Medline Inc.'s Integrated Supply Chain Fuels Scale but Leverage and Regulatory Risks Loom

Medline's vertically integrated model drives extensive product and distribution scale, with long-term Prime Vendor contracts underpinning growth amid competitive and regulatory risks.

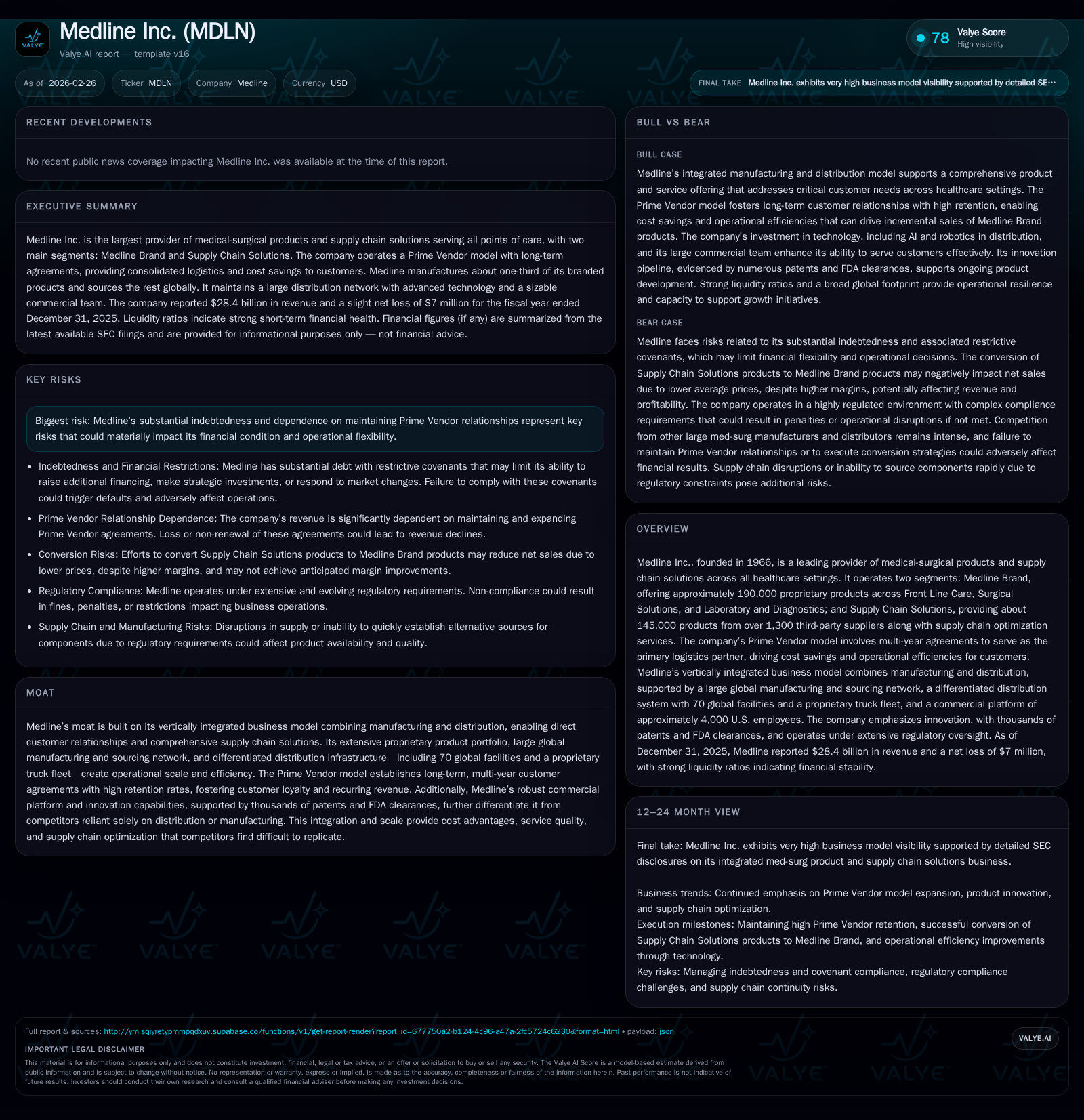

Medline Inc. stands as the largest provider of medical-surgical products by combining a comprehensive portfolio of proprietary and third-party offerings with a highly differentiated supply chain network. Its Prime Vendor model locks in multi-year customer relationships that yield high retention and enable scale efficiencies. While revenue topped $28 billion in 2025 with strong operating income, net income was neutral due to non-operating pressures and the company carries substantial debt that could restrict flexibility. Regulatory scrutiny, especially around healthcare compliance and environmental controls, alongside ongoing competitive pricing pressure, represent significant challenges moving forward. Future growth hinges on converting third-party sales to Medline Brand products and expanding Prime Vendor contracts, balanced against margin pressures and potential litigation or compliance costs.

Company Overview and Historical Performance

Founded in 1966, Medline Inc. has evolved into the largest provider of medical-surgical products globally based on total net sales. The company serves a broad spectrum of healthcare settings—from acute hospitals to outpatient clinics and post-acute care facilities—offering an extensive portfolio exceeding 335,000 med-surg products.

Financially, the company's latest full-year results for 2025 reveal top-line revenues of approximately $28.4 billion supported by robust operational efficiency delivering operating income of $2.2 billion [F1]. However, net income registered a marginal loss at $7 million for the year, influenced likely by interest expenses related to significant debt loads or other non-operating factors not detailed within the provided data [F1]. This points toward strong core business profitability offset by financing or exceptional items.

The company maintains sound liquidity with a current ratio above 4.2x (current assets $10.7B vs current liabilities $2.49B) and positive free cash flow nearing $1.3 billion after capital expenditures [F1]. This cash generation capacity supports investment in infrastructure while servicing substantial leverage.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Cash flow from operations approximates $2.0 billion with capital expenditures near $700 million as per available data; dividends and buybacks are not disclosed explicitly.

Business Segments and Moat Characteristics

Medline operates two principal segments:

Medline Brand: Includes about 190,000 proprietary med-surg products across Front Line Care (patient-facing consumables like gloves and wound care), Surgical Solutions (kits, gowns, orthopedic implants), and Laboratory & Diagnostics (testing kits, analyzers). It holds leading market positions across many key product lines supported by internal R&D and quality assurance teams ensuring rigorous standards [S1,S27].

Supply Chain Solutions: Distributes approximately 145,000 med-surg products sourced from over 1,300 third-party suppliers including national brand leaders. This segment complements the proprietary portfolio while providing supply chain optimization services such as consulting, warehouse management, and logistics technology deployment [S1,S27].

At the core lies Medline’s Prime Vendor model, structured primarily through multi-year agreements averaging five years that designate Medline as a consolidated logistics provider for customers’ med-surg procurement needs [S5]. This model effectively replaces fragmented supplier bases with one comprehensive partner enabling operational efficiencies.

This integration—from product manufacturing through proprietary distribution using over 70 global facilities including significant operations in the US supported by AI/robotics automation—delivers next-day service to 95% of US customers via its MedTrans trucking fleet exceeding 2,100 vehicles [S5]. Such vertical integration forms a competitive moat centered on:

- Cost advantages from lower unit manufacturing costs combined with economies in distribution

- High customer retention (>98% averaged over five years in Prime Vendor contracts)

- Scale benefits enabling consistent price competitiveness relative to peers relying solely on distribution or third-party supply

- Innovation depth protected by thousands of patents contributing to differentiated product quality

Past Growth Drivers

Medline’s revenue growth historically has been powered by expanding Prime Vendor relationships which drive incremental purchases of higher-margin Medline Brand products over lower-margin third-party equivalents within Supply Chain Solutions [S5,S6]. This conversion strategy improves gross profit margins though may compress reported sales near term due to lower pricing on proprietary goods [S6].

Operationally efficient logistics networks enabled better fill rates and service quality shielding clients from supply disruptions—a critical value add during recent industry-wide constraints post-pandemic.

Prospects for Future Growth

Looking ahead, growth opportunities stem chiefly from:

- Increased penetration in existing accounts: By converting Supply Chain Solutions purchases to Medline Brands via Prime Vendor agreements—although this entails managing near-term sales dips balanced against improved gross margins [N1,S6].

- New Prime Vendor contracts: Targeting large health systems seeking consolidated sourcing arrangements that can yield shared cost savings.

- Expansion into non-acute care channels: Where customization needs allow tailored product portfolios with focused offerings driving stickiness [N1,S5].

- Enhancements in digital supply chain solutions: Leveraging AI-enabled warehousing efficiencies could further optimize costs.

Constraints include intense competition driving margin compression; buyer consolidation increasing negotiating leverage; reimbursement changes affecting hospital procurement budgets; and regulatory compliance demands imposing operational costs or limiting market access .

Company Guidance and Milestones to Watch

While explicit financial guidance was not disclosed within public sources provided ([N#],[S#]), key milestones to monitor include:

- Updates on Q4 earnings validation around Prime Vendor expansion impact as noted in recent analyst commentary [N1]

- Success metrics regarding product conversion rates from third-party brands to Medline Brands within existing contracts ([N1])

- Management commentary on capital deployment priorities addressing leverage reduction versus reinvestment in automation or manufacturing capacity expansion ([S11])

- Any regulatory developments impacting core product approvals or logistics operations such as EtO sterilization compliance costs ([S8])

Capital Allocation and Returns Considerations

The available reported metrics suggest strong cash flow generation with free cash flow near $1.3 billion in 2025 after investments supporting operational needs despite substantial debt levels evidenced in liquidity disclosures [F1,S11,S15]. Dividend payments or share repurchase programs were not explicitly mentioned.

Reported return on equity is approximately zero (-0.1%), aligning with the negligible net income result for the year despite solid operating profits reflecting financing costs or one-off charges that weigh on returns overall [F1]. The company’s leverage constraints under senior secured credit agreements impose restrictive covenants limiting strategic flexibility including dividend payments or asset sales to service debt obligations [S11,S15]. This suggests capital allocation decisions will emphasize debt servicing prudence alongside growth investments.

Risks Overview

Medline faces several notable risks broadly grouped into:

- Indebtedness Risk: The firm's high leverage restricts financial agility making it vulnerable to economic downturns or refinancing challenges. Credit agreements also limit dividends/distributions which may affect shareholder returns or funding for innovation projects [S11,S15].

- Regulatory Compliance: Complex regulatory frameworks govern product safety (FDA), healthcare reimbursement integrity (AKS/FCA), environmental controls specifically around sterilization processes using EtO gas which have seen tightening oversight resulting in significant capital expenditure needs ([S8],[S14]). Data privacy laws add further compliance burdens given involvement with protected health information ([S13]).

- Competitive Pressure: Marketwide buyer consolidation leads to increased negotiation power among large hospital systems reducing pricing power. Emergence of e-commerce platforms challenges traditional supply relationships requiring ongoing digital transformation investments ().

- Legal Exposure: Ongoing litigation relating to environmental matters as well as government audits around prior durable medical equipment business raise potential future liabilities despite recent favorable litigation gains recognized ([S7],[S14]).

- Supply Chain Complexity: Global sourcing exposes the firm to geopolitical risks including tariffs, currency fluctuations, human rights adherence requirements in overseas factories as well as freight logistics disruption risks impacting customer service levels ([S1]).

Conclusion

Medline’s vertically integrated business combining proprietary manufacturing with an extensive distribution footprint underpins its leadership position in the med-surg space through operational scale advantages reinforced by its entrenched Prime Vendor partnerships driving cost-efficiency for large healthcare providers.

Its sizeable revenue base surpassing $28 billion alongside strong operating profitability demonstrates the commercial viability of its integrated approach despite muted bottom-line results pressured by non-operating factors.

Looking forward, sustainable growth will rely heavily on deepening penetrations via Medline Brand conversions within existing contracts while carefully navigating an environment marked by regulatory scrutiny, intense pricing competition, industry consolidation among buyers, evolving reimbursement dynamics, and elevated indebtedness requiring prudent capital stewardship.

Monitoring quarterly earnings disclosures will be essential to gauge progress against these strategic vectors along with regulatory developments tied to safety compliance costs and legal contingencies.

This report is intended solely for informational purposes based on publicly available filings and sources cited herein as of February 26, 2026. It does not constitute investment advice or a recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments