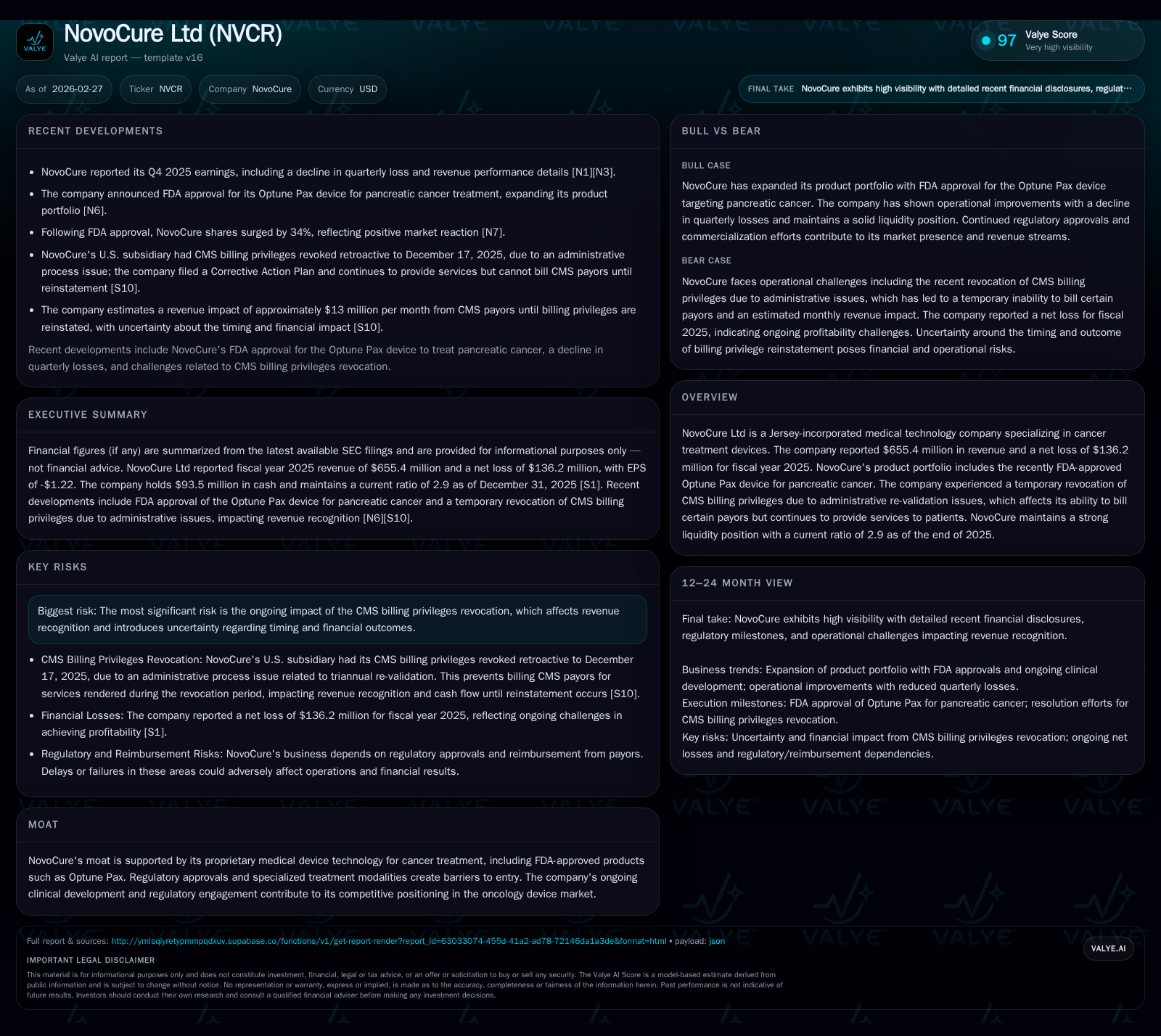

NovoCure's Transition: Balancing Innovative Cancer Technologies and Financial Challenges

NovoCure Ltd's revenue growth through oncology device innovation contrasts with financial impacts from CMS billing disruptions.

NovoCure Ltd has demonstrated robust revenue expansion driven by its tumor treating fields technology, culminating in $655 million for fiscal year 2025. This growth was propelled by the recent FDA approval of Optune Pax for pancreatic cancer, expanding its therapeutic footprint. However, the company faced a significant operational hurdle when its CMS billing privileges were temporarily revoked, introducing uncertainty in revenue recognition and cash flows. Despite this setback, NovoCure maintains a strong liquidity position and continues investing in clinical development and product portfolio expansion.

Innovative Medical Technology Fueling Revenue Growth

NovoCure has exhibited a remarkable trajectory of top-line expansion over the past four years, scaling revenue from $128 million in fiscal year 2022 to approximately $655 million in fiscal year 2025 [F1]. This growth is fundamentally anchored in the adoption of its proprietary medical devices employing tumor treating fields (TTFields) technology—a non-invasive modality that uses electric fields to disrupt cancer cell division. Early commercial success focused on glioblastoma multiforme enabled penetration into specialized oncology markets where device clinical adoption rates gathered momentum.

The company’s continual investment in R&D and regulatory engagement catalyzed the diversification of its therapeutic indications. A landmark advancement came with FDA approval of Optune Pax®, an iteration adapted specifically for locally advanced pancreatic cancer treatment alongside chemotherapy regimens [N7][S5]. This approval not only broadened NovoCure’s portfolio but also reinforced its competitive moat derived from proprietary device design coupled with intensive clinical validation.

Such innovations underpin sustained revenue momentum as NovoCure capitalizes on expanding clinical utility and deepening presence across oncology care protocols. The company’s ability to translate FDA clearances into rapid market uptake velocity among oncologists and payors remains pivotal for future growth.

Impact of CMS Billing Privileges Revocation on Financial Results

In early 2026, NovoCure encountered a material setback when CMS temporarily revoked its Medicare and related CMS payor billing privileges retroactive to December 17, 2025 [S9][S10][N1][N2]. Contrary to substantive compliance failures, the revocation stemmed from administrative process complications within the triannual CMS re-validation cycle — highlighting payer compliance risks inherent to reimbursement workflows in medtech.

During this period, while NovoCure continued providing therapeutic services to new and existing patients, it was barred from billing CMS payors. The management estimates foregone revenue totaled approximately $13 million monthly until reinstatement was secured retroactively on February 24, 2026 [S9]. Billing backquests for services rendered during suspension remain uncertain regarding collectability.

This disruption introduced pronounced volatility into near-term revenue recognition and cash flow profiles, complicating forecasting and reporting clarity. The incident underscores operational dependencies on payer administrative processes even amid strong clinical value propositions.

Financial Performance Trends: Revenue, Losses, and Cash Flows

NovoCure’s financial progression reflects a classic medtech growth phase characterized by accelerating sales juxtaposed with ongoing operating losses attributable largely to heavy R&D investment and commercialization efforts. The following table summarizes key financial metrics for fiscal years 2022 through 2025 [F1]:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 655 | -136 | -49 | -154 | +8.3% | +19.2% |

| 2024 | 605 | -169 | -26 | -170 | +18.8% | +18.6% |

| 2023 | 509 | -207 | -73 | -233 | +296.6% | -455.0% |

| 2022 | 128 | -37 | 31 | -43 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -76 | -40.0 |

| 2024 | -69 | -46.8 |

| 2023 | -100 | -57.1 |

| 2022 | 9 | -8.5 |

Source: SEC companyfacts cache [F1].

Starting from modest revenue base in FY2022, the company experienced explosive sales escalation fueled by clinical adoption and new market launches before decelerating slightly in growth rate to mid-single digits by FY2025 [F1]. Operating losses have narrowed significantly proportionally though remaining sizable due to scale-up costs.

Operating cash flows turned negative since FY2023 as increased working capital absorption outpaced profitability gains; capital expenditure patterns show variability aligned with strategic investments primarily targeting capacity expansion and platform improvements [F1]. The approximate return on equity ratio remains deeply negative (~-40%) reflective of the ongoing investment-heavy phase [F1].

Product Portfolio Expansion with Optune Pax for Pancreatic Cancer

A critical strategic catalyst for NovoCure came from regulatory milestone attainment with FDA granting marketing clearance for Optune Pax® aimed at adults suffering locally advanced pancreatic cancer used concomitantly with gemcitabine and nab-paclitaxel chemotherapy [S11][N7][N11]. This indication expansion transitions the firm beyond prior exclusive focus areas such as glioblastoma towards addressing broader solid tumors therapy landscapes.

The Optune Pax launch exemplifies a vanguard effort linking tumor treating fields mechanism with distinct oncologic settings thereby increasing the device indication breadth and potential patient population served [S5]. Early market response evidenced by substantial share price appreciation underscores investor recognition of enhanced market opportunity coupled with durable competitive advantages grounded in clinical efficacy data [N12][N11].

Continued portfolio growth is anticipated through incremental pipeline developments targeting additional cancer types where TTFields could confer therapeutic benefit—emphasizing innovation-driven differentiation amid intensifying oncology device competition.

Capital Allocation, Liquidity, and Balance Sheet Strength

Despite net losses and cash burn patterns typical for development-stage medtech companies advancing product pipelines, NovoCure sustains a robust liquidity profile underscored by a current ratio of approximately 2.9 as of end-2025 [F1][S13]. Total current assets stood at $647 million against $223 million current liabilities providing ample buffer to absorb operational uncertainties including reimbursement interruptions.

Equity declined modestly from $441 million at end-2022 to $340 million at end-2025 reflecting cumulative losses during scale-up [F1]. No dividends or share repurchase programs have been undertaken recently consistent with prioritization of reinvestment into R&D and commercial infrastructure [F1].

Capital expenditures decreased notably in FY2025 compared to prior year indicative of refined capital intensity management aligned with strategic priorities balancing growth investments versus cost discipline [F1][S13]. Overall working capital management practices appear calibrated to support ongoing innovation cycles without jeopardizing financial flexibility.

Forward Outlook: Market Penetration and Regulatory Risk Resolution

Looking ahead, recovery from the transient CMS billing privileges disruption is paramount for restoring stable reimbursement streams enabling uninterrupted revenue capture [N1][N2][S9][S10]. Management’s corrective action plan filing coupled with reinstatement foreshadows normalization yet exact timing for complete financial impact resolution remains fluid.

Additional FDA approvals or positive pivotal clinical trial results would act as regulatory milestone catalysts potentially unlocking expanded coverage decisions amongst payors beyond Medicare scope—especially relevant given evolving payer dynamics within US oncology sectors . Meanwhile competitive positioning benefits from entrenched TTFields intellectual property protections paired with proprietary manufacturing know-how enhancing barriers against new entrants.

Ongoing leadership under newly appointed CEO Frank Leonard—who brings extensive commercial operations experience within NovoCure—aims to accelerate market penetration efficiencies while navigating complex reimbursement ecosystems delicately balancing innovation priorities against regulatory compliance demands [S20][S23].

Key Milestones to Watch in Clinical Development and Reimbursement

From an analytical vantage point focused on critical upcoming inflection points:

- Further clinical trial readouts assessing efficacy/safety across additional tumor types represent potential sources of new therapeutic indications extending device applications beyond pancreatic cancer [N7].

- Timely remediation of administrative compliance processes ensuring uninterrupted CMS payer coverage remains an immediate operational priority directly impacting near-term cash flow realization [N1].

- Payor policy shifts internationally or domestically—whether tightening or broadening coverage parameters—must be closely monitored given their direct influence on patient access levels affecting adoption curves within commercial rollouts .

A synthesis of these elements frames a nuanced balance where ongoing R&D productivity integrates tightly with proactive payer engagement forming dual pillars essential for substantiating sustainable long-term commercial viability.

This analysis synthesizes publicly available SEC filings and recent news sources without projection beyond verified disclosures and facts known as of February 27, 2026. It is intended exclusively for informational purposes without any investment advice or recommendation concerning NovoCure Ltd or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments