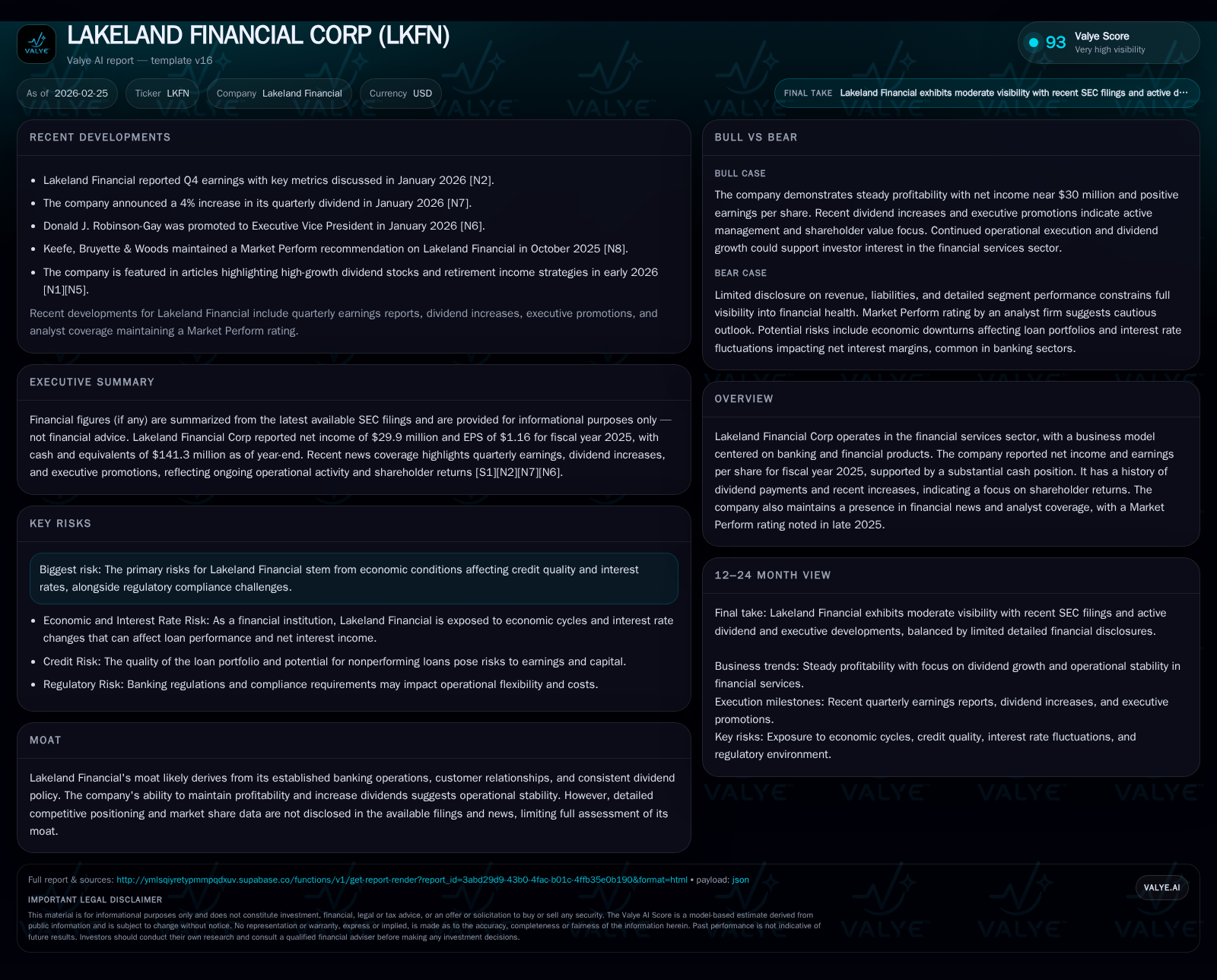

Lakeland Financial’s 2025 Profit Surge Supports Dividend Growth and Capital Returns Amid Interest Rate Uncertainties

After a strong net income rebound in 2025, Lakeland Financial Corp raised dividends and expanded buybacks, balancing shareholder returns with capital preservation.

Lakeland Financial Corp posted a 23.6% year-over-year increase in net income for fiscal 2025, recovering from a prior year dip. This earnings momentum underpinned a 4% dividend hike and a meaningful acceleration in share repurchases, reflecting management’s commitment to shareholder value. While operating cash flow increased moderately alongside higher capital expenditures, the company maintains robust liquidity and an equity base fortified by consistent retained earnings growth. Going forward, Lakeland faces the challenge of navigating possible headwinds from economic cycles affecting credit quality and interest rate fluctuations, with no explicit revenue or operating income guidance disclosed yet.

Historical Performance Highlights

Lakeland Financial Corp's fiscal 2025 performance revealed a meaningful rebound characterized by a net income increase to nearly $30 million, up from $24.2 million the previous year—a hefty gain of approximately 23.6% after a dip seen between 2023 and 2024 [F1]. This resurgence marks a return toward pre-2024 earnings levels (FY2023: ~$29.6 million), indicating operational stability during competitive pressures and financial market volatility.

Operating cash flows rose moderately by about 12%, totaling roughly $114.9 million for the year, albeit accompanied by a near-29% increase in capital expenditures reaching $11.1 million [F1]. The elevated capex spend suggests strategic investments in infrastructure or technology upgrades—typical for regional banks seeking efficiency gains or branch modernization.

Equity shareholders saw their stake appreciate as stockholders' equity climbed from $683.8 million in 2024 to $762.4 million by December 31, 2025, driven largely by retained earnings accumulation rather than aggressive buybacks which remain modest relative to equity size [F1]. Indeed, while share repurchases picked up notably—from around $0.6 million in FY24 to over $20 million in FY25—they still represent a minor fraction of total capitalization.

Financial Summary Table

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 30 | 115 | 11 | +23.6% |

| 2024 | 24 | 102 | 9 | -18.3% |

| 2023 | 30 | 114 | 6 | +14.0% |

| 2022 | 26 | 169 | 5 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 51 | 20 | 104 |

| 2024 | 49 | 1 | 94 |

| 2023 | 47 | 1 | 108 |

| 2022 | 41 | 1 | 165 |

Source: SEC companyfacts cache [F1]. | *Limited data points; exact YoYs approximate.

FY = Fiscal Year; NetInc = Net Income; CFO = Operating Cash Flow; Capex = Capital Expenditures; ROE = Return on Equity

Drivers Behind Past Trends

Lakeland's income rebound likely reflects improved net interest margins benefiting from rising rates earlier in the cycle, combined with stable fee income streams derived from diversified banking products including commercial loans and financial services [S1][N1]. However, explicit revenue or segment profitability data is not disclosed publicly, limiting granular insight.

Cash flow robustness underscores effective core operations with controlled working capital needs despite higher capex outlays associated perhaps with branch upgrades or digital platform investments designed to enhance customer retention and compliance capability—critical given evolving regulatory frameworks affecting mid-sized banks [S1][S2].

The company sustained dividend increases (notably announcing a fresh quarterly dividend hike of roughly +4% in January 2026), reflecting confidence in ongoing cash generation capacity and stable reserve management aligned with shareholder expectations for steady returns typical for regional financial institutions [N9][N5].

Forward Growth Prospects & Constraints

Looking ahead, Lakeland Financial's growth hinges on successfully capitalizing on favorable interest rate environments without degrading asset quality through aggressive loan growth or credit risk deterioration—a common vulnerability given its sizable commercial real estate and agricultural lending exposure within its portfolio [S4][S7]. Recent management promotions indicate efforts to reinforce leadership preparedness amid such cyclical risks [N8].

Notably absent is explicit management guidance or projected financial milestones regarding revenue or margin expansion from the latest filings or news releases [N3][S3], implying cautious optimism amidst macroeconomic uncertainties.

Industry analysis suggests that regional banks like Lakeland contend with margin compression risks should interest rates decline unexpectedly or if competitive pressures intensify due to fintech disintermediation or regulatory cost burdens.

Capital Allocation & Returns Analysis

Lakeland exhibits balanced capital deployment: dividends accounted for about $51 million in payouts during FY25, consistent with a progressive dividend policy that has been incrementally increased over recent years [F1].[N9] Meanwhile, buybacks surged substantially but remain moderate relative to total equity—signaling opportunistic share repurchases rather than systemic capital return strategy.

Calculated approximate ROE at around 3.9% (Net income over Equity) signals restrained leverage usage characteristic of prudent risk management but comparatively low profitability leverage versus peers—potentially reflective of conservative lending standards or pricing discipline under economic tightening phases.

Free cash flow remaining consistently positive at approximately $103.8 million (Operating cash flow minus capex) supports both ongoing investment needs and shareholder distributions without compromising liquidity buffers (Cash & equivalents stood at ~$141 million year-end FY25) [F1][S10].

Key Considerations & Risks

Primary risks identified include exposure to fluctuating credit quality linked to economic cycles impacting commercial real estate and agricultural sectors—a meaningful portfolio concentration area per filings—plus sensitivity to volatile interest rate movements affecting net interest margins even as loan yield repricing may lag deposit cost adjustments [S2][S4][S6].

Regulatory compliance costs and evolving capital requirements present additional challenges for mid-sized banking operations balancing growth ambitions against compliance overheads.

Monitoring quarterly updates will be essential to track progress on asset quality metrics and potential signs of margin pressure or credit provisioning changes given lack of full transparency on segment breakdowns currently.

Conclusion

Lakeland Financial Corp delivered solid net income growth in fiscal year 2025 along with robust operating cash flows supporting enhanced shareholder returns via dividends and expanded share repurchase activity—a testament to operational resilience amidst sector headwinds.

However, established strengths come paired with typical mid-sized bank tradeoffs: moderate ROE requiring sustained efficiency measures alongside vigilant credit risk oversight particularly related to commercial real estate and agriculture lending exposures.

Absent detailed forward guidance from management, observers should focus on upcoming quarterly indicators around loan portfolio performance, margin trends, and capital deployment strategies as key bellwethers for continued value creation.

This report is prepared solely for informational purposes based on publicly available data as of early 2026 without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments