Lakeshore Acquisition III Corp’s Path Toward a Successful Business Combination

An examination of LCCC’s latest quarterly filing reveals its position in the competitive SPAC landscape and its strategy to secure a value-accretive initial business combination.

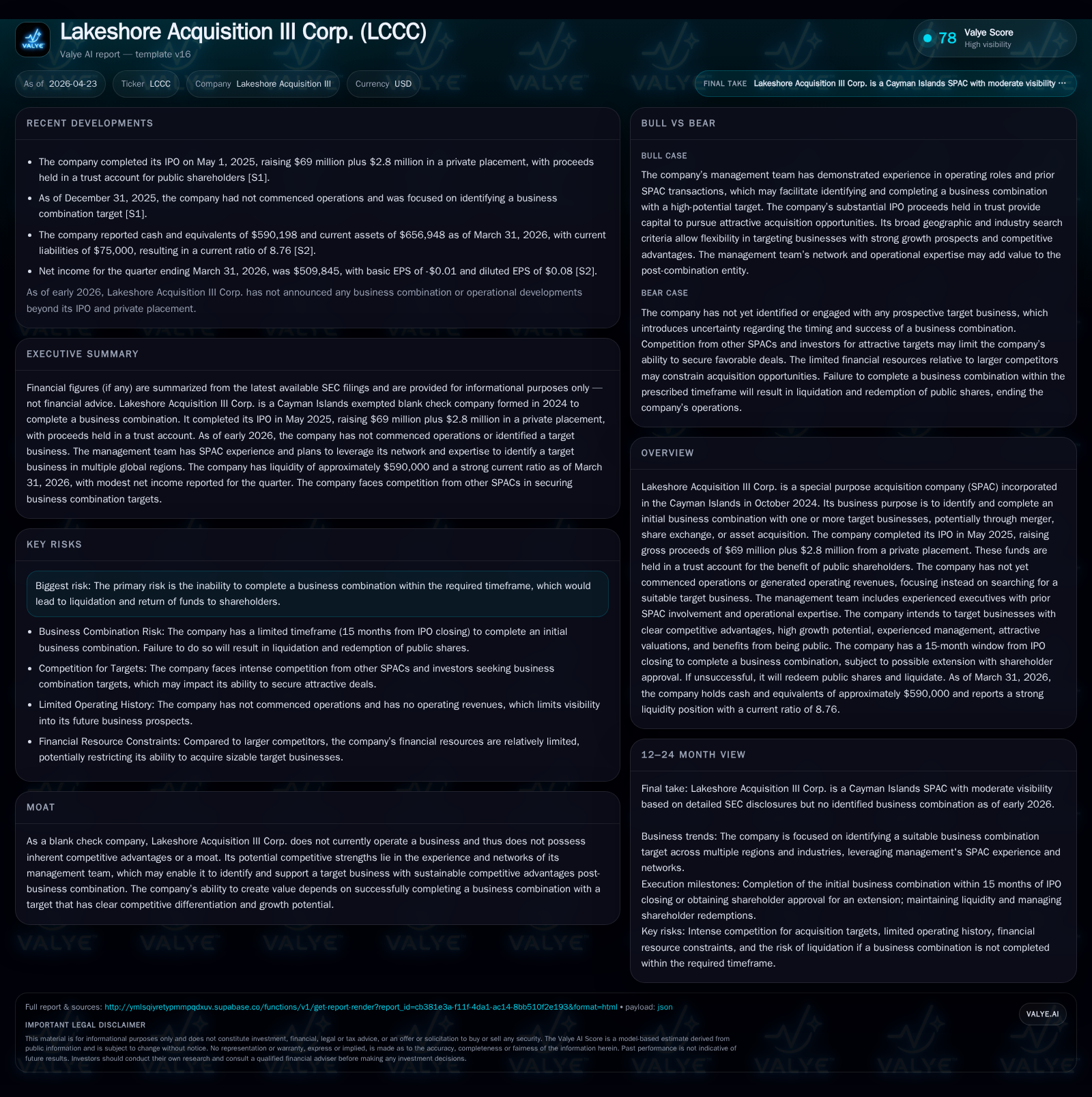

Lakeshore Acquisition III Corp (LCCC) remains operationally inactive as of its April 2026 quarter but maintains strong liquidity within its trust account, underscoring readiness for a prospective business combination. As a blank check company incorporated in the Cayman Islands, its value creation hinges on leveraging an experienced management team to identify and acquire a target with sustainable competitive advantages. Competitive pressures from numerous SPACs and investors limit its target size possibilities given its capital base, but the team’s network and deal execution expertise represent key differentiators. Going forward, monitoring deal announcements and shareholder approvals will provide signals of progress toward consummation.

Latest Quarterly Filing Highlights and Immediate Implications

Lakeshore Acquisition III Corp's latest Form 10-Q filed on April 23, 2026 [S2] presents an unchanged operating picture consistent with its blank check company status. As of March 31, 2026, LCCC holds approximately $590 thousand in cash and equivalents reported outside the trust context [F1], with current assets totaling about $657 thousand against current liabilities near $75 thousand — yielding a robust current ratio of around 8.76. Crucially, these figures exclude the substantial $69 million IPO proceeds plus $2.8 million private placement raised in May 2025 that remain secured in a trust account dedicated solely to protecting public shareholder interests until a qualifying business combination occurs [S1].

No operating revenues were recorded during this period since LCCC has yet to consummate any acquisition or commence operations. All expenditures are administrative and preparatory as the company continues evaluating potential targets. This quarterly disclosure underscores that while commercially inactive today, LCCC maintains financial discipline and liquidity to meet regulatory obligations including the deadline looming August 1, 2026 for completing its initial business combination or seeking shareholder-approved extensions [S14]. This status quo quarter effectively establishes the baseline condition against which any forthcoming transaction-driven transformation will be measured.

Business Model: The Mechanics of a Special Purpose Acquisition Company

LCCC functions purely as a Special Purpose Acquisition Company (SPAC), commonly referred to as a "blank check company," created for the express purpose of raising capital through an IPO—$69 million raised through underwriting including over-allotment—and a concurrent private placement totaling $2.8 million [S1][S4][S6]. Incorporated as an exempted company under Cayman Islands law in October 2024, this offshore domicile offers certain corporate flexibility though it introduces enforceability complexities concerning U.S. securities litigation [S8][S18].

The funds from both offerings are deposited into a trust account pending consummation of one or more business combinations via merger, share exchange, asset acquisition or similar transactions [S1]. Investors initially purchase Units comprising one ordinary share paired with fractional warrants exercisable only after the combination is completed [S1]. Prior to securing a target, LCCC neither generates revenues nor conducts substantive operations—its sole economic activity consists of generating interest income on idle funds [S1]. Financial returns materialize exclusively post-business combination contingent upon successfully acquiring a private operating company deemed suited for public markets.

Key governance mechanisms afford public shareholders redemption rights at about $10 per share if no transaction closes within the prescribed timeframe—thus protecting invested capital while exerting deadline discipline on management [S12]. However, capitalization constraints inherent in SPAC structures mandate careful diligence aligning deal size within available cash plus PIPE (private investment in public equity) raises typically orchestrated alongside transaction announcements.

Management prioritizes leveraging prior SPAC expertise—executives have collectively served on boards or management of four consummated SPAC transactions—to source attractive targets possessing high visible growth prospects and sustainable competitive advantages. The team intends not only to close deals but also deploy operational insights post-combination to enhance acquired company value [S13][S17].

Competitive Dynamics in the SPAC Market and Strategic Differentiators

The special purpose acquisition space remains exceptionally crowded with numerous competing SPAC sponsors alongside traditional private equity firms vying aggressively for appealing targets across sectors identified by LCCC: North America, Latin America, Europe, and Asia [S9][S10]. Many competitors boast superior capital pools or tighter strategic alignment allowing larger transactions or niche market penetration. Relative modesty in LCCC's roughly $71.8 million gross raise positions it towards middle- or lower-tier deal opportunities where transaction sizing aligns with available resources.

This financial constraint creates natural barriers limiting pursuit of large-capitalization targets but does not preclude access to mid-market companies displaying compelling innovation or market positioning requiring partnership support rather than just capital provision [S9]. Consequently, management’s proven ability to identify promising sectors early combined with expansive networks offers differentiation potential unavailable to newer entrants lacking seasoned executive leadership.

Further structural challenges arise because many target companies command premium valuations driven higher by intense bidding among numerous SPAC formations contemporaneously seeking merger partners; this heightens negotiation complexity demanding sharp valuation discipline from sponsors like LCCC [S9][S21]. Hence execution acumen around timing and structuring financial overlays including PIPE arrangements becomes critical for success amid pervasive competition.

Growth Drivers: How LCCC Aims to Build Value Through Its Initial Business Combination

Growth for Lakeshore Acquisition III Corp fundamentally hinges on selecting an acquisition target that satisfies several strategic criteria articulated by management: possessing clear competitive moats difficult to replicate; driven by management teams demonstrating capacity for scaling operations; demonstrating high organic growth drivers along with robust cash flow profiles; presenting valuations that reflect attractiveness relative to comparable publicly listed firms; and benefiting substantively from access to public equity markets post-merger facilitating capital formation or acquisition roll-ups [S1][S13][S21].

Geographically diversified focus across four continents widens potential investment opportunities but demands rigorous diligence frameworks augmenting local knowledge through existing networks ensuring disciplined evaluation [S1][S6]. Emphasizing transformational businesses serving customers innovatively reflects understanding that mere capital injection is insufficient absent genuine structural differentiation.

Post-business combination value-add extends beyond funding into governance support leveraging management’s operational history — refining strategic initiatives, bolstering organizational excellence, navigating regulatory environments inherent in cross-border dealings—and providing public market technical expertise critical during transition phases from private ownership stages [S13][S17]. These non-financial enhancements seek to catalyze market confidence accelerants underpinning longer-term appreciation trends.

Key Risks and Operational Constraints on Completing Target Acquisitions

Several material risks accompany LCCC’s operational narrative; foremost among them is failure to complete an initial business combination before August 1, 2026—or any extended deadline approved by shareholders—that compels mandatory liquidation returning investor funds minus allowable costs [S14][S19]. Such outcomes would extinguish future upside entirely.

Additional pressures arise from fierce bidding conditions driving elevated acquisition multiples constraining ability to negotiate favorable terms amid competing SPACs and alternative financing vehicles like buyout firms employing more flexible investment mandates or larger war chests [S9][S10]. Moreover, regulatory considerations characteristic of Cayman Islands incorporation—while affording tax efficiency—inject legal uncertainties around enforceability of U.S.-based judgments or securities law suits invoking punitive damages which Cayman courts may decline enforcing [S8][S18].

Operational success depends heavily on execution capabilities spanning efficient due diligence processes; timely market communications aligning shareholder expectations; managing necessary approvals including proxy solicitations; structuring sophisticated financing arrangements incorporating warrant holders’ interests among myriad stakeholders; all coordinated within compressed timetable windows typical for SPAC lifecycle progression [S14][S19]. Failure at any juncture heightens risk existentially threatening ongoing viability.

Forward-Looking Signals: What Investors Should Monitor Next

Since LCCC currently lacks active revenue streams or disclosed acquisitions as per latest filings [S2], forward-looking observers should prioritize indicators reflecting advancement toward de-SPAC milestones. Critical events include public announcements regarding Letters of Intent (LOIs) or definitive agreements signaling substantive progress towards identifying suitable target(s) aligned with stated investment parameters [S1][S3].

Subsequent notable markers comprise timely SEC filings describing deal terms including valuation metrics; PIPE financing completions augmenting cash resources supporting broader transaction sizes; shareholder meeting proxies soliciting approval votes contextualizing investor sentiment; changes in reported trust account balances reflecting deal-related expenses deducted once negotiations mature into binding commitments [F1][S12][S16].

Transparency around deviations such as requests for extensions exceeding original deadlines would also communicate management’s assessment regarding pace toward consummation ultimately influencing perceptions of operative credibility versus liquidation threats. Thus attention over coming quarters will crystallize narrative trajectories guiding risk/reward calibration.

Supporting Financial Overview: Capital Structure and Liquidity Position

From a financial standpoint anchored by disclosures as of March 31, 2026 [F1], Lakeshore Acquisition III Corp retains cash & equivalents at approximately $590 thousand reported outside direct trust account funds presented in SEC statements--with current assets standing near $657 thousand versus current liabilities about $75 thousand yielding a comfortable current ratio near 8.76 indicative of sound short-term liquidity management unaffected by operational burdens typical for blank check companies.

Operating income remains negative reflecting ongoing administrative costs without associated revenues (-$600K year ended Dec 31, 2025), while net income shows positive due solely to non-operating items like interest income ($1.25M net income end-2025) consistent with expectations for dormant pre-merger entities focused entirely on preserving shareholder investment while questing for suitable acquisition candidates [F1].

Leverage is absent as no debt obligations are assumed reflecting conservative balance sheet priorities emphasizing protection of IPO proceeds segregated under trust arrangements ensuring investor capital return rights absent business combination completions—reinforcing core promise fundamental for maintaining confidence within heavily scrutinized SPAC frameworks.

This analysis synthesizes information derived from recent quarterly filings (Form 10-Q dated April 23, 2026), annual disclosures (Form 10-K dated February 4, 2026), and accompanying SEC documentation without speculative extrapolation beyond stated facts. It does not offer investment advice but aims to provide industry-focused insights into Lakeshore Acquisition III Corp’s positioning within the evolving SPAC ecosystem.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments