Owens Corning's Turnaround Challenge: Evaluating Pressures and Growth Levers

Owens Corning faces mounting profitability pressures despite stable revenues, navigating macroeconomic challenges and operational scale.

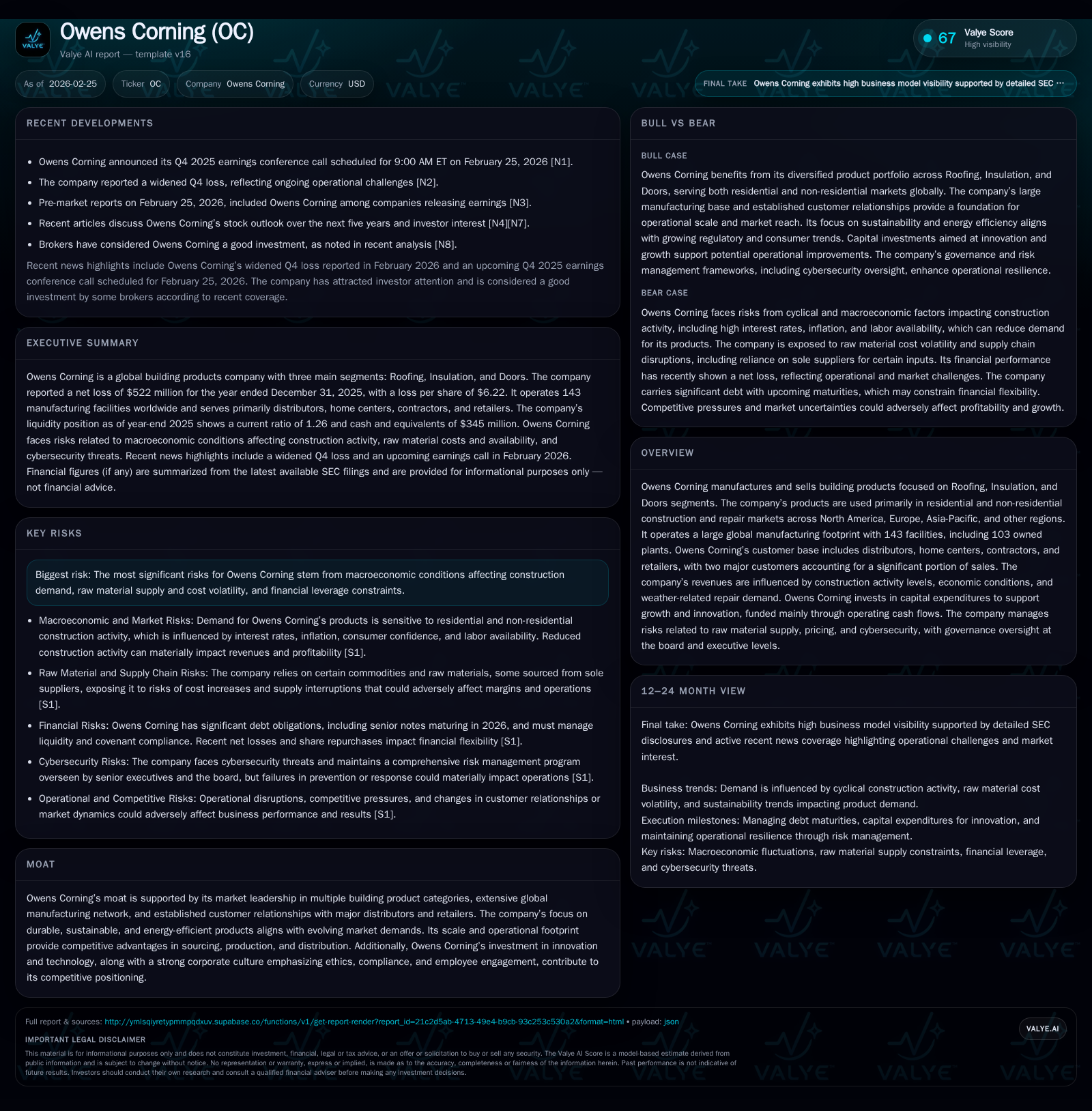

Owens Corning recorded only marginal revenue growth of 1.5% in 2025 yet suffered a severe operating income decline of 68%, culminating in a significant net loss of $522 million. The company’s extensive manufacturing footprint and product leadership have buffered top-line resilience, but escalating input costs, industry cyclicality, and integration costs from recent acquisitions compress margins. With ample liquidity and a strengthened credit facility, Owens Corning continues capital allocation through sizeable buybacks and dividends funded by robust cash flow. Near-term growth hinges on housing market dynamics and cost management, while cybersecurity and regulatory risks remain under close governance.

From Expansion to Earnings Pressure: Growth and Drivers Through 2025

Owens Corning's topline growth in 2025 was tepid at best, with revenues advancing just 1.5% year over year to roughly $10 billion [F1]. This modest expansion belies significant operational challenges evident in profitability metrics. Operating income cratered by over two-thirds (-68.1%) from $1.13 billion in 2024 to a mere $360 million in 2025 [F1], signaling sharp margin deterioration despite flat sales.

Net income performance further underscores these struggles: Owens Corning swung from a healthy net profit of $647 million in the prior year to a deep loss of approximately $522 million [F1]. The disparity between stable revenue streams and collapsing earnings points to pressure from surging input costs, disruption-related expenses, or nonrecurring charges. Segment disclosures confirm that Roofing, Insulation, and Doors remain core drivers; however, shifting product mix dynamics alongside elevated costs appeared to weigh heavily on corporate results [S5].

Notably, the company runs an extensive global manufacturing footprint — totaling 143 facilities worldwide with 103 owned plants — providing significant capacity across all reportable segments [S1]. Despite this scale which should enable sourcing efficiencies and market coverage, margin compression indicates that fixed cost absorption or cost inflation has outpaced sales gains.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -522 | 1786 | 360 | 824 | -180.7% |

| 2024 | 647 | 1892 | 1127 | 647 | -45.9% |

| 2023 | 1196 | 1719 | 1812 | 526 | -3.6% |

| 2022 | 1241 | 1760 | 1714 | 446 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 232 | 815 | 962 |

| 2024 | 208 | 491 | 1245 |

| 2023 | 188 | 657 | 1193 |

| 2022 | 136 | 795 | 1314 |

Source: SEC companyfacts cache [F1].

Notes: Revenue for years prior to 2025 are not directly available; Operating Income and Net Income for same periods are present for contextual YoY calculation only where data allows.[F1]

Operating cash flow remained relatively robust at approximately $1.79 billion in 2025 despite the net loss, reflecting solid working capital management or non-cash charges impacting earnings [F1]. Capital expenditures ramped up sharply by over 27% year over year to $824 million reflecting investments targeted at sustaining capacity and fostering innovation [F1],[S13]. Dividend payments increased moderately to $232 million while share repurchases accelerated to $815 million—demonstrating the company's commitment to shareholder returns despite earnings volatility [F1],[S19],[S20].

Industry Forces and Company-Specific Constraints on Near-Term Growth

The building materials industry remains highly attuned to residential housing starts, commercial construction cycles, and renovation activities that collectively drive demand for Owens Corning's Roofing, Insulation, and Doors products [S5]. North American markets dominate revenue exposure—where residential new construction and repair plus remodeling underpin volumes—while Europe and Asia-Pacific lean more towards non-residential applications influenced by industrial production trends [S5],[S8].

Macro headwinds—such as inflationary pressures on raw material inputs including petrochemical derivatives for insulation foam and fiberglass production—continually strain manufacturing margins amidst supply chain tightness [N7],[S11]. Owens Corning’s large-scale operations provide cost advantages through broad sourcing capabilities, but persistent volatility in raw material pricing remains a formidable challenge that limits pricing power downstream.

Cybersecurity governance emerges as a critical risk vector within this digital era; the company maintains vigilant oversight through its Audit Committee backed by senior IT leadership including the Chief Information Officer with more than two decades of experience [S1]. This structure is designed to preempt operational disruptions rooted in cyber threats.

Financial leverage constraints constitute another strategic consideration given Owens Corning's sizable $5.2 billion long-term debt portfolio primarily from senior notes with staggered maturities [S6],[S13]. Amendments excluding certain non-cash impairment charges from leverage ratio calculations reflect proactive covenant management enhancing liquidity flexibility during turbulent earnings periods [S4],[S6].

The company’s dependence on two major customers—accounting for nearly a quarter of consolidated sales—poses concentration risk alongside potential pricing pressure or demand fluctuations germane to these partners [S5],[S14].

2026 Expectations and What Investors Should Watch Next

Official public guidance for full-year 2026 remains limited as per recent earnings calls and broker reports; however, monitoring backlog trends within residential construction markets will be pivotal given their outsized influence on Roofing and Insulation segment volumes [N3],[N8]. Cost containment initiatives targeting procurement optimization and productivity gains also feature prominently in management commentary as mechanisms intended to arrest margin erosion.

Capex projections hover near last year's elevated levels at about $800 million focused on sustaining manufacturing capability enhancements and technology deployment aligned with sustainability goals [S13],[N10]. New product innovations emphasizing energy efficiency dovetail with increasing customer demands amid tightening environmental standards—offering potential differentiation levers.

Watch also for any operational milestones related to integration fallout or remediation costs stemming from Paroc’s product recalls in the European marine insulation category—a continuing liability risk factor influencing overall segment profitability [S18].

Capital Allocation Discipline: Buybacks, Dividends, and Cash Flow Analysis

Despite posting negative net income for the first time since pre-pandemic years, Owens Corning generated free cash flow close to $962 million after accounting for capex outlays in excess of $800 million [F1]. This robust cash generation enabled continuation of disciplined capital returns consisting of $232 million dividend payments—the highest on record—and aggressive share repurchases totaling approximately $815 million during fiscal year 2025 [F1],[S19],[S20].

Liquidity remains ample with cash balances above $340 million complemented by a recently expanded Senior Revolving Credit Facility bumped up from $1 billion to $1.5 billion maturing in March 2030, providing substantial borrowing headroom unused as of December-end [S4],[S6],[S15]. Importantly, the revolving facility's February 2026 amendment excluded specific impairment charges from leverage calculations—a notable concession improving covenant compliance prospects amid cyclical earnings downturns.

Credit metrics such as net debt-to-EBITDA ratios require careful watching given EBITDA contracted significantly but remain somewhat cushioned by adjustments excluding impairment charges [S15].

Operational Scale, Product Leadership, and Strategic Innovation

Owens Corning’s wide global platform comprises 143 manufacturing sites including its R&D centers spanning Ohio-based Science & Technology Center encompassing more than half a million square feet devoted to advanced product development [S1]. This footprint enables proximity to key markets in North America, Europe, Asia-Pacific delivering supply chain levers critical for meeting both new construction demand spikes and repair/remodel bursts driven by weather events or aging building stock repairs.

Product line breadth spanning Roofing shingles/materials, Fiberglass Insulation solutions tuned for thermal efficiency, acoustic control along with Doors products integrates synergies that appeal across contractor distributors, home centers, retailers plus commercial developers alike [S8]. This multifaceted offering backed by ongoing innovation efforts—including executive leadership hires focusing on R&D acceleration—positions Owens Corning well amid intensifying competition grounded on sustainability-driven product performance requirements.

Strategically embracing trends toward durable, eco-conscious materials reflects both customer expectations and tightening regulatory imperatives framing building codes globally.

Risk Oversight in a Cyclical Market: Governance and Compliance Focus

Robust governance underpins risk oversight across financial operations and expanding digital security demands—a paramount concern underscored by detailed cybersecurity protocols led directly by Owens Corning’s CIO reporting lines into CEO-level oversight committees [S1]. The layered approach includes continuous monitoring via internal teams supplemented by external security suppliers ensuring timely detection/mitigation of incidents.

Cyclical fluctuations characteristic of construction materials sectors dictate vigilant enterprise risk management encompassing supply chain disruption contingencies linked with commodities inflation alongside macroeconomic slowdowns linked with housing market softness or broader industrial downturns [S11],[N7]. Environmental compliance matters especially related to recent recall events further highlight regulatory complexity adding cost uncertainty axes requiring proactive legal reserve establishment.

Owens Corning’s documented code of conduct emphasis paired with robust quality assurance programs seeks to engender ethical culture traits easing navigation through fragmented global regulatory landscapes while aligning internal performance objectives around inclusion/diversity priorities supporting workforce engagement crucial during turnaround efforts.

This analysis is grounded exclusively on reported data as of February 25, 2026 without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments