Medical Properties Trust Reports Q1 Miss Amid Tenant Challenges

MPT’s recent quarterly results reveal earnings pressure tied to tenant financial difficulties, underscoring inherent risks in its specialized healthcare real estate portfolio.

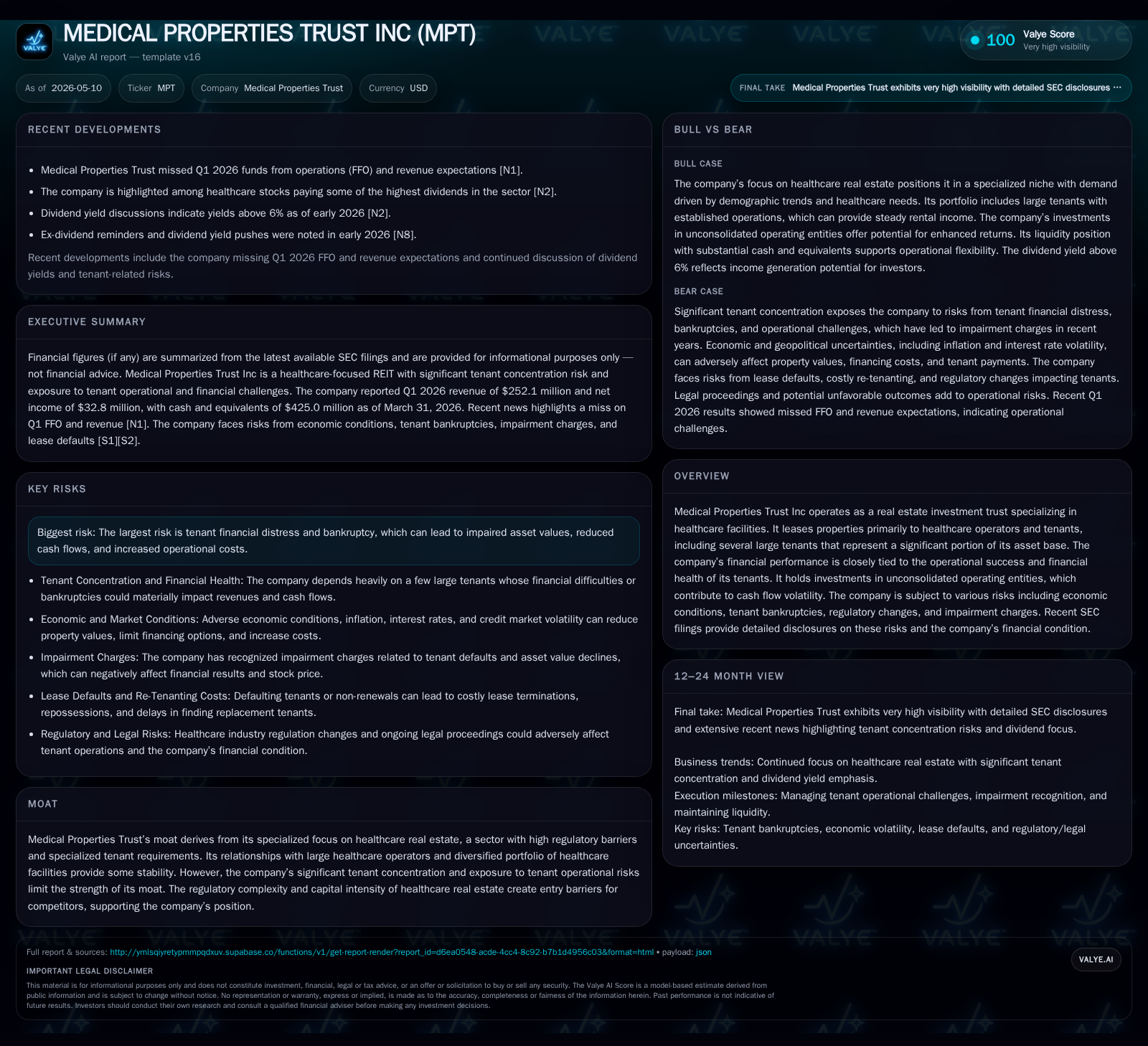

Medical Properties Trust Inc (MPT) reported weaker than expected Q1 2026 results driven by operational stress among key tenants, which impacted cash flows and rent collections. As a REIT specializing in healthcare facilities leased primarily to specialized operators, MPT's cash flow stability is closely linked to tenant health and lease compliance. While regulatory barriers and sector specialization create competitive moats, concentration risk among large tenants like Circle and Priory amplifies susceptibility to operator challenges. Growth opportunities hinge on strategic acquisitions and portfolio diversification but remain constrained by tenant credit risks and regulatory complexities. Monitoring upcoming lease renewals, tenant performance, and refinancing activity will be critical to assessing near-term execution.

Latest Quarterly Operating Update Reflects Tenant Pressure

In its May 8, 2026 Form 10-Q filing [S2], Medical Properties Trust disclosed underperformance in Q1 results that reflected mounting challenges among several key tenants. The company missed funds from operations (FFO) and revenue estimates as reported by Nasdaq on April 30 [N1], driven principally by delayed or deferred rent payments from certain large healthcare operators within its portfolio. The April 30 8-K filing [S3] supplemented this update with detailed disclosures explaining that the tenant concentration — particularly exposure to operators such as Circle Health Group and Priory Healthcare — contributed materially to earnings pressure. The reliance on these large tenants means any operational disruption or financial distress on their part directly suppresses MPT's ability to generate steady rental cash flows.

These developments highlight a notable short-term increase in cash flow volatility compared with previous periods. While long-term leases typically afford some stability for healthcare REITs, the operational difficulties facing select tenants have introduced uncertainty regarding rent timing and collectability. This situation necessitates increased monitoring of tenant credit profiles and may impede MPT’s capacity to maintain expected distributions or fund acquisitions from internally generated cash flow.

Business Model Focused on Specialized Healthcare Real Estate Leasing

Medical Properties Trust operates as a publicly traded real estate investment trust that specializes exclusively in healthcare real estate assets—primarily acute care hospitals, rehabilitation centers, behavioral health facilities, and similar specialty inpatient/outpatient medical facilities [S1]. Its revenue model derives chiefly from leasing these properties under long-term triple-net leases to healthcare operators who manage day-to-day clinical services.

Beyond traditional rental income streams, MPT also maintains certain equity interests in unconsolidated healthcare operating entities which add variability but also offer upside potential linked directly to the operators’ financial performance. This dual revenue mechanism—lease payments plus operator equity returns—is pivotal but introduces complexity; unlike pure landlord models reliant solely on rent, MPT has exposure to operating company financials which can be volatile.

The sector-specific focus requires deep expertise given the high regulatory oversight that governs patient care facilities—spanning federal HIPAA rules, CMS payment frameworks for Medicare/Medicaid reimbursement, state-level licensure requirements, and increasingly nuanced telehealth regulations. These regulatory intricacies shape both tenant behavior and lease terms; operators must maintain compliance to remain viable tenants capable of timely rent payments.

Competitive Position Navigates Regulatory Barriers and Concentration

The REIT’s moat largely stems from its specialization within highly regulated healthcare real estate markets—a space characterized by elevated entry barriers due to capital intensity, complicated zoning/healthcare licensing laws, and operational complexity of medical facilities. Competitors without integration into this niche face steep hurdles replicating MPT’s portfolio footprint.

However, an Achilles’ heel remains the remarkable tenant concentration within its operating base. The top five tenants—including Circle (14.1% of total assets), Priory (8.7%), HSA (8%), Swiss Medical (5.8%), and Lifepoint Behavioral (5.4%)—constitute a significant portion of asset valuation and rental revenues [S13][F1]. This concentration elevates credit risk since distress at any one major operator disproportionately affects overall cash flow stability.

Moreover, large master leases often contain cross-default provisions tying multiple properties under single-operator leases, multiplying operational risk exposure if defaults occur. Healthcare facility operations are challenging to transfer swiftly due to stringent regulation; replacements involve costly licensing processes that can delay re-leasing or result in asset impairments if downtime persists [S11][S17].

Growth Prospects Amid Expansion Opportunities and Tenant Dynamics

Growth strategies lean heavily on increasing scale through selective acquisitions of additional healthcare properties predominantly in established or underserved markets with robust demand for inpatient care services [S1][S3]. Enhancing geographic diversity aims to mitigate localized risk concentrations while supporting rental income resilience.

Additionally, incremental expansion is sourced from strengthening relationships with existing tenants who may require capital for renovation or expansion projects; these collaborations can enhance property values over time. Returns from equity stakes in unconsolidated operators—although more volatile—provide supplementary income growth opportunities contingent on operator success.

Nonetheless, growth potential is tempered by tenant credit quality uncertainties. Fresh acquisitions demand careful underwriting amid ongoing operational turbulence seen among some key lessees. Furthermore, regulatory shifts affecting healthcare reimbursement policies or post-pandemic patient volumes could constrain facility utilization trends critical for operator profitability and thus lease payment capacity.

Risks Surrounding Tenant Financial Health and Regulatory Exposure

Tenant insolvency risk ranks highest among concerns given its direct impact on rental collections and asset values [S11]. History shows prior bankruptcies (e.g., Steward Health in 2024) have involved protracted recovery efforts accompanied by impairment charges reducing net asset book value [S17]. Such events drain management bandwidth through litigation/court processes while increasing professional fees borne by MPT.

Healthcare industry regulation compounds risks: any adverse outcomes from regulatory investigations or enforcement actions targeting tenants—ranging from breaches of patient data privacy standards to telehealth billing irregularities—could impair tenant viability resulting in missed rents or forced lease renegotiations [S11]. Cybersecurity vulnerabilities impacting electronic health records systems represent a material emerging threat potentially triggering legal liabilities or reputational damage detrimental to lessee financial health.

Macroeconomic factors including persistent inflationary pressures increasing labor costs for hospital staffing or tightening credit conditions can further strain operator margins with knock-on effects on lease compliance dates. Additionally, fluctuations in property valuations tied closely to underlying operator strength expose MPT to periodic impairment charge risk threatening reported earnings stability.

Key Upcoming Milestones and Market Signals to Monitor

Looking ahead, several near-term events warrant close observation:

- Major tenant lease expirations/renewals: Timing coincides predominantly around clustered dates due to master leases under key operators; renewals or replacements will significantly impact occupancy/margin metrics [S2][S3].

- Quarterly earnings for upcoming periods: Further updates on FFO trends will signal whether Q1 underperformance persists or reverses.

- Debt refinancing deadlines: With nearly $9.8 billion total debt outstanding at quarter-end [F1], maturities pose refinancing execution risk especially if rental income remains stressed.

- Regulatory updates impacting major tenants: Legislative changes at federal/state levels altering reimbursements or compliance mandates could disrupt tenant economics materially. Monitoring these variables will provide signals about both short-term liquidity steadiness and longer-term portfolio quality evolution.

Current Financial Snapshot and Capital Structure Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $425mm | |

| 2026-03-31 | ||

| Total debt | $9.8bn | |

| 2026-03-31 | ||

| Net debt | $9.4bn | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

From a financial standpoint at March 31, 2026 quarter-end based on companyfacts data [F1]:

| Metric | Value (USD) | Period End |

|---|---|---|

| Cash & Equivalents | $425,001,000 | |

| 2026-03-31 | ||

| Total Debt | $9,790,218,000 | |

| 2026-03-31 | ||

| Net Debt | $9,365,217,000 | |

| 2026-03-31 |

Despite strong liquidity buffers reflective of prudent treasury management during turbulent times, the REIT carries substantial leverage consistent with capital-intensive healthcare property ownership models. High fixed-charge obligations accentuate sensitivity toward rental collection disruptions stemming from tenant operational issues discussed above.

Recent quarterly filings also reflect persistent net losses driven partly by impairment charges linked to troubled operators alongside non-cash mark-to-market adjustments related to equity investments held in unconsolidated entities [S2][S3]. This underscores the ongoing challenge balancing stable triple-net lease revenues against variable returns tied directly to operating partners’ performance nuances.

This analysis is based solely on publicly filed documents including the latest quarterly report (10-Q) dated May 8, 2026; recent event filings; industry context; and verified financial snapshot data as of March 31, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments