Koppers Holdings Inc.: Industrial Integration and Growth Dynamics in Niche Markets

Koppers leverages vertical integration and dominant niche positions to sustain profit growth amidst volume declines and tariff challenges.

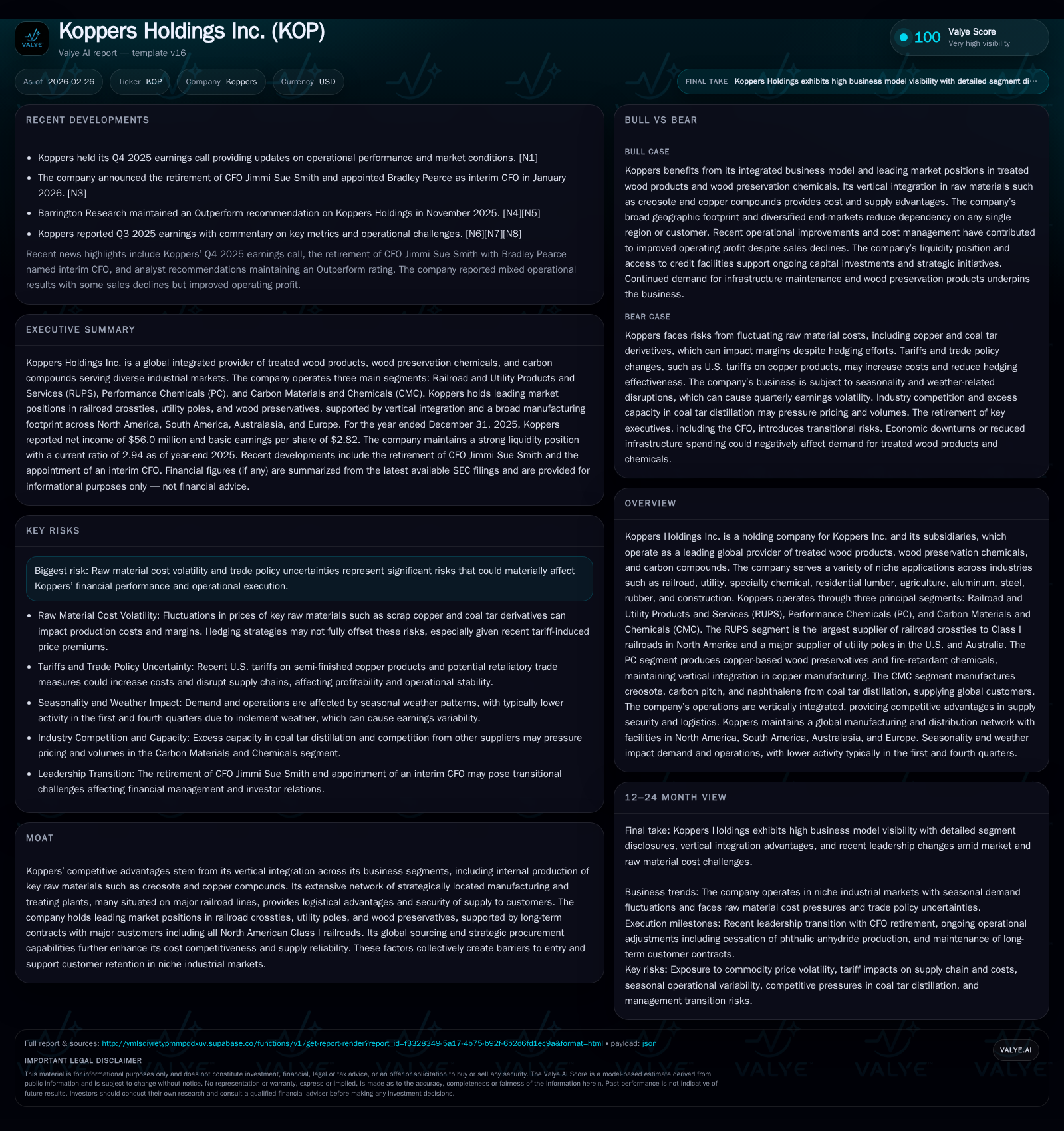

Koppers Holdings Inc. operates as a vertically integrated leader in treated wood products, wood preservation chemicals, and carbon compounds, primarily serving the railroad and utility sectors. Despite a 10.2% revenue contraction in 2025 driven by volume pressures and segment-specific headwinds, operating income surged 13.2% year-over-year, reflecting effective pricing strategies and cost control. The company’s vertical integration—particularly in creosote and copper processing—provides resilience against raw material volatility, while tariff-related risks persist but are actively managed through sourcing and pricing adjustments. Capital allocation balances acquisitions, share repurchases, dividends, and measured capex, supported by robust cash flow generation with a ~9.8% return on equity.

Strong Market Positions Driving Historical Revenue and Earnings

Koppers Holdings Inc., through its wholly owned subsidiary Koppers Inc., has established itself as a leader in specialized industrial wood products, wood preservation chemicals, and carbon compounds globally [S20]. The company’s three principal segments — Railroad and Utility Products and Services (RUPS), Performance Chemicals (PC), and Carbon Materials and Chemicals (CMC) — command leading shares in their respective niches.

Financially, 2025 saw consolidated revenues at approximately $1.879 billion, down 10.2% from $2.092 billion in 2024 [S1]. This decline traces primarily to volume declines within the PC (-16.5%) and CMC (-17.9%) segments, partially offset by resilience in RUPS which experienced only a minor dip (-1.7%) due to volume softness in Class I crossties balanced by higher domestic utility pole volumes and price increases of about $11 million across key markets [S1].

Yet profitability showed strength: Operating income rose by 13.2% year-over-year to $167.8 million—the improvement largely driven by cost discipline efforts and price adjustments rather than volume growth [F1][S1]. Net income rose more modestly to $56 million (+6.9%), underscoring some margin compression amid ongoing restructuring charges.

Cash flow from operations remained robust at $122.5 million (+2.6%), supporting capital spending of $55 million (-28.9%) which reflects completion of prior growth projects like the Nyborg CMC facility yield enhancement [F1][S1][S23].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 56 | 123 | 168 | 55 | +6.9% |

| 2024 | 52 | 119 | 148 | 77 | -41.3% |

| 2023 | 89 | 146 | 195 | 121 | +40.7% |

| 2022 | 63 | 102 | 138 | 105 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 38 | 68 |

| 2024 | 6 | 51 | 42 |

| 2023 | 5 | 20 | 26 |

| 2022 | 4 | 24 | -3 |

Source: SEC companyfacts cache [F1].

*Historical data beyond two years omitted for brevity; see [F1]

The above captures Koppers’ trajectory through measured pricing improvements amid tougher volumes particularly in specialty chemicals.

Volume Pressures and Product Mix Shifts Impacting Recent Performance

Volume erosion marked Koppers’ recent top-line pressures: PC segment's sales dropped predominantly due to a loss of U.S. market share (-17%) linked to competitive dynamics affecting key customers [S1][N1]. The cessation of phthalic anhydride production during Q2 2025 materially impacted CMC volumes ($67.5 million lower sales), compounded by global price softness for carbon pitch products (-6%), especially pronounced in Australasia [S1].

The divestiture of the railroad bridge services segment mid-2025 also reduced RUPS volumes but was partly compensated by increased domestic utility pole activity [S1]. Price increases notably helped offset volume declines—especially price hikes averaging about $11 million on crossties—and foreign currency movements had mixed impacts across segments [S1].

Segment-specific shifts underscore changing customer demand patterns within North American railroad maintenance-of-way activities that influence tie replacement volumes seasonally .

Vertical Integration as a Moat Against Raw Material Volatility

Koppers' competitive moat is anchored strongly in vertical integration—a strategic advantage uncommon among peers—providing cost control and supply chain stability for critical inputs.

In North America and Europe, the CMC segment processes coal tar into creosote internally consumed primarily by the RUPS treating operations for pressure treatment of wood crossties, poles, pilings, etc., securing internal supply against wholesale market swings [S22]. Creosote being central chemical for penetration into hardwood ties exemplifies this proprietary feedstock integration.

Similarly, PC produces copper-based preservatives such as chromated copper arsenate (CCA), dichloro-octyl-isothiazolinone (DCOI), micronized copper azole variants which are essential for utility pole treatment — these copper compounds are manufactured from scrap copper sourced globally but further processed internally at plants in Hubbell, Michigan & Millington, Tennessee [S13][S22]. Such vertical control nejen enables pricing power but also reduces exposure to commodity copper price spikes aided by hedging via swap contracts targeting copper scrap exposure [S2][S13].

This dual integration into creosote refining upstream of wood treating operations alongside vertically integrated copper manufacturing provides security of supply unmatched by many competitors who must source these inputs externally.

Tariff Risks and Supply Chain Mitigation Strategies

Trade policy uncertainties pose significant operational risks given that Koppers imports roughly $100–120 million annually of raw materials principally supplying PC and CMC segments into the U.S., though most imports originate outside China reducing direct tariff exposure somewhat [S2].

Recent U.S.-driven tariff escalations could cut pre-tax profits by an estimated $10–14 million over the next twelve months if left unmitigated [S2]. Koppers tackles this risk proactively via three tactical layers:

- Diversifying import origins away from high-tariff sources,

- Sharing cost burdens with suppliers where feasible,

- Incorporating contractually allowed price escalators with customers mostly restricted to select segments .

These mitigation strategies are industry-honed mechanisms addressing ‘tariff-induced cost push inflation’ risks typical for global chemical intermediates supply chains involved here.

While still potentially disruptive to margins if tariffs intensify or broaden unpredictably, these responses buffer immediate profit shocks.

Capital Allocation Focus: Balancing Acquisitions, Buybacks, Dividends, and Capex

Koppers demonstrates disciplined capital stewardship amid growth capital needs balanced against shareholder returns:

- Acquisitions: Brown Wood acquisition closed prior year bolstered portfolio; Greenhill acquired in current period supporting strategic expansion albeit with no disclosed synergy forecasts [S1][S3].

- Share Repurchases: In FY2025 repurchases totaled $38.2 million after heftier buys ($50.8 million) prior year—reflecting active buyback programs despite revenue pressures [F1][S1].

- Dividends: Dividend payouts were a modest ~$6.4 million showing stable distribution policy supporting income-focused investors yet conservative relative payout ratio given free cash flow generation [F1].

- Capital Expenditures: Capex moderated sharply from earlier peaks associated with major growth projects—from nearly $77 million in ‘24 down to around $55 million projected for ’26—reflecting project completions like Nyborg yield projects while earmarking capacity sustainment investment funded internally [F1][S1][S17].

Financially the company maintains leverage within covenant thresholds: total net leverage ratio came down to approximately 3.3x EBITDA at FY end versus maximum allowance of 4.75x under credit agreement terms; interest coverage ratios remain comfortable near 4.4x highlighting solid debt service capacity [S4][S6][S9].

This balance allows ongoing liquidity (~$383 million combined cash/credit lines) securing operational flexibility along with potential for further strategic acquisitions or capital returns backed by operations generating ~$67.5 million free cash flow as CFO minus capex suggests [F1][S5]. Return on equity approximates a healthy ~9.8%, consistent with steady profitability supporting reinvestment plus shareholder distributions [F1].

Future Outlook: Cost Management, Contract Pricing, and Industry Trends

Management commentary underscores continued emphasis on extracting efficiencies post-workforce rationalization measures implemented during early fiscal periods aiming at margin preservation despite weaker unit volumes notably within PC & CMC sectors [N2][S1]. Adjusted EBITDA reflects temporary impacts from restructuring costs however ongoing cost targets aim to stabilize earnings quality post-adjustments [S23].

Contract negotiations with North American Class I railroads remain pivotal; these long-term arrangements underpin a predictable demand base even if incremental volume growth appears constrained due to maintenance-of-way replacement cycles inherent to infrastructure asset management dynamics [N2]. Tariffs related to roofing components pose downside risks contingent on evolving trade policies.

Industry tailwinds are mixed: While infrastructure spending sustains demand for rail ties and poles bolstered by regulatory environment emphasizing safety compliance; specialty chemical markets face renewed competition requiring further product rationalizations observed through phthalic anhydride discontinuation [analysis combined with S1/N3/N2 info].

What to Watch: Key Milestones and Industry Signals for 2026 and Beyond

Key monitoring points that could shape Koppers’ prospects include:

- Quarterly earnings cadence revealing progress on tariff mitigation impact uptake,

- Raw material price trajectories especially scrap copper volatility along with creosote feedstock availability,

- Execution of planned capital expenditures aligned with yield enhancement or efficiency projects,

- Legal/regulatory developments particularly pending environmental litigation outcomes which could influence operational contingencies [$3.9M accrued remediation remains uncertain] [S11],

- Signals from contract renewals or shifts within large railroad customers possibly signaling altered maintenance capex patterns,

- Trade policy updates that may alter tariff regimes further impacting cost structures or customer pricing agreements.

These factors collectively will inform how well Koppers can preserve its competitive advantages balancing industrial integration while navigating operational headwinds.

Disclaimer: This report reflects analysis based solely on publicly available information without provision of investment advice or recommendations regarding securities buying or selling decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments