to specialty biopharma firms [S4][S7][S14][N1]. Competition remains intense especially within orphan drug segments where other companies may launch superior or cheaper alternatives.

Execution risks loom around maintaining collaborative relationships—with potential disagreements or shifting terms adversely impacting pipeline delivery or revenue flows. Regulatory landscapes also evolve unpredictably; delays or denials of approvals could materially affect commercialization timelines.

Geopolitical tensions pose further uncertainty regarding cross-border supply chains, pricing policies, tariffs affecting manufacturing costs, or market access limitations [S7]. Additionally, concentrated insider ownership influences corporate governance dynamics that could limit outsider shareholder influence.

Therefore, ongoing vigilance toward partnership efficacy, regulatory compliance, reimbursement climates, and geopolitical developments is essential for sustaining growth trajectories.

Key Milestones Ahead: Pipeline Progress and Market Expansion Prospects

Though explicit forward guidance remains sparse [N8], investors should monitor upcoming clinical trial readouts expected across Kiniksa’s immunology portfolio over the next 12-24 months. Achieving pivotal study success would unlock regulatory submissions enhancing commercial footprint.

Geographic expansion efforts—particularly leveraging global licensing partners—could broaden patient access beyond core U.S./U.K. markets documented previously [S10][N8]. Given industry-standard drug development timelines, anticipated milestones revolve around late-stage clinical phases advancing toward approval decisions.

Absent detailed forecast statements at this juncture, prospective catalysts predominantly hinge on managed pipeline advancements coupled with successful scaling of existing therapy sales.

Valuation Considerations: Return on Equity, Liquidity, and Capital Allocation

Kiniksa exhibits an improving return on equity estimated near 10.4% in FY2025—a significant rebound from prior years characterized by negative returns [F1]. This reflects effective deployment of shareholders’ capital toward profitable operations after overcoming earlier losses.

The company maintains a sizable equity base (approximately $568 million) alongside robust cash reserves supporting ongoing investment requirements without immediate dilution concerns [F1][S24]. While no dividends or share repurchase programs exist currently—typical for growth-stage pharmaceutical entities—the strong balance sheet endows flexibility for future capital return policy evolution as earnings stabilize.

Prudent capital allocation manifests via modest CAPEX relative to strong CFO growth; this controlled reinvestment preserves operational momentum while safeguarding liquidity buffers necessary amid sector cyclicality.

Summary Table: Kiniksa Pharmaceuticals - Key Financials (FY2022-FY2025)

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 678 | 59 | 138 | 77 | +60.1% | +236.6% |

| 2024 | 423 | -43 | 26 | -46 | -406.7% | |

| 2023 | 14 | 13 | -25 | -92.3% | ||

| 2022 | 183 | 6 | 10 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 136 | 10.4 |

| 2024 | 25 | -9.9 |

| 2023 | 13 | 3.2 |

| 2022 | 6 | 46.3 |

Source: SEC companyfacts cache [F1]. Note: Revenue is rounded to nearest million USD; percentage growth computed where data permits; Capex figures are approximate; Buybacks/dividends data not available.

Disclaimer: This analysis synthesizes reported financial data and disclosures without providing investment guidance or recommendations. All figures are cited from official SEC filings [F1], earnings calls [N1], and company releases up to February 25, 2026. Forward-looking statements are interpreted cautiously per available evidence without speculative forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments