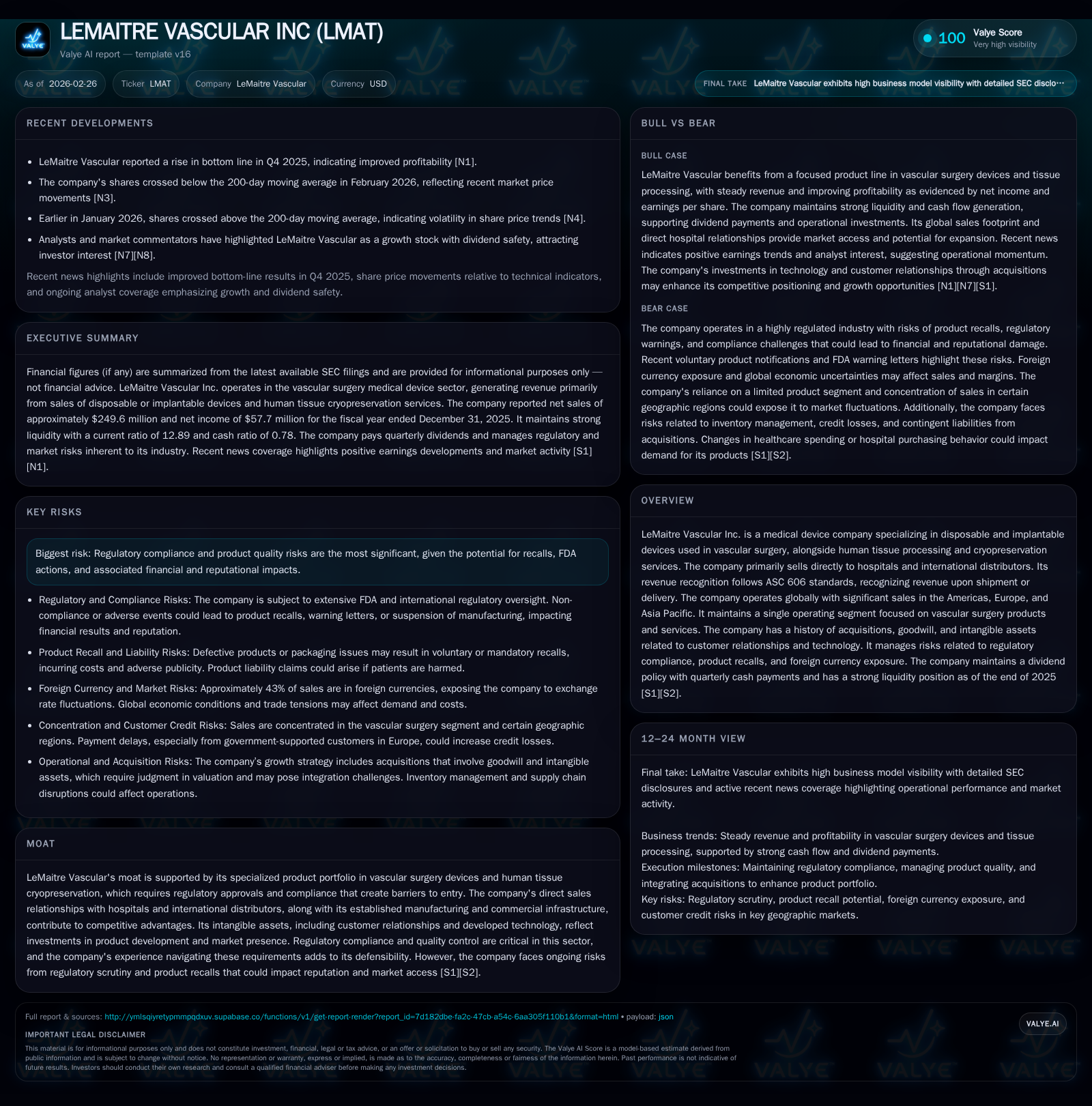

LeMaitre Vascular’s Steady Profit Growth Supported by Diversified Vascular Surgery Products and International Expansion

Specialized medical devices and tissue services underpin LeMaitre Vascular's expanding global footprint and improving financial returns.

LeMaitre Vascular Inc. leverages a focused portfolio of vascular surgery devices and human tissue cryopreservation services to fuel steady revenue and profit growth. The company’s direct sales model to hospitals and distributors spans the Americas, Europe, and Asia Pacific, supporting top-line expansion from $193.5 million in 2023 to nearly $250 million in 2025. Rising net income reflects operational leverage despite ongoing regulatory and quality risks inherent in the sector. Capital allocation emphasizes consistent dividends alongside cautious buybacks, supported by strong operating cash flows exceeding $81 million in 2025. Future growth will hinge on navigating complex regulatory environments while expanding international penetration and maintaining innovation in specialized products.

Company Overview

LeMaitre Vascular Inc. specializes in medical devices used primarily in vascular surgery, encompassing disposable and implantable devices along with human tissue processing and cryopreservation services [S1]. It operates a single segment focused exclusively on vascular products sold through direct channels to hospitals globally as well as through international distributors [S8][S11]. This singular operating segment strategy emphasizes deep expertise within a niche medical device category characterized by substantial regulatory hurdles that act as barriers to entry.

Historical Financial Performance

Over recent years, LeMaitre has demonstrated robust growth across its core financial metrics (see table). Revenue climbed steadily from approximately $193.5 million in FY 2023 to nearly $250 million by FY 2025 — representing a meaningful increase supported by geographic expansion into Europe, the Middle East, Africa, Asia Pacific, alongside sustained strength in its American markets [F1][S11]. Net income surged significantly from about $8.47 million to over $57.7 million within the same period — reflecting considerable margin expansion presumably driven by operational leverage alongside disciplined expense management [F1][S16].

Capital expenditure remains moderate relative to cash flows generated; capex includes property and equipment purchases disclosed at approximately $6.8 million for FY 2025 [F1][S21]. Operating cash flows more than doubled between FY 2023 ($36.8M) and FY 2025 ($81.3M), underscoring strong underlying business cash generation capacity validated by consistent net income growth coupled with disciplined working capital management [F1][S21]. Cash & equivalents increased slightly year-over-year reaching $28.2 million at year-end FY25 providing liquidity cushion.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 58 | 81 | 68 | +31.1% |

| 2024 | 44 | 44 | 52 | +420.2% |

| 2023 | 8 | 37 | 10 | +50.4% |

| 2022 | 6 | 25 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | ROE% |

|---|---|---|---|

| 2025 | 18 | 1821000 | 14.7 |

| 2024 | 14 | 1719000 | 13.1 |

| 2023 | 12 | 853000 | 2.8 |

| 2022 | 11 | 642000 | 2.1 |

Source: SEC companyfacts cache [F1].

Note: Capex estimated from property & equipment purchases disclosed [S21]

Revenue Breakdown & Geographic Performance

Sales remain concentrated geographically but with diversification: approximately two-thirds of revenues derive from the Americas while Europe MEA contributes about 29% and Asia Pacific just under 7% as of FY25 [S11]. This reflects leveraging of domestic direct sales complemented by international distributor channels facilitating penetration into regulated foreign markets requiring distinct product approvals.

Direct hospital relationships enhance customer retention while distribution partners extend reach—typical for specialized medtech firms balancing high service demands alongside localized regulatory requirements.

Regulatory Environment & Risks

LeMaitre operates under stringent FDA regulation as well as parallel authorities abroad such as the EU Medical Device Regulation (MDR). The company recently addressed a voluntary product packaging seal issue affecting certain catheter lines; this notification did not materially impact financial results but illustrates ongoing vigilance required within the sector [S19].

The firm also faces clinical regulatory risk exposure inherent to the vascular surgical device industry including potential recalls or FDA warning letters; no material litigation or claims have arisen recently though these remain key risk factors [S4][S17]. Continuous investment into quality assurance systems, post-market surveillance, and compliance processes remains essential.

Capital Allocation & Returns

The company maintains a disciplined capital allocation approach balancing shareholder returns with prudent financial management. Quarterly dividends have increased over time culminating at $0.20 per share quarterly during fiscal year 2025 totaling approximately $18 million paid out — illustrating a stable cash return policy anchored by solid earnings generation capability [F1][S13][S26].

Share repurchases are modest relative to market capitalization but represent opportunistic capital return aligned with internal funding priorities; approximately $1.8 million was deployed for buybacks in FY25 [F1][S14].

Balance sheet strength is evident with equity nearing $394 million at year-end FY25 supporting flexibility alongside manageable liabilities including convertible senior notes totaling about $169 million [F1][S18]. The company’s approximate return on equity stands around mid-teens (~14.7%) reflecting efficient use of equity capital driven by profitability improvements.

Future Growth Prospects

Growth drivers include further international market penetration leveraging distributor networks; incremental product enhancements within vascular surgery niches; leveraging acquired technologies for cross-selling opportunities; and secular demand trends driven by aging populations increasing peripheral arterial disease prevalence globally.

Challenges include intensifying global regulatory scrutiny especially within EU jurisdictions post-MDR implementation alongside pricing pressures from healthcare cost containment measures internationally.

Navigating these dynamics successfully will be critical for sustaining momentum.

Summary Assessment

LeMaitre Vascular Inc exemplifies a niche-focused medtech player combining a specialized vascular device portfolio with robust direct customer relationships and diversified geographic channels providing resilient growth foundations amidst complex regulatory oversight.

Financially, it has transformed profitability through steady revenue gains paired with operational efficiencies producing substantial earnings growth accompanied by solid free cash flow generation facilitating ongoing dividend funding alongside moderate buybacks attractive to income-focused investors.

Regulatory risks remain foremost among challenges given stringent FDA/EU frameworks potentially imposing costly remediation or recalls—recent voluntary actions demonstrate management responsiveness mitigating exposures.

The near-to-medium term outlook hinges on continued international expansion coupled with pragmatic incremental innovation addressing evolving clinical needs rather than disruptive technology bets.

For investors seeking focused medtech exposure with tangible cash returns underpinned by competitive moats emerging from complex regulatory barriers, LeMaitre offers compelling attributes warranting close monitoring against upcoming regulatory developments or product milestones.

Disclaimer: This analysis is intended for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments