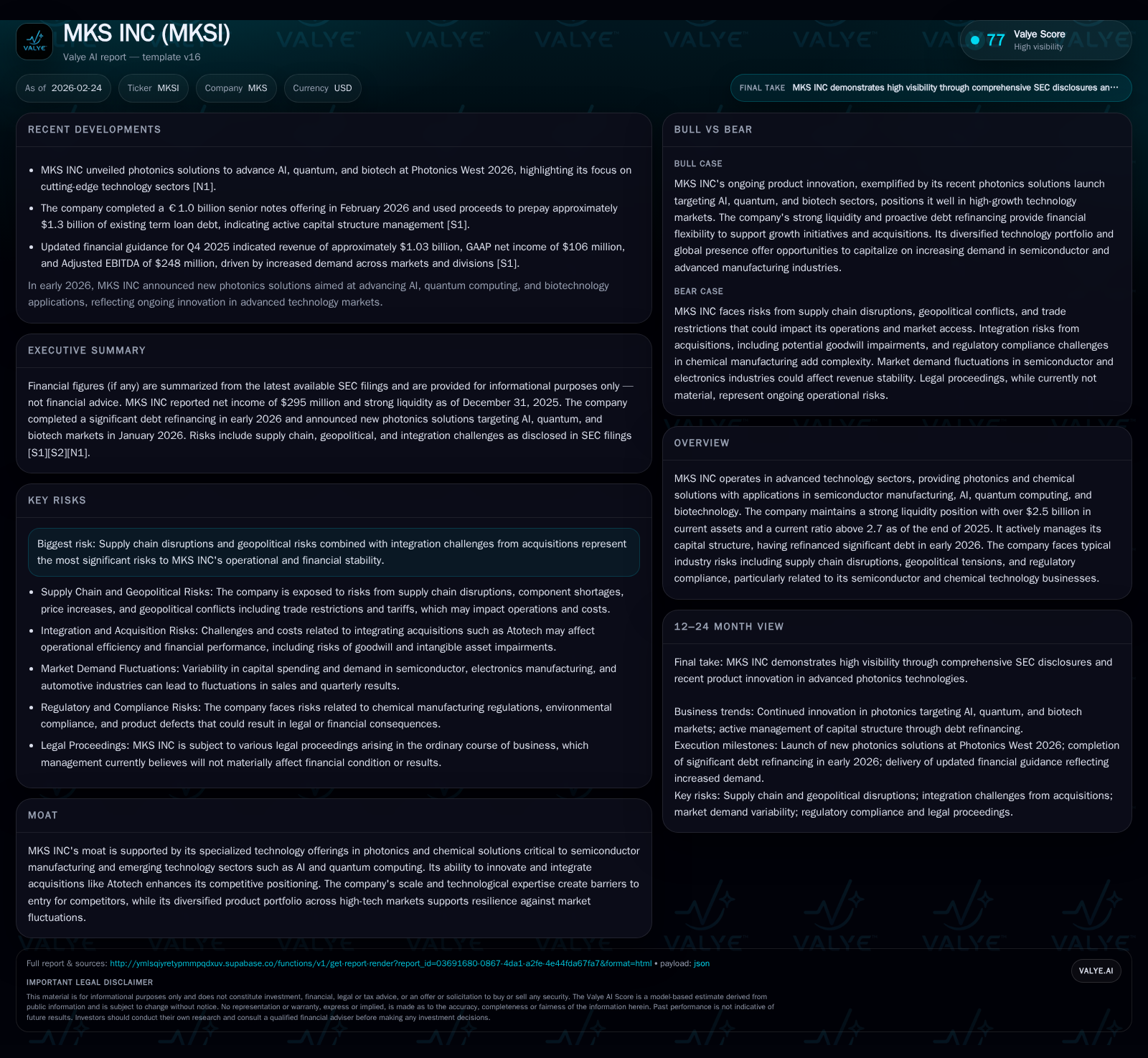

MKS Inc Strengthens Technological Moat and Capital Structure After Challenging Loss

The company rebounded from a large loss in FY2023 to profitability in FY2025, leveraging photonics leadership and a refined debt profile.

After enduring a significant operating loss in FY2023, MKS Inc achieved a marked financial turnaround by FY2025, returning to solid operating income and net profits. This recovery reflects operational improvements across its photonics and chemical segments along with strategic integration of acquisitions such as Atotech. Additionally, MKS executed a comprehensive refinancing of its term loan facilities in early 2026, extending maturities and reducing borrowing costs, bolstering liquidity and capital flexibility. Going forward, semiconductor fab demand variability and supply chain risks remain key factors to monitor.

From Significant Loss to Solid Operating Income: MKS Inc’s Recent Financial Trajectory

MKS Inc encountered a pronounced earnings turbulence in FY2023, recording an operating loss of approximately -$1.55 billion followed by a net loss of roughly -$1.84 billion [F1]. This severe downturn contrasted sharply with prior years where operating income hovered above half a billion dollars ($617 million in FY2022). The primary drivers behind the FY2023 setback are not explicitly detailed but align with semiconductor sector cyclicality and acquisition-related costs.

However, the fiscal narrative reversed strongly over the next two years. By FY2024, operating income rebounded to nearly $498 million and climbed further to $528 million by end-2025 – representing a steady 6% year-over-year increase despite ongoing macroeconomic headwinds [F1]. Net income surged from $190 million in FY2024 to an impressive $295 million in FY2025 – a notable +55.3% growth YoY [F1]. The recovery hinged on improved operational execution across core technology segments alongside cost management initiatives.

Operating cash flows demonstrated resilience throughout this period despite volatile earnings. From $319 million CFO in the trough year of 2023, cash flow expanded considerably reaching $645 million by 2025 – a +22.2% annual increase reflecting superior working capital management and enhanced product mix capturing higher-margin demand from the semiconductor ecosystem [F1]. Capital expenditure showed a measured upward trajectory consistent with growth ambitions: rising from $87 million capex spend in 2023 to $148 million in 2025 (+25.4%) complementing investments into fabrication tooling capabilities essential for sustaining client fabs’ CMP process upgrades [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 295 | 645 | 528 | 148 | +55.3% |

| 2024 | 190 | 528 | 498 | 118 | +110.3% |

| 2023 | -1841 | 319 | -1554 | 87 | -652.9% |

| 2022 | 333 | 529 | 617 | 164 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 497 | 10.8 |

| 2024 | 410 | 8.2 |

| 2023 | 232 | -74.5 |

| 2022 | 365 | 7.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not available from provided tags.

Core Drivers Supporting Growth: Photonics, Chemicals, and Strategic Acquisitions

MKS Inc’s technological moat is anchored in its photonics solutions combined with semiconductor-grade chemical processing equipment vital for fabrication lines. The August 2022 acquisition of Atotech expanded its footprint into chemical formulations used for plating and surface finishing — critical for semiconductors as well as emerging AI hardware platforms, quantum computing components, and biotech device manufacturing [N2]. This broadened product diversity while fortifying recurring revenue streams within high barrier-to-entry CMP consumables markets.

This diverse portfolio provides resilience amid sector volatility while maintaining technological leadership through intensive R&D supporting sub-10nm geometry nodes.

Industry Challenges: Supply Chain Disruptions and Regulatory Risks

MKS faces risks from reliance on limited or sole-source suppliers for critical components heightening vulnerability during global supply chain disruptions [S7][S9]. Geopolitical tensions notably U.S.-China trade frictions impose export controls affecting shipment of sensitive photonics parts or chemicals that may be dual-use technologies [S4][N2]. Tariffs and retaliatory actions also pressure cost structures.

Environmental regulations related to chemical manufacturing introduced via Atotech raise compliance liabilities particularly around waste management under EPA guidelines [S8]. These factors combine with inherent semiconductor capital spending cyclicality contributing to earnings variability.

Capital Structure Refinement: Debt Refinancing and Enhanced Liquidity

In February 2026, MKS completed significant refinancing activities including amendments to credit agreements and issuance of €1 billion senior unsecured notes due in 2034 [S5][S6][S10]. The refinancing replaced the prior $2.2 billion USD Tranche B Term Loan with a new lower principal tranche of approximately $914 million, alongside renewed euro-denominated Term Loans extending maturities significantly.

Interest margins decreased notably (e.g., SOFR-based margins reduced from ~2% to ~1.75%), optimizing borrowing costs aligned with market conditions [S6]. The revolving credit facility was upsized from $675 million to $1 billion with extended maturities enhancing short-term liquidity flexibility supporting working capital needs amid fab expansions [S5]. These moves deleveraged principal balances while maintaining leverage neutrality per company disclosures.

Cash Flow Strength and Capital Allocation Strategy

Robust cash flow generation is evident with CFO reaching nearly $645 million in FY2025 against controlled capex spending of $148 million yielding approximately $497 million free cash flow [F1]. This financial discipline supports internal funding for growth initiatives or opportunistic debt reduction.

Share repurchases were modest at about $45 million during FY2025 while dividends have not been paid recently signaling management preference for reinvestment over direct shareholder distributions currently [F1]. Equity capital remains strong at nearly $2.72 billion resulting in an indicative return on equity near 10.8%, reflecting efficient use of shareholder funds post-restructuring impacts [F1].

Forward Outlook: Monitoring Semiconductor Demand Cycles and Supply Chains

Going forward, semiconductor fab capital expenditure trends remain cyclical but increasingly influenced by AI-driven demand surges boosting orders for photonics-enabled tooling platforms crucial for advanced node implementations [N2][N5][S26].

Investors should watch backlog levels reported during earnings calls as leading indicators alongside customer investment plans tied specifically to CMP consumables — critical given recurring revenue nature directly impacting Atotech's business.

Supply chain normalization pace post-global disruptions will be key to margin expansion potential given past reliance on constrained raw material sources requiring strategic supplier diversification efforts.

Integration Risks and Geographic Diversification Mitigate Exposure

Post-acquisition integration of Atotech presents typical challenges including aligning global operations while maintaining innovation momentum [S8][N2]. Geographic diversification across U.S., China, and Europe reduces concentration risk amid geopolitical tensions enabling smoother operational continuity despite trade policy uncertainties.

Successful post-merger integration remains critical to realizing synergies without excessive disruption or unforeseen liabilities affecting earnings stability.

Disclaimer: This analysis relies exclusively on publicly available SEC filings ([F1], [S#]) and recent earnings call transcripts ([N#]). It does not constitute investment advice but offers an informed assessment based strictly on documented financial results and disclosed corporate actions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments