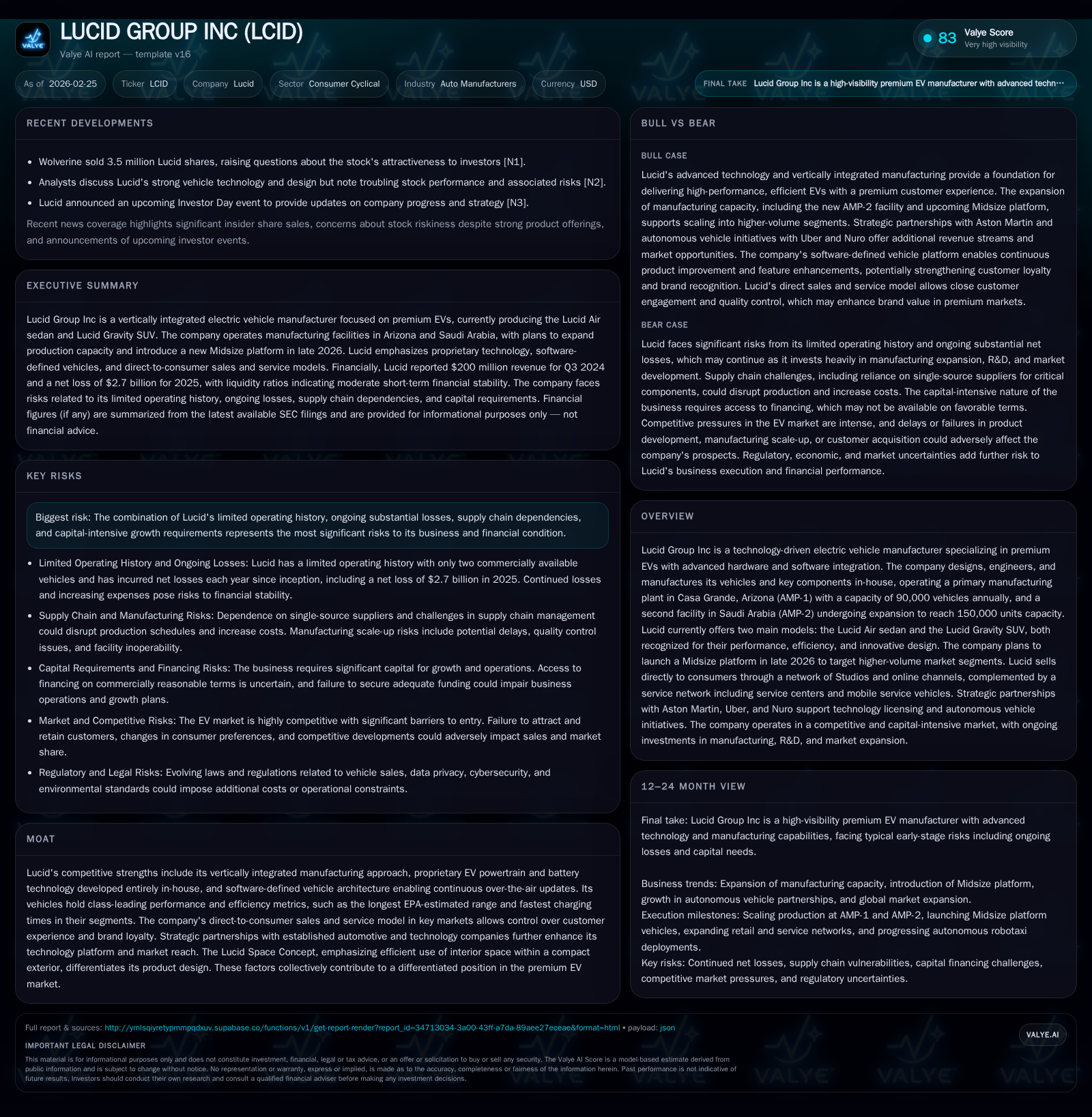

Lucid Group Inc’s Challenge of Scaling Premium EVs While Managing Mounting Losses

Lucid combines technological innovation and vertical integration with severe financial pressures amid an evolving EV market.

Lucid Group Inc has distinguished itself in the premium electric vehicle space via proprietary technology and a vertically integrated manufacturing model focused on high-performance, efficient vehicles. However, its historically limited model lineup and substantial operating losses reflect significant scaling hurdles. The company aims to expand capacity, including a new midsize platform planned for late 2026, but must navigate operational risks, supply constraints, and capital demands. Financial metrics reveal mounting cash burn and negative returns on equity, underscoring the challenge of advancing from niche innovation towards profitable volume production.

Lucid’s Historical Revenue Growth and Profitability Trends

Since beginning deliveries of the Lucid Air sedan in late 2021 and the Lucid Gravity SUV in late 2024, Lucid’s revenue trajectory reflects its early-stage operations. Revenue grew from $27 million in FY2021 to $608 million in FY2022 but declined slightly to $595 million in FY2023. Latest trailing data shows a sharp slowdown to approximately $200 million as of September 2024, indicating challenges scaling beyond niche volumes [F1].

Operating income has been consistently negative, worsening alongside increased investments in manufacturing capacity and research & development. Losses expanded from about -$2.59 billion in FY2022 to nearly -$3.10 billion in FY2023, then -$3.02 billion in FY2024, culminating at approximately -$3.50 billion for FY2025. Net losses followed similar trends with -$2.7 billion recorded in FY2025 [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -2.7 | -2.9 | -3.5 | +0.6% | ||

| 2024 | -2.7 | -2.0 | -3.0 | +4.0% | ||

| 2023 | 595 | -2.8 | -2.5 | -3.1 | -2.1% | -116.8% |

| 2022 | 608 | -1.3 | -2.2 | -2.6 | +2143.3% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | -3.8 | -376.1 | |

| 2024 | -2.9 | -70.1 | |

| 2023 | 0 | -3.4 | -58.3 |

| 2022 | 0 | -3.3 | -30.0 |

Source: SEC companyfacts cache [F1].

*Revenue data for FY2025 is not fully available; latest quarterly figures indicate significant slowdown.

These figures underscore the substantial costs associated with transitioning from boutique EV manufacture toward scalable volume production.

Operational Drivers Behind Revenue and Loss Trends

Lucid’s revenue performance reflects reliance on a limited product lineup featuring the Lucid Air and Gravity models [S1][S5]. Although AMP-1 manufacturing capacity was expanded to 90,000 vehicles annually by 2024, production is constrained by supply chain challenges—particularly single-source lithium-ion battery cell suppliers—which limit output scalability and elevate unit costs [S4][S6].

Vertical integration adds fixed costs as Lucid develops proprietary powertrains, batteries, and software-defined vehicle architectures requiring ongoing investment without immediate volume offsets [N1][N2]. Competition within premium EV segments intensifies margin pressures.

The direct-to-consumer sales model via retail studios and online platforms involves upfront customer engagement expenses aimed at building brand loyalty among luxury buyers accustomed to traditional dealership experiences [S5][S8]. Global economic uncertainties further weigh on consumer purchasing decisions for high-ticket items like EVs.

Technological Differentiation and Product Design Innovations

Key technological advantages include:

- Proprietary powertrain innovations: Miniaturized drivetrain components reduce weight while delivering superior efficiency and performance within their class [S14].

- Advanced battery technology: In-house battery system development focusing on energy density and thermal management supports market-leading range and charging speeds per EPA estimates [S14].

- Software-defined vehicle architecture: Over-the-air updates enable continuous feature improvements post-sale; foundational for future ADAS Level 4 autonomy applications including ride-hailing use cases [S1][S14].

- Design philosophy: The Lucid Space Concept maximizes interior volume through smaller exterior footprints compared to hybrid-adapted platforms used by competitors [S14].

These elements create a technical moat supporting premium positioning but require sustained R&D investment.

Outlook: Midsize Platform Launch and Global Manufacturing Expansion

Lucid plans to expand its addressable market by launching three new Midsize platform vehicles starting late 2026 targeting higher-volume segments beyond its current offerings [S1][N3][N9]. This strategy aims to unlock economies of scale absent from prior generations.

Additionally, AMP-2 facility in Saudi Arabia is ramping up from semi-knockdown assembly toward full-scale completely built unit (CBU) production targeting an annual capacity of up to 150,000 vehicles. This geographic diversification seeks cost benefits alongside capacity growth [S13].

Execution risks remain considerable given historical delays coupled with complexities of international model launches amid volatile supply chains and regulatory environments.

Supply Chain Vulnerabilities and Production Risks

Dependence on single-source suppliers for key components like lithium-ion batteries heightens supply chain risk that could disrupt production cadence despite expanded manufacturing capacity at AMP-1 [S4][S6][S9][S10]. Such vulnerabilities are common industry-wide but more acute here due to limited scale.

Tariff exposure and geopolitical trade uncertainties add cost pressures on raw materials unless mitigated through strategic sourcing partnerships underway at critical mineral levels [S25].

Capital Allocation, Cash Flows, and Equity Positioning

Lucid’s capital deployment remains focused on heavy investment with capex around $870–$910 million annually directed at scaling manufacturing plants and technology platforms while operating cash flows remain deeply negative—over $2.9 billion outflow recorded in FY2025 alone [F1].

The equity base contracted markedly from about $4.85 billion at end-FY2023 down to roughly $717 million at end-FY2025 due to cumulative losses eroding retained earnings alongside potential dilution effects from financing activities detailed elsewhere [F1][S7][S12].

No dividends have been paid nor share buybacks conducted recently consistent with growth-stage capital retention norms.

Return on Equity and Liquidity Metrics Highlight Financial Strains

Calculated ROE stands near negative 376% based on latest net income relative to equity illustrating severe loss absorption overwhelming shareholder capital contributions so far [F1].

Liquidity indicators show current assets around $3.30 billion versus current liabilities near $2.63 billion yielding a current ratio of approximately 1.25—providing some short-term cushion though reliant on continued access to capital markets amid ongoing cash burn [F1][S7][S19].

These metrics highlight the imperative for revenue growth paired with improved operational efficiency before profitability becomes feasible.

Competitive Landscape and Market Risks Impacting Growth Prospects

Legacy automakers benefit from established dealer networks and broader product portfolios including hybrids which provide competitive advantages over Lucid's limited lineup thus far [S14].

Customer acquisition costs under direct-to-consumer strategies contrast with franchise models favored by traditional luxury brands impacting brand recognition especially outside core U.S., Middle East, and emerging European markets where expansion efforts continue [S5][S8].

Charging infrastructure partnerships including conditional access to Tesla’s Supercharger network mitigate but do not eliminate user experience risks amid uneven public charging deployment patterns [S7].

Macroeconomic uncertainty further weighs on discretionary spending affecting uptake of premium-priced electric vehicles.

Investor Considerations: Monitoring Milestones and Cash Burn Trajectory

Critical upcoming milestones include the commercial launch of Midsize platform vehicles targeted for late 2026—a key test of product acceptance and operational scalability linked closely with AMP-2 expansion progress [N3][N9].

Quarterly earnings will be important indicators for revenue inflection points alongside reductions in operating losses or improvements in adjusted margins excluding fixed cost leverage effects.

Free cash flow remains deeply negative—estimated around minus $3.8 billion most recently—signaling dependence on capital raises absent rapid margin improvements necessitating disciplined expense control plus potential strategic partnerships or financing transactions yet unconfirmed publicly [F1][N8][N13].

This analysis is based solely on publicly available information as of February 2026 without any forward-looking statements or investment advice implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments