Minerva Gold’s Bid to Diversify Amid Persistent Liquidity Challenges

Minerva Gold's latest quarterly filing reveals early revenue from design services overshadowed by critical liquidity constraints and looming capital needs.

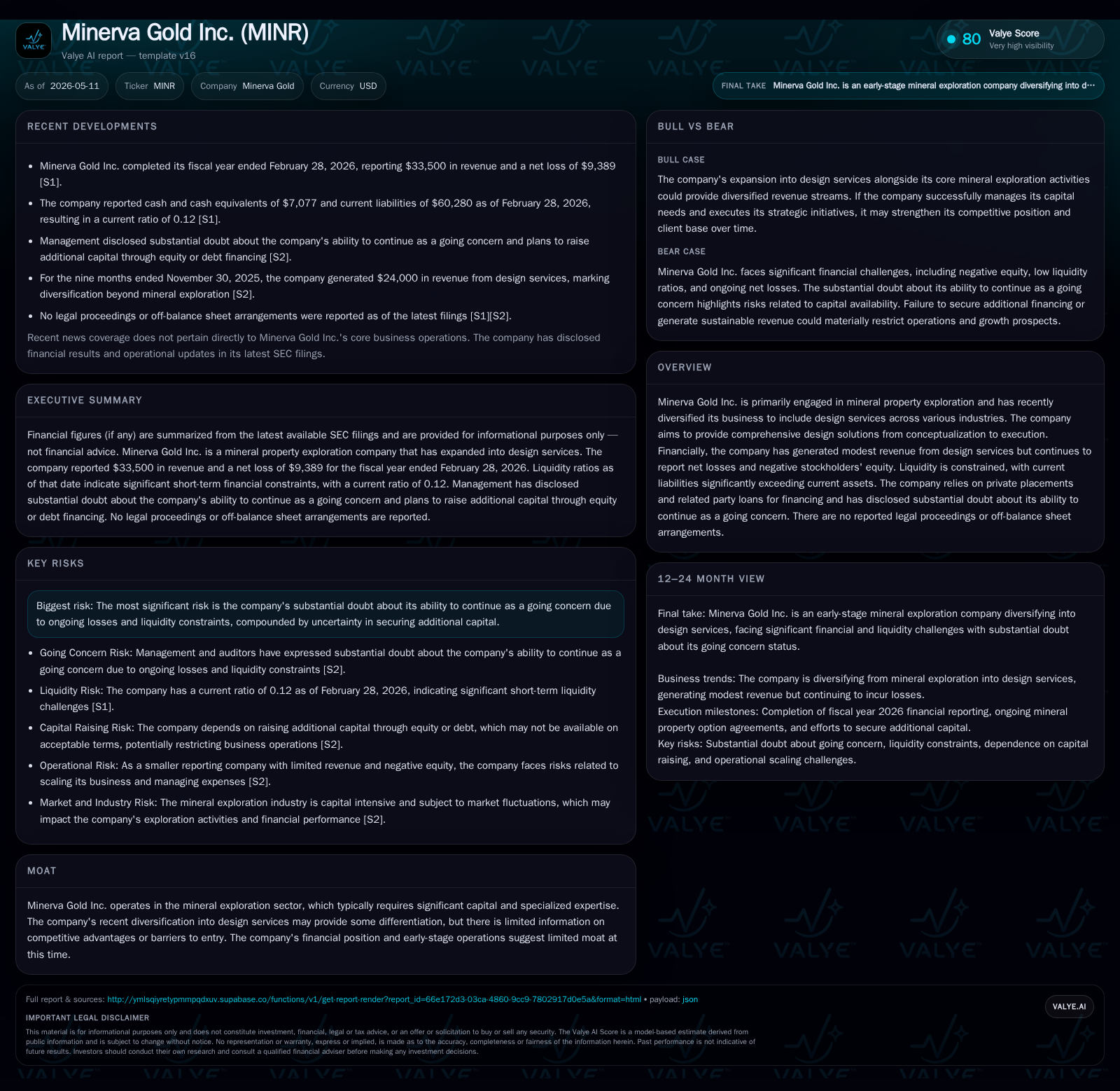

In its 2026 Q3 filing, Minerva Gold Inc. reported its first revenues of $24,000 from new design services, reflecting a strategic diversification beyond mineral exploration. However, the company's financial health remains precarious, with a current ratio of 0.12 and negative shareholders’ equity underscoring severe working capital deficiencies. Management plans further capital raises to sustain operations but warns of dilution risks and uncertain financing availability. The company’s path to growth hinges on executing its diversification while overcoming substantial cash flow and funding challenges.

Latest Operating Update: Revenue Gains Shadowed by Capital Concerns

The latest quarterly disclosure filed January 20, 2026 [S2] presents Minerva Gold at a critical juncture of fledgling commercial expansion coexisting with acute financial strain. The company recorded $24,000 in revenue from its newly integrated design services over the first nine months of fiscal 2025. This marks a tangible but modest step toward generating cash flows beyond its core mineral exploration activities which have yet to produce revenue.

However, this nascent growth contrasts sharply with the company's deepening loss profile. For the comparable nine-month period ended November 30, 2025, expenses totaled nearly $38,000 against the modest income stream leading to a net loss of $13,945 [S2]. The financial statements continue to be prepared under going concern assumptions during explicit auditor warnings about viability risks [S2].

Balance sheet metrics illustrate heightened distress: as of February 28, 2026, Minerva held only $7,077 in cash and equivalents while current liabilities stood at $60,280—yielding a perilously low current ratio of approximately 0.12 [F1]. Negative stockholders’ equity exceeds $50 million as per the latest figures indicative of accumulated operational losses far outstripping invested capital [S2], [F1].

Operating liquidity has thus been sustained primarily through related party loans and private placements rather than operating-generated cash flow or external credit facilities—which do not exist [S2]. Management acknowledges an imperative need for further capital raises involving equity or convertible debt issuances which carry dilution and subordinated security risk for existing shareholders.

Business Model and Service Portfolio: Mineral Exploration Meets Design Services

Minerva Gold was incorporated in Nevada in early 2021 focused predominantly on mineral property exploration primarily targeting assets in Kazakhstan [S1]. This upstream segment is intrinsically capital-intensive with prolonged lead times before monetization stemming from exploration permits acquisition through development.

Recognizing these challenges, Minerva embarked on a strategic pivot that integrates design services across various industries into their portfolio [S1], [S2]. This new segment pledges comprehensive end-to-end creative solutions from conceptualization through execution aimed at delivering high-quality outcomes intended to diversify revenue streams away from mineral exploration’s structural cyclicality and capital demands.

This dual model blends the speculative nature of mineral prospecting — reliant on securing exploration rights and eventual resource monetization — with service-based offerings that can generate incremental recurring revenues dependent on client acquisition and retention dynamics. However, the design services business remains nascent with initial revenues totaling just $24k over nine months indicating early-stage commercialization subject to scalability constraints [S2].

Operational synergies or cross-selling opportunities between these disparate lines remain unclear given minimal disclosed scale or client base overlap.

Competitive Context and Industry Positioning: Opportunities and Barriers

Within mineral exploration, barriers to entry stem largely from high upfront capital requirements, regulatory approvals for mining rights, geological expertise needs, and long resource development cycles. However well entrenched incumbents enjoy advantages around geological data access and financing relationships.

Minerva presently holds no disclosed competitive moat as a small explorer still without proven resource assets or diversified funding sources. Exploration rights were lost when prior option agreements lapsed due to unmet financial obligations pointing to execution challenges [S18].

Design services markets are typically fragmented with many small agencies offering tailored solutions but comparatively low switching costs for clients who can move among providers flexibly. Minerva’s value proposition hinges on integrated end-to-end service delivery potentially distinguishing it if scale permits but this advantage remains speculative given minimal early revenues [S1], valye_report_excerpt.

Dual-focus operations may complicate resource allocation choices amid finite capital—both segments compete for funding while each demands distinct competencies: geology/development versus creative service delivery.

Growth Drivers: Diversification Potential Against Financial Constraints

Key growth drivers include expanding adoption of design services evidenced by initial contract wins delivering $24k revenue in nine months—a base to build upon subject to effective marketing and operational scaling [S2].

On mineral exploration frontiers, opportunities hinge on re-entering reserve acquisition avenues or forming partnerships potentially unlocking value but contingent on reliable financing commitments.

Recent filings reveal intent to acquire Taizhou Sentian Sanitary Ware Co., Ltd., signaling diversification beyond existing verticals into manufacturing adjacent markets through an April 2026 letter of intent aiming for a May closing [S3], which could materially reshape scale and revenue profiles if consummated.

Yet all growth trajectories are contingent upon timely raising substantial additional capital as working capital needs rise alongside planned expansions in inventory acquisitions, start-up developmental costs, and marketing expenses required to grow both design offerings and broader business lines [S2].

Risks and Limitations: Going Concern Uncertainty and Capital Dependency

Outstanding risks loom large with explicit disclosure of substantial doubt surrounding continuity as a going concern due to ongoing losses compounded by excessive current liabilities relative to assets [S2], [S9], valye_report_excerpt.

No bank lines of credit exist; operations depend entirely on intermittent private equity/debt placements or related party advances exposing vulnerability to market condition shifts or investor appetite decline.

Future financings will likely dilute existing shareholders given anticipations that new securities may have senior rights/preference above common stock holders undermining shareholder value [S2]. Failure to secure funding on acceptable terms may force curtailment or cessation undermining business prospects.

Additionally, strategic pivots into unfamiliar industries such as manufacturing heighten exposure to integration execution risks while ongoing losses erode financial flexibility creating mounting operational pressure.

What To Watch Next: Liquidity Milestones and Strategic Execution

Market participants should closely monitor completion status and impact from acquiring Taizhou Sentian pitched for late May 2026 closing which could diversify revenues materially if executed effectively [S3].

Further quarterly submissions will be critical reporting whether design service revenues accelerate beyond preliminary levels providing meaningful contribution towards reducing net losses.

In sum, upcoming performance indicators such as backlog growth in design services contracts or improved cash position will offer tangible insights into operational execution amidst persistent liquidity constraints.

Financial Snapshot: Current Liquidity, Leverage, and Capital Needs

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $7077 | |

| 2026-02-28 | ||

| Current assets | $7491 | |

| 2026-02-28 | ||

| Current liabilities | $60280 | |

| 2026-02-28 | ||

| Current ratio | 0.12x | |

| 2026-02-28 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) |

|---|---|

| Revenue (Trailing) | 33,500 |

| Net Income (Trailing) | -9,389 |

| Cash & Equivalents | 7,077 |

| Current Ratio | 0.12 |

As evidenced at February 28 year-end data drawn from companyfacts repository [F1], liquidity metrics starkly illustrate the severity of Minerva Gold’s near-term financial challenges despite incremental top-line progress. Cash suffices to cover barely over one tenth of current liabilities reinforcing reliance on fresh capital inflows.[S2]

This analysis is based solely on publicly available SEC filings as referenced above. It does not constitute investment advice or an endorsement of Minerva Gold Inc.’s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments