KonaTel’s Regulatory Moat and Market Challenges Shape 2026 Outlook

Recent restructuring around IM Telecom’s standalone operations highlights both regulatory reliance and operational adjustments limiting growth.

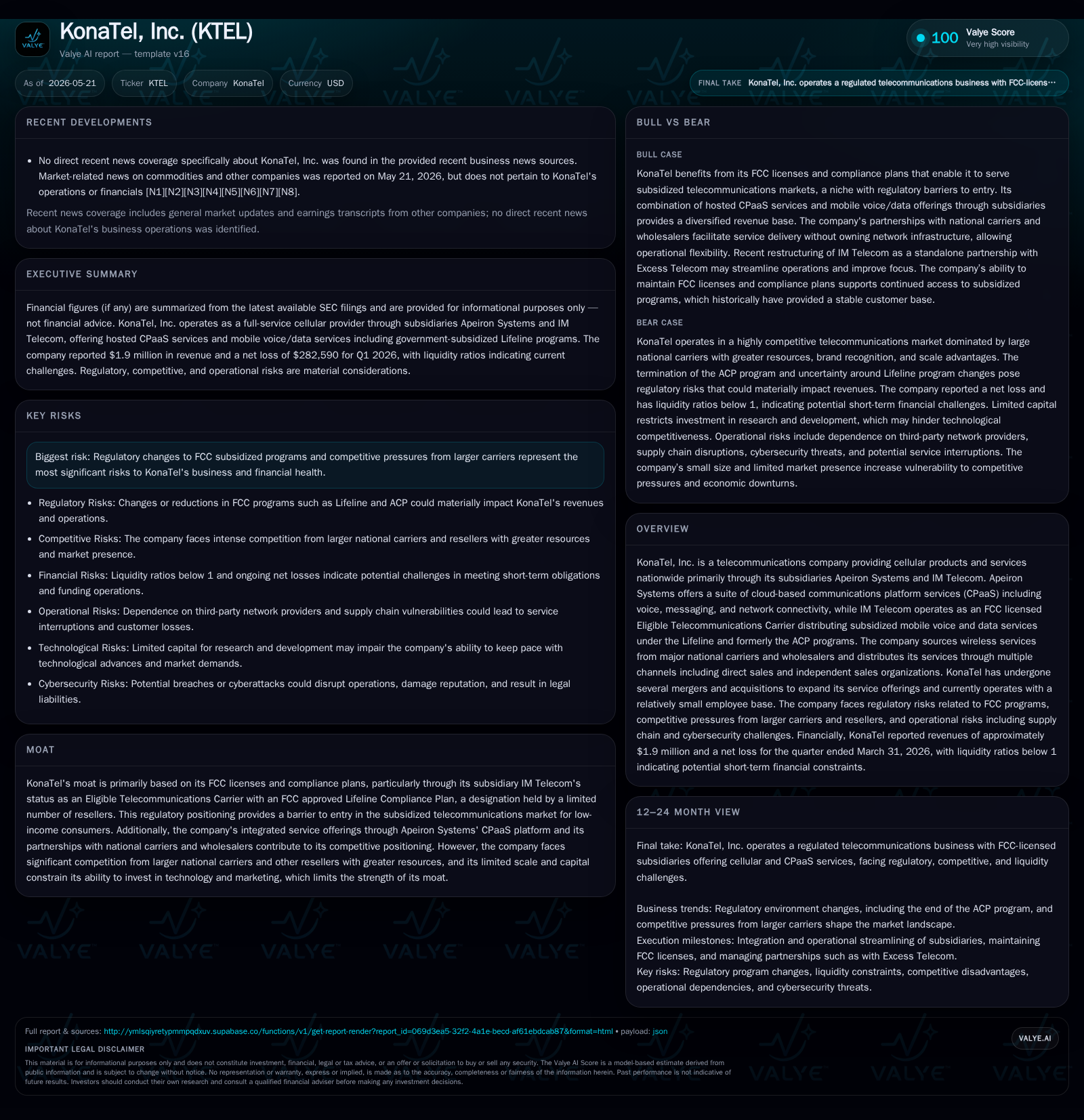

KonaTel's latest quarterly filing reveals a strategic reorganization of its IM Telecom subsidiary into a standalone partnership with Excess Telecom, altering operational and tax reporting structures. This move underscores KonaTel's dependence on FCC-licensed subsidy programs, particularly Lifeline, which impose both barriers to entry and significant regulatory risks. While Apeiron Systems’ CPaaS platform diversifies revenue streams, KonaTel faces competitive pressures from larger carriers and capital constraints that temper its growth prospects. Investors should monitor FCC policy developments, subscriber trends in subsidized markets, and the company’s execution of platform enhancements as key growth indicators.

Latest Quarterly Update: Operating Trends and Near-Term Implications

KonaTel’s most recent Form 10-Q filing dated May 20, 2026 ([S2]) reveals critical operational reorganization within its subsidized service subsidiary IM Telecom. The September 2025 First Omnibus Amendment created IM Telecom as a stand-alone partnership entity owned 51% by KonaTel and 49% by Excess Telecom ([S11]). This restructuring included withdrawing the pending FCC approval application for full transfer ownership and transferring several employees formerly on KonaTel’s payroll to the new entity. Crucially, the combined net income of IM Telecom is now reported on a partnership basis (Form 1065), with KonaTel receiving distributions per a new Distribution Agreement based solely on sales compensation from IM Telecom's vertical sales channels including newly developed healthcare vertical partnerships ([S11]).

This shift terminates the prior Management Agreement tied to IM Telecom operations. Financially, it enabled payment of approximately $700,000 to KonaTel from Excess Telecom’s remaining note receivable balance related to the Initial Closing Date consideration under their Membership Interest Purchase Agreement ([S11]). Notably, the FCC has yet to approve certain ownership transfer conditions as of year-end 2025 ([S15]). This restructuring highlights KonaTel’s strategic aim to preserve operational control while monetizing partial interests in IM Telecom amid regulatory complexities.

IM Telecom also closed its warehouse/distribution center in Tulsa effective July 31, 2025 and maintains headquarters in Plano, Texas with limited full-time employees relative to Apeiron Systems ([S17]). These moves underscore a lean operational footprint focused on compliance-driven participation in subsidized wireless markets.

KonaTel’s Business Model: CPaaS and Lifeline Services Integration

KonaTel's revenue architecture hinges on two principal divisions: Apeiron Systems’ Communications Platform as a Service (CPaaS) suite and IM Telecom’s FCC-licensed subsidized wireless services ([S1], Valye Report Excerpt). Apeiron offers cloud-hosted telephony solutions including VoIP/SIP services, SMS/MMS messaging, call recording, faxing capabilities, and IP network connectivity featuring MPLS and LTE Wireless WAN solutions ([S12]). These products appeal broadly across businesses seeking integrated communication infrastructure accessible via APIs.

Conversely, IM Telecom operates primarily as an Eligible Telecommunications Carrier (ETC), distributing federally subsidized mobile voice/data service under the Lifeline program targeted at low-income consumers. The ACP (Affordable Connectivity Program) previously supplemented this offering until its termination in mid-2024 ([S17]). KonaTel sources wireless capacity wholesale from major national carriers while serving customers through direct and ISO channels (). This dual model attempts to blend scalable technology-driven hosted services with a niche reliance on government-driven subsidy flows.[^note]

The financial interplay involves Apeiron generating recurring service fees largely decoupled from subsidy risk but facing intense competition to innovate rapidly; while IM Telecom's revenue depends heavily on strict FCC program compliance facilitating access to universal service funds ([S1],). Revenue is volume-usage sensitive — subscriber counts matter greatly for scale economies but pricing power is constrained by government caps and carrier agreements.

[^note]: Two distinct customer profiles—enterprise clients favoring Apeiron’s CPaaS solutions versus retail low-income subscribers leveraging IM Telecom's subsidized plans—create diversification but also complexity in channel management.

Competitive Landscape: Position Among National Carriers and Resellers

Within telecommunications industry parameters outlined in the 10-K ([S1]), KonaTel confronts structural competition marked by a division between large facility-based national carriers (AT&T, Verizon, T-Mobile) and smaller resellers like itself. The former enjoy extensive network ownership, substantial capital reserves for R&D/marketing, brand equity benefiting customer acquisition/retention, and broad regulatory influence. In contrast, resellers face cost disadvantages including wholesale fees paid to MNOs (Mobile Network Operators) limiting margin expansion potential.

KonaTel's proprietary licenses as an ETC only partially offset these disparities given it lacks facility ownership or scale benefits. Its CPaaS offerings through Apeiron compete against cloud-native heavyweights and established VoIP providers boasting greater product breadth or deeper integration capabilities (). Moreover, pricing pressures are acute; aggressive discounting tactics by larger peers exert margin compression across subsidized voice/data plans that constitute much of IM Telecom's service base.[^scale]

[^scale]: KonaTel employed only twenty-five full-time employees as of December 2025 compared to thousands at larger peers ([S17]), reflecting scale limitations impacting development velocity and customer support.

Regulatory Environment: FCC Programs as Competitive Barriers and Risks

The cornerstone of KonaTel's competitive moat stems from regulatory licensing rooted in the FCC Eligible Telecommunications Carrier designation secured by IM Telecom along with an approved Lifeline Compliance Plan (,[S1]). This specialized status is held by relatively few resellers owing to stringent FCC requirements instituted since the inception of Lifeline cellular add-ons circa 2009 — notably no new reseller compliance plans have been approved post-2012 ([S5]). The exclusivity erects significant barriers for new entrants seeking access to federal Universal Service Fund reimbursements.

However, this dependence also presents systemic risk. As detailed comprehensively in risk disclosures ([S16],[S23]), any reduction in federal/state subsidy funding levels or termination of Lifeline/ACP mechanisms would profoundly impair revenue visibility. Governmental delays or cutbacks in reimbursement payments exacerbate cash flow uncertainty for carriers reliant on these streams. Given approximately seven million current Lifeline users exist among an eligible pool exceeding thirty-four million nationwide (), policy shifts could be draconian even if politically challenging.

Further complicating matters is ongoing FCC scrutiny over reseller practices affecting program integrity or fraud potential which can impose onerous administrative burdens or injection of compliance costs. Bureaucratic opacity around approval timelines for ownership transfers such as those involving Excess Telecom dilutes deal certainty ([S15],[S11]).

Growth Drivers: Platform Enhancements and Subsidized Market Penetration

KonaTel’s growth strategy endeavors to incrementally augment Apeiron Systems' CPaaS functionality with innovations such as Cloud IVRs refinements, enhanced messaging capabilities including bulk SMS/MMS options, IoT data management improvements, plus expanding dedicated IP network access solutions ([S12]). Such technical enhancements target enterprise customers seeking flexible communication APIs adaptable for a range of vertical applications.

Concurrently its strategy incorporates deepened penetration into eligible low-income consumer segments within states allowing Lifeline services distributed through partnerships alongside Excess Telecom (,[S17]). Maintaining strict adherence to FCC compliance enables sustained access to subsidy funding vital for affordable handset/device distribution facilitated under arrangements like the Installment Sale Agreement with ACP Financing ([S20]).

[^Supply Chain Note]: Access to discounted or refurbished cellular devices compatible with modern LTE/4G platforms supports subscriber acquisition under subsidized programs but requires capital investment managing inventory turnover risks.

Potential acquisition synergies remain available contingent upon regulatory approval evidenced by Tempo Telecom transaction pending review; such consolidation could broaden state-level footprint enhancing scale efficiencies ([S9],).

Overall customer adoption metrics including incremental subscriber count growth within Lifeline demographics serve as key KPIs alongside close monitoring of average revenue per user trends transmitted via periodic SEC disclosures.

Crucial Risks and Constraints: Regulatory Uncertainty and Capital Limitations

Foremost risk remains policy volatility surrounding federally subsidized telecommunications programs that constitute a core revenue pillar especially for IM Telecom operations (,[S16],[S23]). Any contraction or termination could swiftly unravel planned partnership revenues prompting adverse financial consequences.

Competitive pressure imposes margin erosion risk heightened by inability to match marketing spend or technology investments deployed by larger carriers possessing financial muscle beyond KonaTel’s reach. The company cites challenges attracting engineering talent at competitive rates against industry peers hampering timely product evolution required in rapidly shifting communication tech landscape ([S16]).

Financially restricted liquidity constrains operational flexibility; latest companyfacts snapshot shows cash balances approximately $665k versus current liabilities nearing $1.9 million at Q1 2026 quarter-end resulting in sub-1 current ratio (0.59) signifying tight working capital conditions ([F1],[S2]). Debt positions approximating $3.15 million total carry potential refinancing risks given elevated interest rates (15% noted historically) restricting free cash flow generation necessary for growth investments ([F1],[S4]).

Moreover legal completeness over intellectual property rights underlying proprietary software components used within Apeiron products remains subject to industry-standard infringement claims potential adding uncertainty costs ([S16]).

Forward-Looking Considerations: Milestones and Market Signals to Monitor

Stakeholders should closely track several catalysts shaping near-term outlook:

- Updates on FCC rulings affecting Lifeline/Universal Service Fund regulations or emerging subsidy frameworks impacting eligibility/reimbursement rates will materially influence revenue predictability.

- Quarterly disclosures detailing net subscriber additions or churn rates within Lifeline/ACP populations provide leading demand indicators guiding capacity planning.

- Progress on pending regulatory approvals relating to ownership structures involving Excess Telecom partnership modifications could affect consolidation benefits realization [S2][S3].

- Execution cadence around Apeiron Systems’ product rollout schedules featuring enhanced CPaaS service modules especially cloud IVR scalability or IoT device management platforms indicates ability to capture enterprise wallet share amidst competition.

- Management commentary addressing capital raising or cost restructuring initiatives would clarify operational sustainability given current liquidity constraints.

These markers collectively frame potential inflection points illuminating whether KonaTel can convert its unique regulated position into sustainable commercial expansion or confront structural profitability limits.

Financial Overview: Liquidity, Profitability, and Balance Sheet Health

KonaTel's latest financial snapshot portrays constrained liquidity with cash & equivalents totaling roughly $665k as of March 31, 2026 while current liabilities stand at nearly $1.92 million resulting in a precarious current ratio around 0.59 signaling working capital pressure [F1]. Total debt reported at about $3.15 million (last verified end-2022) contributes notable leverage—net debt estimated near $2.5 million after accounting for cash holdings [F1].

On an operating basis for calendar year-end 2025 reported revenues decreased substantially to approximately $8.45 million with operating losses totaling over $2.67 million reflecting ongoing margin challenges exacerbated by elevated cost of revenues exceeding $5.8 million [F1][S1]. Net loss similarly reached around $2.65 million evidencing weak earnings capacity constrained by competitive pricing environments coupled with investment needs for compliance costs.

While steady negative operating margins raise concerns regarding profitability sustainability absent topline growth acceleration or cost discipline improvements management appears reliant on maintaining federal subsidies plus selective platform-driven hosted-service gains as stabilization levers moving forward.

This analysis synthesizes recent filings with industry structural context without providing actionable investment guidance. All information derives from public SEC documents dated through May 20, 2026 unless otherwise noted.

Financial position in context

As of 2026-03-31, companyfacts shows $665068 in cash and equivalents [F1]. Current assets of $1131658 and current liabilities of $1924472 imply a current ratio near 0.59x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments