Myriad Genetics Faces Growth Challenges and Profitability Pressures Amid Strategic Pivot

MYGN aims to accelerate cancer testing growth while confronting reimbursement, regulatory, and operational hurdles.

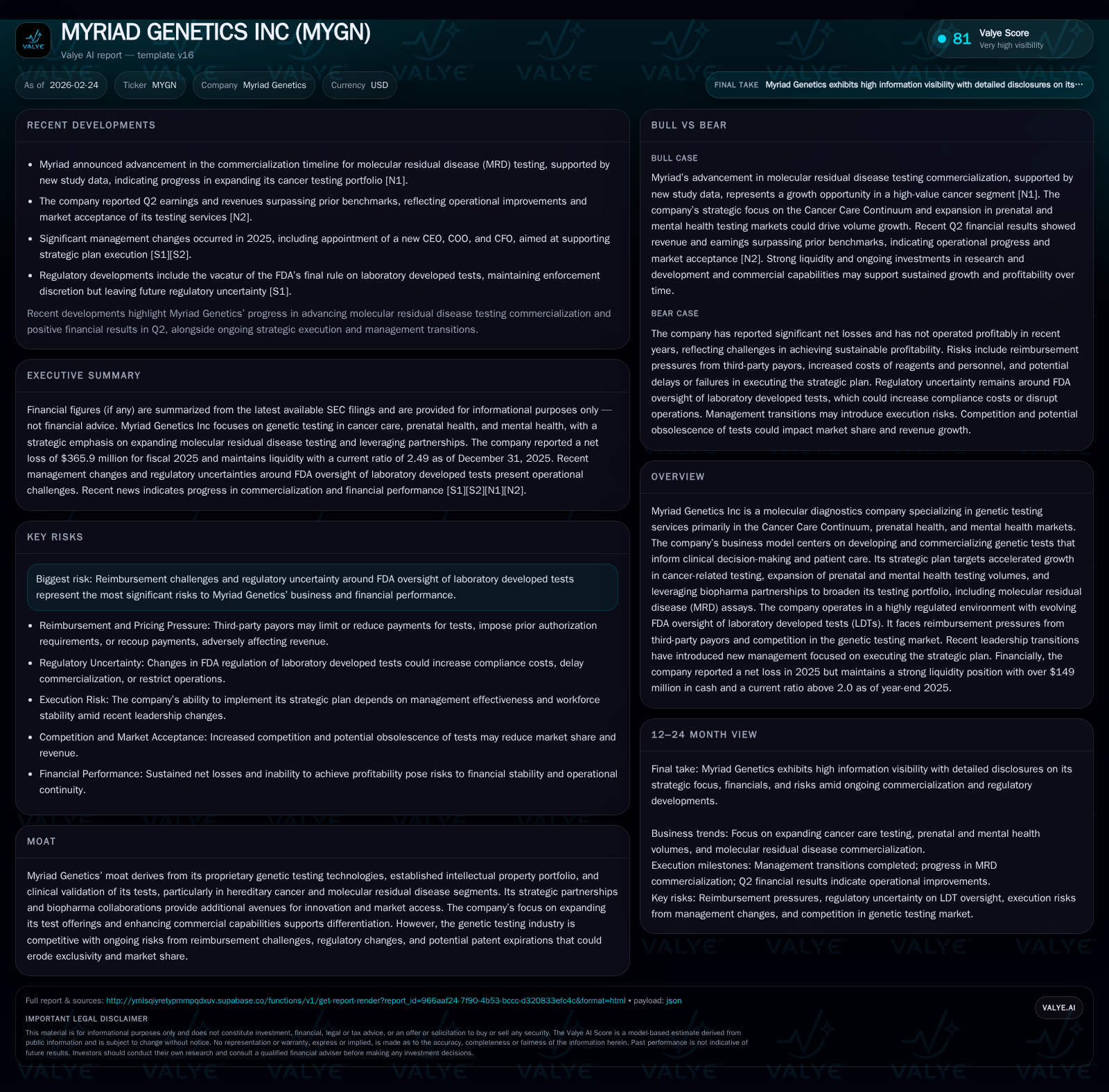

Myriad Genetics Inc specializes in genetic testing across cancer, prenatal, and mental health markets. The company’s historic revenue growth has been modest, with profitability challenges deepening over recent years, culminating in substantial operating losses in FY2025. Its strategic focus on the Cancer Care Continuum (CCC), including molecular residual disease (MRD) tests, prenatal screening expansion, and mental health testing aims to unlock new growth. However, execution risks remain high given regulatory uncertainties around FDA oversight of LDTs, reimbursement pressures, recent leadership changes, and operational cost inflation. Cash flow remains weak with negative free cash flow despite marginal positive operating cash flow in 2025. Investors should watch upcoming test volumes, reimbursement landscapes, and MRD commercialization milestones closely.

Company Overview

Myriad Genetics Inc (MYGN) operates as a molecular diagnostics company focused primarily on genetic testing services spanning the Cancer Care Continuum (CCC), prenatal health, and mental health diagnostics. Its offerings aim to inform clinical decision-making through proprietary genetic technologies supported by a robust intellectual property portfolio and clinical validation efforts. The strategic ambition revolves around accelerating revenue growth particularly in cancer-related testing via enhanced R&D investments, improved commercial engagement, and expansion into high-growth areas such as molecular residual disease (MRD) assays leveraged by strategic biopharma partnerships [N8][N9][S2].

Historical Performance

The company’s revenue trajectory over the past eight years has been relatively muted when considering the scale of investment and competitive dynamics within the molecular diagnostics sector. Key financial performance metrics extracted from filings show:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -366 | 2 | -387 | -187.4% |

| 2024 | -127 | -9 | -123 | +51.7% |

| 2023 | -263 | -111 | -257 | -135.1% |

| 2022 | -112 | -106 | -141 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -99.4 |

| 2024 | -18.2 |

| 2023 | -33.6 |

| 2022 | -12.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures for recent years are unavailable or not directly comparable; operating income and net income have deteriorated significantly since FY2022 [F1].

The stark deterioration of operating income—from about negative $123 million in FY2024 to negative $387 million in FY2025—reflects significant cost pressures and investments associated with strategic repositioning and new product development costs [S2][N1]. Net losses have similarly expanded with minimal improvement signs despite cautious progress on operating cash flow.

Industry Context

Within molecular diagnostics, particularly genetics-focused firms like Myriad, market performance is heavily influenced by test adoption rates, payer reimbursement policies, intellectual property protection duration, and evolving regulatory standards for laboratory developed tests (LDTs). FDA's recent attempts to regulate LDTs under the medical device framework were curtailed by court rulings preserving enforcement discretion but leave material uncertainty regarding future compliance cost burdens [S9]. Additionally, third-party payor pressure aims at limiting reimbursements for genetic tests given increasing scrutiny on healthcare expenditures [S13][S14]. These factors represent meaningful headwinds constraining growth and profitability potential.

Recent Developments & Future Growth Prospects

Management’s refreshed strategic plan focuses on three pillars:

Cancer Care Continuum (CCC): Acceleration through increased R&D investment; enhancement of commercial capabilities; digitizing customer experience; leveraging biopharma collaborations especially around the Precise MRD assay designed for minimal residual disease detection post-cancer therapy [S2][N8][N9]. Commercialization timelines for MRD assays have advanced with encouraging study data boosting confidence in this area.

Prenatal Health: Expansion driven by newly launched FirstGene Multiple Prenatal Screen targeting broader volumes despite a reported slight revenue decline (-4% testing volume change reported for prenatal specialties) [S25].

Mental Health Testing: Targeted growth by focusing on high-value GeneSight accounts plus leveraging state biomarker laws that potentially improve reimbursement rates; mental health test volumes showed about +6% growth [S25].

Volume trends for full year 2025 show overall modest volume expansion of ~1%, broken down as hereditary cancer +7%, mental health +6%, and prenatal health declination by ~4%, underlining mixed prospects across segments [S25].

Optimizing operational agility amidst these sectoral shifts is pivotal given past managerial transitions — with the CEO role changing hands recently and key senior commercial roles also reshuffled — introducing short-term execution risk [S20].

Financial Outlook & Milestones to Watch

Explicit management guidance disclosed early 2026 sets expectations around steady though unspectacular volume gains paired with continued investment spending supporting longer term innovation projects like MRD commercialization [N6][N8]. Key observable milestones include:

- Successful clinical validation data rollouts for Precise MRD;

- Adoption rates within oncology workflows;

- Expansion in prenatal product lineup acceptance;

- Progress on improved payor reimbursement terms especially under state biomarker laws applying to mental health testing;

- Managing regulatory developments impacting LDT classification.

Absent further formal guidance disclosures beyond preliminary forecasts, analysts should track quarterly volume data releases alongside payer policy updates for clues into trajectory shifts .

Returns & Capital Allocation

ROE remains deeply negative at approximately -99%, owing largely to sustained net losses against declining equity bases reflecting write-downs or prior share repurchase amortizations [F1]. Operating cash flow shifted positive marginally (+$1.8M) compared to heavy negative outflows historically but free cash flow is still negative given ongoing capital expenditures likely related to lab expansions or technology upgrades [F1]. Dividend payments are not disclosed indicating no current shareholder distributions; buybacks ceased after FY2019’s $50 million program [F1]. Thus capital allocation appears focused on sustaining operations and funding R&D rather than returning cash.

Risks & Challenges

Reimbursement risk predominates with payors increasingly demanding evidence of clinical utility while seeking to limit reimbursement expansion or impose administrative barriers like prior authorizations [S13]. Regulatory uncertainty about FDA oversight could suddenly impose costly premarket clearances or quality system mandates [S9]. Intellectual property risks remain given patent expirations potentially eroding exclusivity over core hereditary cancer tests [S10]. Operational risks include talent retention challenges post-executive reshuffles compounded by inflationary pressures elevating reagent costs and personnel expenses [S20]. Lastly, competitive pressure from large integrated diagnostics providers maintaining rapidly evolving platforms intensifies market share contests.

Conclusion

Myriad Genetics’ strategic pivot toward driving CCC market growth through MRD assay commercialization while reinforcing prenatal and mental health testing volumes represents a logical alignment with high-growth opportunities within molecular diagnostics sectors shaped by precision medicine advances. However, large-scale structural challenges manifesting as sustained profitability deficits ($-387M operating loss in 2025), uncertain regulatory frameworks governing LDTs gone forward, constrained reimbursement environments, and operational execution risks temper near-to-medium term optimism.

Investors should closely observe quarterly test volumes segmented by cancer versus other areas; regulatory updates particularly any FDA moves affecting test approvals; payer negotiations outcomes tied to new state biosignature laws; management commentary post-leadership changes; and commercialization progress on Precise MRD assay offering clear visibility into the turnaround trajectory prospects for Myriad’s business model.

Disclaimer: This document is strictly an informational analysis based on public filings and news sources up to February 2026 and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments