SPAC Dynamics and Everli Merger Shape Melar Acquisition’s Next Chapter

Melar Acquisition Corp. I is advancing its business combination with Everli Global Inc., navigating liquidity pressures and deal milestones critical to executing on its SPAC strategy.

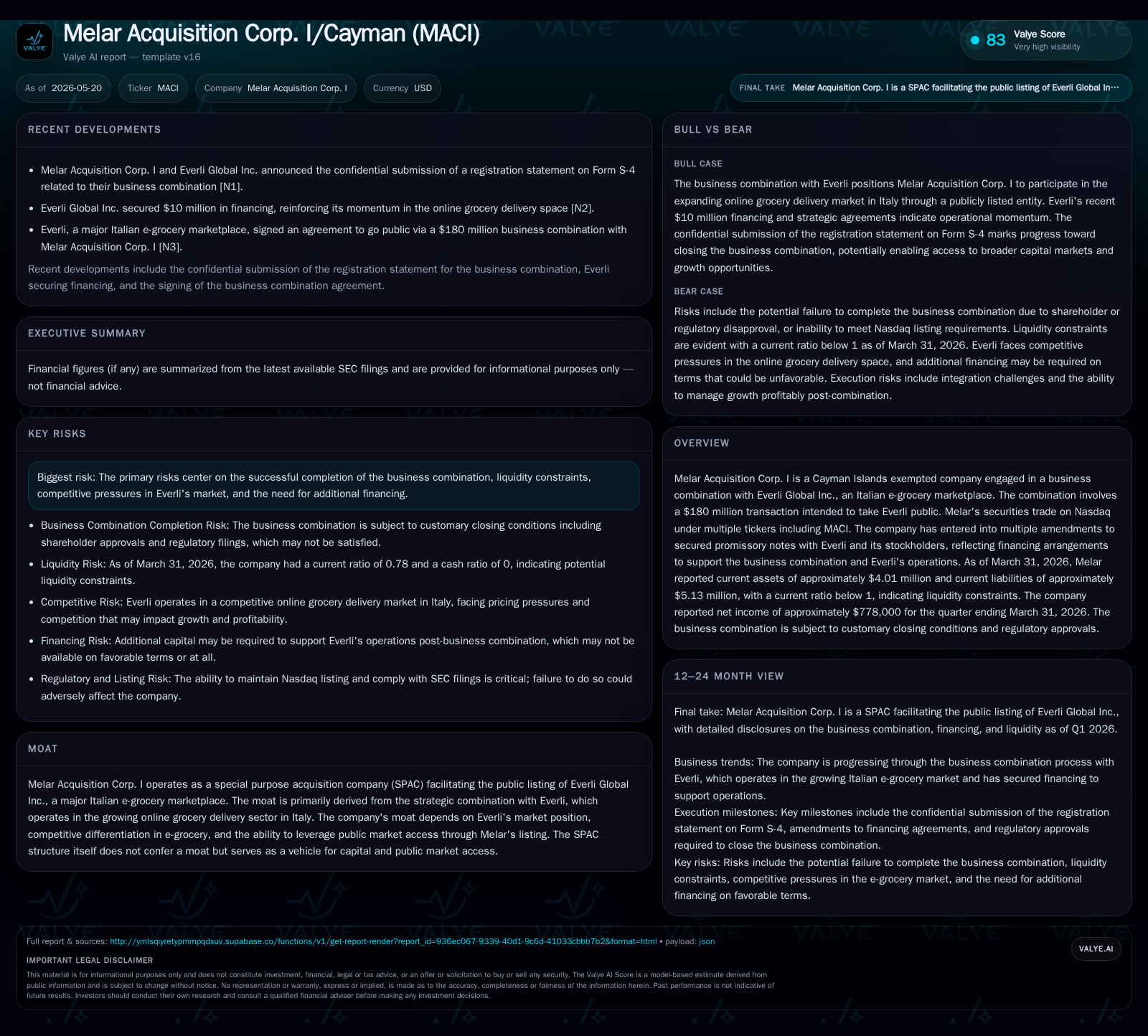

The latest quarterly filing dated May 14, 2026, highlights a tight liquidity profile for Melar Acquisition Corp. I as it approaches the June 20 deadline to close its business combination with Everli Global Inc., an Italian e-grocery marketplace. The SPAC structure positions Melar as a financial vehicle enabling Everli's public market access, contingent on final regulatory approvals and financing arrangements including multiple amendments to secured promissory notes supporting the transaction. The merger taps into growth opportunities in Italy’s expanding digital grocery sector but carries notable execution and financing risks given the sub-1 current ratio and competitive SPAC landscape.

Recent Quarterly Update Highlights Combination Deadline and Liquidity Constraints

Melar Acquisition Corp. I’s latest Form 10-Q filing dated May 14, 2026 ([S2]) portrays a sharpened view of immediate operational realities as the company approaches the June 20, 2026 deadline to consummate its business combination with Everli Global Inc. As of March 31, 2026, Melar reported $4.01 million in current assets against $5.13 million in current liabilities, resulting in a current ratio of about 0.78—a clear signal of liquidity pressure that could constrain near-term operational flexibility without additional funding or deal closure [F1]. Despite this tight position, Melar covered the quarter with positive net income near $778,000, indicating controlled operating costs amidst a phase focused primarily on merger execution rather than standalone revenues [S2].

The proximity of the business combination deadline introduces urgency for completing remaining conditions precedent. Failure to close by June risks forced liquidation and redemption scenarios customary to SPAC legal structures ([S1]). This places strong emphasis on effective capital management and securing shareholder support.

Business Model Overview: Melar as a SPAC Vehicle for Everli’s Public Market Entry

Melar Acquisition operates as a special purpose acquisition company (SPAC), essentially a blank check entity formed in Cayman Islands with no operating revenue history pre-combination ([S1]). The core business model revolves around raising capital via an initial public offering—here $160 million gross proceeds were raised—and deploying these funds through a targeted merger to bring a private company public; in this case, Italian e-grocery platform Everli Global Inc [S1].

Revenue generation is deferred until after successful consummation of the business combination when Melar’s securities effectively represent ownership in Everli post-merger. Before combination closure, Melar’s income statement largely reflects operational expenses tied to administrative functions and financing costs rather than commercial revenues.

Sponsor-led governance underlies this process with leadership experienced in emerging finance markets providing strategic direction ([S1]). The SPAC structure confers value primarily through access to public equity markets for private companies like Everli seeking growth capital and liquidity options.

Understanding Everli’s Position Within Italy’s Growing E-Grocery Sector

Everli Global operates an Italian online grocery marketplace that matches consumers with home delivery services through partner supermarkets (,[S1],[S3]). The Italian e-grocery market benefits from secular growth trends driven by rising digital adoption among consumers and demand for convenient delivery solutions.

The platform’s value proposition stems from expansive supermarket network integration across major urban centers enabling broad customer reach and frequency. Market dynamics favor scale and technological sophistication in logistics, inventory management, and user engagement tools—areas where Everli has established footholds.

While specific competitive metrics are not cited herein, industry context suggests that platform differentiation via service coverage area depth and proprietary technology can create customer stickiness important for retention amid fragmented competition.

Financing Structure: Amendments to Promissory Notes Supporting Combination Progress

Recent SEC filings reveal multiple amendments to secured promissory notes between Melar Acquisition Corp., Everli stakeholders, and third-party lenders designed to bridge liquidity gaps during final transaction phases ([S3],). These credit agreements provide operational funding pre-transaction close while underpinning shareholder obligations.

Such arrangements are typical for SPAC mergers involving high-growth businesses that have not yet achieved sustained positive cash flows but require interim capital infusion. The ongoing restructuring and negotiation of these promissory notes reflect dynamic financing needs reflective of evolving deal terms.

Competitive and Regulatory Landscape in Emerging Finance and E-Grocery Markets

The strategic focus on merging with a fintech-linked consumer services company positions Melar within two competitive ecosystems: SPAC sponsor activity in capital markets and the rapidly evolving European digital grocery delivery industry ([S1],).

Competition among SPACs heightens risk over target scarcity and deal pricing pressure as more blank check companies vie for attractive targets—possibly inflating valuations or complicating negotiations ([S1]). Regulatory scrutiny over SPAC structures also continues adapting globally, adding compliance layers.

Within the e-grocery segment, regulation combines consumer protection laws, labor regulations relevant to delivery personnel logistics operations, and data privacy measures related to customer information as applicable across Italy and EU jurisdictions. Managing these alongside scalable technology deployment forms part of inherent constraints in growth.

Key Growth Drivers: Market Penetration, Public Access, and Operational Synergies

Post-merger growth will be driven by leveraging public market capital raised via Melar’s Nasdaq listing providing financial strength for geographical expansion across Italy’s grocery retail segments (,[S1]).

Everli’s platform aims to deepen penetration into digitally engaged consumers who increasingly seek omnichannel fulfillment options including same-day or scheduled deliveries.

Operational synergies may also emerge from combined expertise within Melar's sponsor group versed in fintech innovations potentially assisting backend payment systems or credit offerings integrated into Everli's ecosystem.

Public listing status could enhance visibility lending credibility needed for partnership expansions with major retailers or technology vendors essential for sustaining competitive advantage.

Risks and Constraints: Liquidity Challenges, Deal Execution Risks, and Market Competition

Chief risks highlighted include Melar's limited liquidity evidenced by a sub-1 current ratio at quarter-end posing financial strain if merger delays persist or further funding sources fail ([F1],[S2],).

Execution risk linked to meeting all closing conditions by June deadline remains material; failure would trigger mandatory liquidation impacting shareholders negatively ([S1],[S2]).

Competitive pressure derives both from rival SPAC bids on scarce targets inflating merger premiums as well as from established e-grocery operators intensifying battle for consumer mindshare post-merger ([S1]). Additionally, regulatory changes affecting financing mechanisms or operational practices impose uncertainty on cost structures.

What Investors Should Monitor Next: Closing Conditions, Financing Execution, and Shareholder Approvals

Stakeholders should closely track developments related to final merger closing steps including:

- Timely satisfaction of all transaction conditions by June 20 deadline ([S2])

- Completion of related financing arrangements evidenced by promissory note amendments finalized ([S3])

- Results from potential shareholder voting or redemption outcomes impacting deal viability ([S2])

- Regulatory filings progression including SEC approval of proxy materials ahead of votes ([S3]) These milestones will collectively determine whether Melar successfully transitions from SPAC shell into a publicly-listed operating entity centered around Everli.

Financial Snapshot: Current Assets, Liabilities, and Recent Net Income Insights

As per companyfacts data at March 31, 2026 [F1], Melar's balance sheet displays:

- Current assets: $4.01 million

- Current liabilities: $5.13 million

- Current ratio: roughly 0.78 indicating short-term liquidity challenges While limited revenues pre-close make operating income less meaningful for standalone valuation—the recently reported positive net income near $778k [S2] partially offsets concerns regarding administrative expense control during this pivotal period.

This financial profile underscores that while Melar successfully supports transaction activity thus far structurally through credit amendments ([S3]), it faces critical pressures requiring close management attention until business combination completion unlocks broader operational scale benefits.

Financial position in context

Current assets of $4mm and current liabilities of $5mm imply a current ratio near 0.78x for 2026-03-31 [F1]

Disclaimer: This Valye News analysis is based solely on available SEC filings dated through May 14, 2026, associated companyfacts data at March 31 fiscal snapshot date, and related documents provided. It does not constitute investment advice or research views.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments