LENSAR's Strategic Reset Following Merger Termination

After the collapse of its merger with Alcon, LENSAR refocuses on core robotic cataract laser technology to drive independent growth.

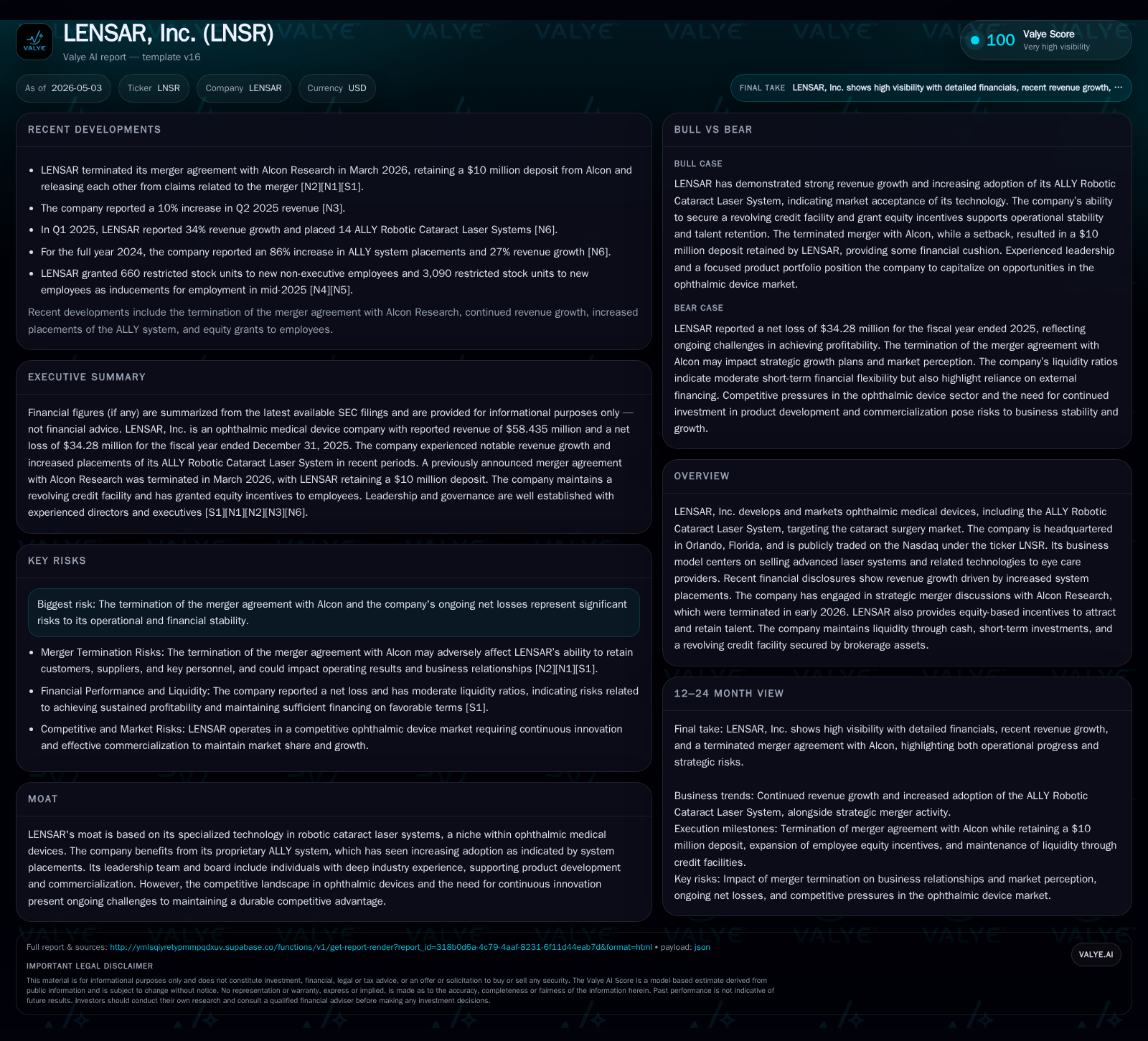

LENSAR, Inc. recently terminated its merger agreement with Alcon Research, marking a significant inflection point in its strategic direction. This development shifts the company's near-term focus toward organic growth through adoption of its ALLY Robotic Cataract Laser System and sustaining innovation in a competitive ophthalmic devices market. While the proprietary technology offers differentiation, ongoing operational losses and post-merger termination costs exert financial strain. Monitoring system placement metrics, regulatory progress, and financial liquidity will be critical to assessing LENSAR's path forward.

The Impact of the Terminated Alcon Merger

On March 16, 2026, LENSAR officially terminated its previously announced merger agreement with Alcon Research, LLC, which had been in place since March 23, 2025 [S11], [S12], [N1]. This strategic deal promised to fold LENSAR into Alcon as a wholly owned subsidiary but was discontinued by mutual agreement. Although LENSAR retained the $10 million deposit made by Alcon under the merger terms, this outcome represents a setback in terms of anticipated operational synergies and shareholder value realization. The termination injects uncertainty about future partnership prospects and temporarily distracts management’s focus due to associated costs and legal contingencies [S5].

This shift forces LENSAR to recalibrate as an independent entity navigating a competitive ophthalmic device market without the scale leverage or distribution benefits that might have flowed from the Alcon platform. Market sentiment likely reflected this pivot adversely in the near term as investors face elevated uncertainty regarding execution risks outside a strategic buyer framework.

The company also disclosed leadership changes shortly after the merger termination announcement: CFO Thomas R. Staab II resigned effective May 2026 to pursue other opportunities, accentuating potential transitional challenges at the financial helm during this critical juncture [S29].

LENSAR’s Core Business Model and Technological Edge

LENSAR generates revenue principally through sales and placements of its ALLY Robotic Cataract Laser System—an advanced ophthalmic medical laser designed for precision enhancement in cataract surgery [S1], Valye excerpt. The business model centers on direct sales of high-tech equipment to eye care providers coupled with related consumables or service arrangements that support ongoing usage.

The ALLY system embodies specialized robotic precision laser technology intended to improve surgical outcomes compared to manual methods by providing digital mapping and customized laser incisions. This innovation supports premium pricing positions relative to legacy systems or more commoditized platforms prevalent in the market.

Customer adoption dynamics are influenced by surgeons’ willingness to invest capital expenditures in new ophthalmic technology balanced against clinical efficacy evidence and workflow integration benefits. Retention is fostered through software innovations and equity incentive programs that maintain engineering talent vital for continuous product improvement [S1], Valye excerpt. Pricing power derives from differentiated capabilities emphasizing safety, accuracy, and procedural customization.

Industry Dynamics and Competitive Positioning

LENSAR operates within a specialized segment of ophthalmic medical devices focused on cataract surgery lasers—a niche characterized by rapid innovation cycles, rigorous regulatory oversight, and entrenched competition from larger players such as Alcon and STAAR Surgical [S1], Valye excerpt. While LENSAR’s ALLY system provides proprietary technological edges, overall industry barriers for sustained moat remain moderate due to evolving standards of care and rapid competitor advancements.

The firm’s relatively smaller scale compared to giants like Alcon limits negotiating leverage with suppliers and distribution channels but allows nimbleness in product iteration. Regulatory hurdles are non-trivial given FDA requirements for medical device safety and performance claims; thus maintaining compliance while accelerating innovation forms a delicate balancing act.

Supply chain pressures common across medtech sectors—such as semiconductor shortages impacting laser components—could constrain capacity utilization temporarily yet have not been explicitly cited as severe for LENSAR at this stage. Adoption curves hinge on convincing surgeons to transition from manual or alternative laser platforms amid cost sensitivity within healthcare provider budgets.

Growth Catalysts and Expansion Opportunities

Despite the merger setback, LENSAR showcases several structural levers for growth:

- System Placements: Recent filings affirm increasing installations of ALLY systems driving revenue growth momentum (approx. $58.4 million total revenue reported for FY 2025) [F1], [S1]. Higher penetration especially among selective cataract surgery centers sustains topline expansion potential.

- Product Development Pipeline: Continuous engineering efforts supported by equity-based incentives secure innovation pipeline strength crucial for responding to competitive technologies.

- Geographic Expansion: Opportunities exist beyond core U.S. markets where cataract prevalence is rising due to aging demographics; regulatory pathways outside FDA also provide scope for international growth.

- Talent Retention: Compensation programs incorporating stock units aim at maintaining key scientific and commercial staff amid an otherwise competitive employment landscape in medtech.

- Strategic Partnerships: Absent the Alcon deal closure, LENSAR may explore alternative alliances or distribution collaborations to broaden reach or enhance complementary offerings [S1].

Concrete KPIs such as installation rates per quarter, backlog bookings for new systems, renewal rates on service contracts, and margin improvements tied to economies of scale will be pivotal markers of progress.

Risks and Operational Challenges Ahead

Key risks shape LENSAR’s near-term outlook:

- Financial Pressure: The company reported operating losses totaling approximately $24.6 million in 2025 alongside net losses near $34.3 million reflecting ongoing investment outlays required for R&D and commercialization efforts [F1]. Sustained cash burn stresses liquidity management without merger-related funding support.

- Post-Termination Costs: Expenses associated with unwinding the merger—legal fees, transaction costs—and disruption impact operating performance per disclosures [S3], [N1].

- Leadership Transition: CFO departure introduces risk around financial planning continuity during arguably one of company’s most fragile phases ([S29]).

- Competitive Intensity: Larger competitors possess deeper resources allowing accelerated product launches or price competition pressures requiring agile innovation from LENSAR.

- Regulatory Risk: Medical device regulatory delays or failure to obtain clearances could stall product launches or limit market acceptance.

- Customer Retention Uncertainty: Loss of partnerships or reduced buyer confidence stemming from merger fallout may impair customer acquisition or renewals.

Taken together these factors underscore execution risk heightened by recent corporate upheaval but mitigated somewhat by underlying product relevance.

Key Milestones and What to Monitor Next

Stakeholders should focus on several imminent developments:

- CFO Replacement & Finance Function Stability: Outcome of search process triggered by April resignation will signal operational steadiness ([S29]).

- Quarterly System Placement Announcements: Tracking install pace will reveal whether growth momentum endures independently.

- Regulatory Approvals / New Product Launches: Milestones here could validate development trajectory enhancing competitive stance ([S1]).

- Liquidity Updates & Financing Events: Any refinancing moves or equity raises needed to extend runway warrant close attention given net loss backdrop ([F1]).

- Strategic Partnership Announcements: Signals of collaborations linked to commercialization leverage will be meaningful post-merger exit ()

- Operational Cost Management: Efforts to contain post-termination expenses impacting profitability should be disclosed periodically ([S3]).

These data points will collectively inform if LENSAR can sustain its independence while building off core robotic laser innovation.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $13mm | |

| 2025-12-31 | ||

| Current assets | $47mm | |

| 2025-12-31 | ||

| Current liabilities | $41mm | |

| 2025-12-31 | ||

| Current ratio | 1.15x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Revenue | $58.44M | |

| 2025-12-31 | ||

| Operating Income | -$24.58M | |

| 2025-12-31 | ||

| Net Income | -$34.28M | |

| 2025-12-31 | ||

| Cash & Equivalents | $12.97M | |

| 2025-12-31 | ||

| Current Ratio | 1.15 | |

| 2025-12-31 |

Financials reveal robust revenue generation associated with growing system placements but persistent operating deficits reflective of R&D investment intensity typical of medtech innovators [F1]. It does not constitute investment advice.*

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments