Ethos Technologies Revolutionizes Life Insurance with Digital Platform Growth

Strong Q1 2026 operational momentum highlights expansion of Ethos’s digital platform, agent productivity gains, and carrier collaborations fueling scalable commissions.

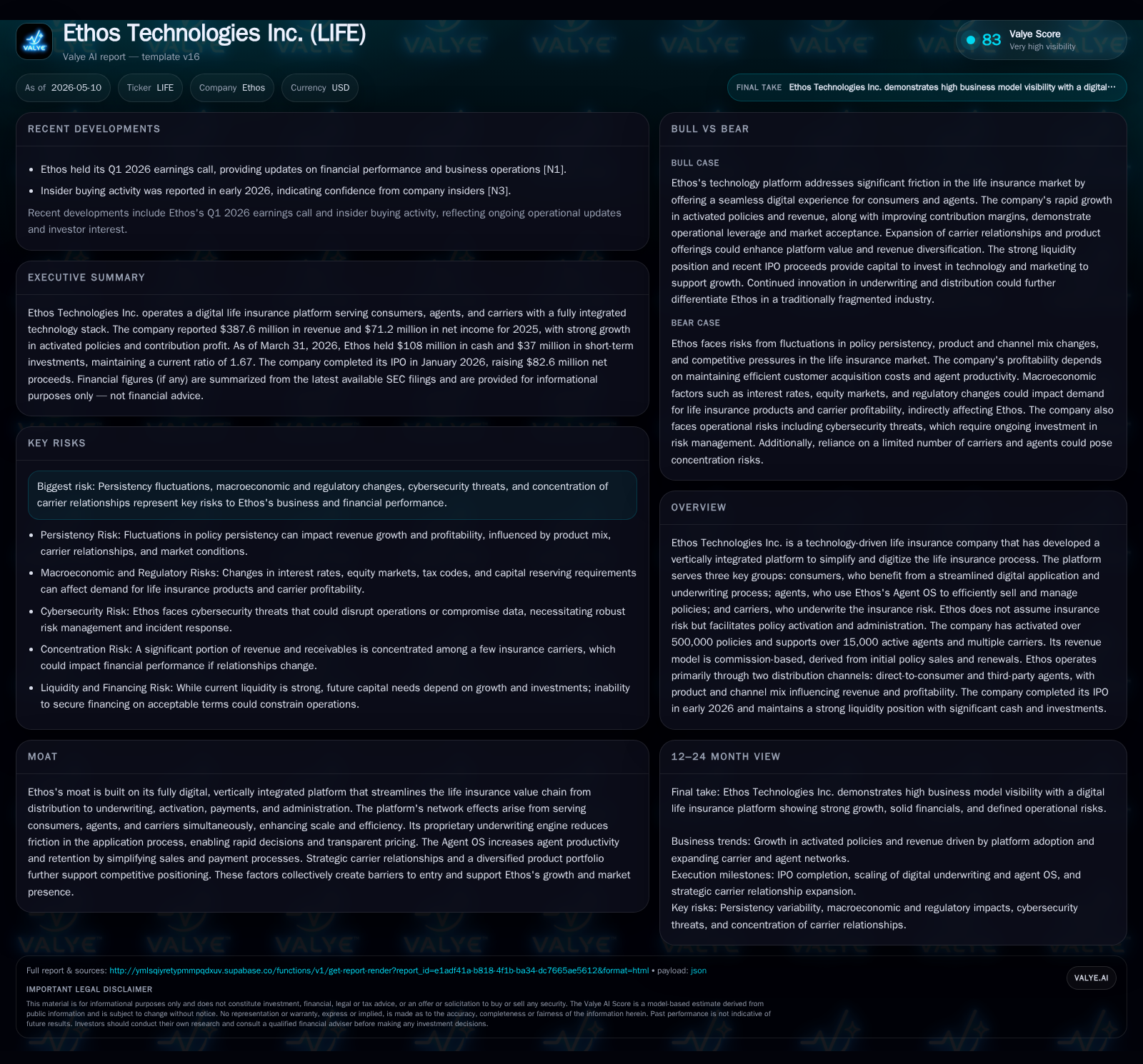

Ethos Technologies reported robust progress in Q1 2026 with active policy count surpassing 500,000 and a growing agent base exceeding 15,000, reflecting solid adoption of its vertically integrated life insurance platform. The company’s commission-based revenue benefits from increasing policy activations and renewals supported by its proprietary underwriting engine and Agent OS productivity tools. Strengthening carrier partnerships and diversified distribution channels underpin Ethos’s position within the fragmented life insurance technology landscape. Near-term growth hinges on scaling consumer and agent engagement alongside new product introductions, while managing persistency and regulatory risks remains pivotal.

Latest Quarterly Operating Update: Momentum from Q1 2026 Results

Ethos Technologies' latest quarterly filing for Q1 ended March 31, 2026 ([S2]) reveals continued operational momentum. The company reported its active policies have now exceeded the milestone of 500,000 activated policies—a key indication of growing consumer adoption. Concurrently, Ethos supports a network of over 15,000 active agents utilizing its proprietary Agent OS platform ([S2], [N1]) which streamlines sales workflows and policy management. This reflects sustained agent engagement critical to expanding third-party distribution channel revenues.

The May 6 event filing ([S3]) supplemented these disclosures by highlighting ongoing enhancements to the digital platform aimed at improving user experience for both consumers and agents. Combined with the Q1 earnings call transcript ([N1]), this confirms Ethos is capitalizing on increased commission income driven by higher policy sales volume and improving retention reflected in early renewal metrics.

Overall, the operational data suggest the platform's network effects are strengthening as more agents leverage Agent OS productivity tools and carriers expand offerings through Ethos's integrated system.

Business Model and Platform Overview: Vertical Integration Unlocking Efficiency

Ethos Technologies functions as a technology-driven life insurance intermediary that owns no underwriting risk but facilitates an end-to-end digital process from consumer application through to policy activation and administration ([S1], Valye_report_excerpt). The company's vertically integrated platform serves three key constituencies:

- Consumers benefit from digitized application flows allowing quick approvals via an automated underwriting engine that reduces traditional frictions in life insurance purchases.

- Agents, through Ethos's Agent OS software, gain streamlined tools for managing sales pipelines, processing commissions efficiently, and handling renewals—all designed to optimize productivity and retention.

- Insurance Carriers partner with Ethos by underwriting the actual risk while relying on Ethos’s infrastructure for policy issuance and lifecycle management.

Revenue primarily derives from commissions paid by carriers based on new policy activations and renewals in both direct-to-consumer (DTC) sales and third-party agent channels ([S1]). Product mix varies across term life, whole life, and indexed universal life insurance offerings; each differs in average premiums, commission rates, persistency profiles, influencing unit economics ([S28]). This model enables Ethos to scale without direct exposure to underwriting losses while harnessing network synergies among participants.

Competitive Setting and Industry Dynamics: Network Effects and Carrier Partnerships

The US life insurance industry remains fragmented with a growing shift toward digitization. Within this setting, Ethos distinguishes itself by deploying a fully integrated digital ecosystem that connects consumers, agents (via Agent OS), and carriers on one platform (, [S1]). This integration reduces underwriting friction—a notable competitive lever—by accelerating decision-making timelines through proprietary algorithmic underwriting capabilities.

Ethos’s multi-sided platform engenders network effects: more consumers attract additional agents seeking efficient sales tools; more agents bring carrier partners motivated by increased policy flow. This concentric value creation enhances switching costs for agents who benefit from streamlined commission processing and data analytics embedded in Agent OS.

Primary competitors include digital brokers focusing solely on distribution or traditional carriers expanding their internal technology but lacking Ethos’s breadth of vertical integration. The company’s strategic carrier relationships provide scale advantages yet concentration risk remains notable as few large carriers constitute majority revenue share ([S28]). Persistency rates—a structural determinant of lifetime customer value—remain a critical metric dictating renewal commissions sustainability.

Growth Drivers: Scaling Consumers, Agents, and Carrier Collaborations

Ethos's expansion hinges on several measurable drivers:

- Agent Network Growth: Active agent count above 15,000 signals healthy adoption of the Agent OS toolset which enhances productivity via simplified payment mechanisms and CRM functionalities ([S2], [N1]). Increasing agent retention helps stabilize recurring commission streams.

- Consumer Engagement: Digital-first application processes reduce acquisition cycles boosting conversion rates for both DTC customers and third-party referrals. Simplification fuels volume growth in new policies activated each quarter.

- Carrier Partnerships: Broadening carrier participation expands product variety enabling tailored solutions per demographic segments improving overall market penetration ([S28]). These collaborations deepen integration with underwriting engines supporting faster policy issuance.

- Technology Investment: Continued capital allocation towards advanced automation in underwriting processes enhances speed while potentially improving loss ratios by better risk assessment ([S22]).

Together these trends support margin uplift prospects as fixed technology costs leverage incremental volume growth alongside improved persistency enhancing long-term cash flow visibility.

Risks and Constraints: Persistency, Regulation, and Relationship Concentration

Ethos discloses several watchpoints shaping its operating landscape:

- Persistency Fluctuations: Renewal commission income depends heavily on customer retention—variability here can materially impact revenue forecasts given elongated premium collection windows ([S1], Valye_report_excerpt).

- Regulatory Environment: Life insurance regulations vary regionally; evolving compliance requirements around underwriting standards or consumer disclosures could raise operational complexity or constrain product innovation ([S1]).

- Cybersecurity Threats: As a digital-native entity hosting sensitive personal data on its platform, Ethos prioritizes cyber risk management overseen by an experienced Chief Information Security Officer (CISO) supported by multidisciplinary teams for incident detection/response ([S1]). Despite robust protocols there remains potential exposure to data breaches affecting reputation or incurring fines.

- Carrier Concentration Risk: Revenue concentration with a few major carrier partners exposes vulnerability should partnership terms shift unfavorably or carriers opt to internalize certain functions ([S28]). Diversifying carrier relationships is thus strategically imperative.

Management appears conscious of these challenges with governance structures actively monitoring risks alongside investments in security infrastructure ( [S1]).

Key Upcoming Catalysts and What to Watch Next

Looking ahead, key performance indicators will revolve around:

- Quarterly Policy Activation Volumes: Trends indicating sustained new sales velocity underpin near-term top-line growth potential ([S3], [N1]).

- Agent Onboarding Rates: Changes in active users of Agent OS reveal how effectively Ethos is converting agents into loyal users who drive recurring revenues.

- Carrier Expansion Announcements: New partnerships or product launches enhance addressable market size; announcements monitored via SEC events or investor communications will be pivotal.

- Regulatory Developments: Updates impacting digital insurance delivery models may influence compliance cost structures or necessitate platform adaptations.

- Technological Enhancements: Deployment of new features aiming to streamline underwriting further or improve analytics capabilities serve as execution milestones signaling competitive advantage preservation.

Financial Snapshot: Balance Sheet Strength and Profitability Metrics

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $108mm | |

| 2026-03-31 | ||

| Current assets | $259mm | |

| 2026-03-31 | ||

| Current liabilities | $155mm | |

| 2026-03-31 | ||

| Current ratio | 1.67x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Ethos concludes Q1 2026 with a robust financial position supported by $107.9 million in cash & equivalents alongside $259.4 million current assets against $155.0 million current liabilities—yielding a comfortable current ratio of 1.67 confirming liquidity adequacy for operational needs ([F1], [S2]).

No immediate debt or covenant concerns were flagged in recent filings suggesting balance sheet flexibility remains intact to pursue growth initiatives without excessive leverage pressures ([S2], [F1]).

This analysis is based exclusively on publicly filed documents including the latest quarterly (10-Q), annual (10-K), recent event (8-K) submissions from Ethos Technologies Inc., complemented by primary news transcripts as noted. It aims solely to synthesize operating developments within the context of industry fundamentals without providing investment guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments