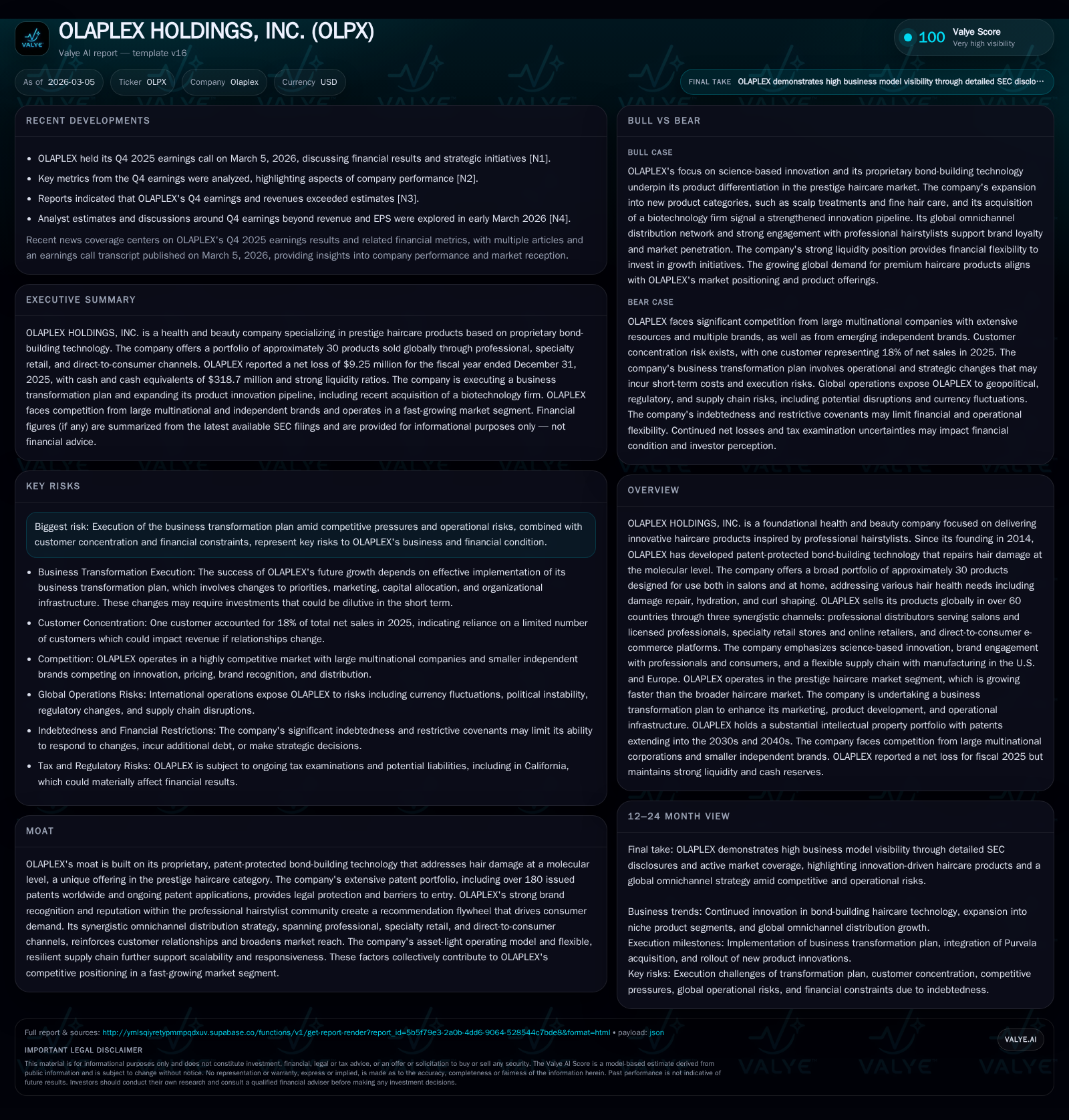

OLAPLEX Holds Strong Global Footprint While Managing Transformation and Profitability Challenges

OLAPLEX leverages proprietary bond-building technology and a synergistic omnichannel model but faces operational and financial execution risks amid competitive pressures.

OLAPLEX has pioneered molecular-level hair repair technology since 2014, expanding from professional salon treatments to a wider portfolio sold globally through professional, specialty retail, and direct-to-consumer channels. The company’s moat is anchored in its extensive patent portfolio and strong brand loyalty, particularly among hairstylists. After rapid growth including impressive profitability through 2023, OLAPLEX reported a steep earnings decline in 2025 driven by strategic investments in its business transformation plan and channel resets. Its balance sheet remains strong with high liquidity, but navigating competitive pressures, customer concentration, regulatory complexities, and integration risks of acquisitions will be key to restoring profitability and sustaining growth.

Company Overview

Founded in 2014, OLAPLEX HOLDINGS, INC. (ticker: OLPX) has established itself as a foundational player in the prestige haircare segment by introducing a novel, patent-protected bond-building technology (Bis-aminopropyl diglycol dimaleate) that repairs hair damaged at the molecular level. This innovation disrupted the haircare industry by enabling professionals ('Pros') to restore disulfide bonds damaged during chemical treatments such as coloring or perming. OLAPLEX quickly expanded its footprint beyond salons via an at-home regimen launched within the same year.

Over the years, the company broadened its product line to approximately 30 items designed for holistic hair health addressing damage repair from chemical, thermal, environmental, and mechanical sources. These products serve diverse hair needs including hydration and curl shaping – evidenced by their recent launch of an in-salon curl repair service featuring proprietary technology [S1].

Historical Performance and Growth Drivers

From inception through 2023, OLAPLEX experienced robust top-line growth facilitated by rapid adoption among professional salons globally and growing consumer awareness via social media-driven demand loops. The company’s strategy leans heavily on engagement with professional hairstylists who act as both users and brand advocates.

Financially, this translated into significant profitability with operating income peaking at $364 million in 2022 before contracting to $108 million in 2023 [F1]. Net income followed a similar pattern with $244 million earned in 2022 and $61.6 million in 2023 before turning negative in the latest fiscal year.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -9 | 59 | 7 | 331000 | -147.4% |

| 2024 | 20 | 143 | 67 | 1124000 | -68.3% |

| 2023 | 62 | 178 | 108 | 375000 | -74.8% |

| 2022 | 244 | 255 | 364 | 650000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 58 | -1.1 |

| 2024 | 142 | 2.2 |

| 2023 | 177 | 7.3 |

| 2022 | 255 | 31.3 |

Source: SEC companyfacts cache [F1].

*Prior year YoY changes calculated backward from known values [F1]. Revenue figures were not explicitly provided.

Despite relatively low capital expenditures characteristic of an asset-light cosmetics company (capex dropped to $331k in FY2025), OLAPLEX sustained solid operating cash flow of $58.7 million in FY2025, yielding free cash flow near $58 million after capex deductions [F1]. This demonstrates operational resilience despite net losses recorded last year.

Business Transformation Plan Impact

Management has highlighted ongoing investments tied to their business transformation plan including resetting international distribution networks using a tiered market approach; enhancing sales & marketing efforts targeting both Pros and consumers; accelerating innovation pipelines supported by acquisitions like Purvala completed August 2025 [S27]; and organizational restructuring with IT upgrades [N1],[S1].

These initiatives have increased costs contributing to a sharp contraction in operating income compared to prior years [F1]. Management acknowledges these short-term margin pressures are part of repositioning for longer-term scale benefits [N3].

Channels & Market Reach

OLAPLEX operates globally across more than sixty countries via three main channels:

- Professional Channel: Products distributed mainly through beauty supply distributors serving licensed professionals and salons; over one hundred distributors worldwide enforce territorial exclusivity where applicable [S12].

- Specialty Retail: Products available through leading online and brick-and-mortar specialty retailers across approximately twenty countries.

- Direct-to-Consumer (DTC): Online sales primarily via Olaplex.com plus third-party e-commerce platforms enhance direct consumer engagement and education [S13].

In FY2025, about half of net sales originated domestically (48%) with international sales comprising the remainder (52%) [S7]. One customer accounted for a significant portion—18%—of total sales presenting concentration risk [S7],[S20].

Competitive Environment and Moat

OLAPLEX’s core competitive advantage derives from its patented Bis-amino chemistry with over 180 patents globally protecting this proprietary molecule complex [S26]. This molecular repair technology differentiates it from traditional cosmetic products focused on surface effects.

Brand loyalty among professionals fuels a recommendation flywheel sustaining demand despite competition from multinational conglomerates such as Estee Lauder and L’Oreal alongside emerging indie brands leveraging customization and digital marketing.

However, maintaining differentiation requires continuous innovation amidst regulatory scrutiny over advertising claims worldwide [S15],[S26]. Failure to comply or maintain efficacy could harm brand reputation disproportionately.

Regulatory & Legal Landscape Risks

Operating internationally exposes OLAPLEX to complex regulations governing ingredient approvals, marketing claims validation (e.g., FDA, FTC in U.S., EU REACH chemical reviews including Bis-amino analogs) [S9],[S14],[S15]. Noncompliance risks include product recalls or fines potentially impacting sales.

Supply chain dependencies centered on third-party manufacturers primarily in the U.S. pose risks of disruption due to natural disasters or geopolitical events [S20],[S27],[S28]. Intellectual property litigation risk also persists amid rapid innovation cycles requiring costly global patent defense [S10],[S19],[S28].

Capital Structure & Financial Positioning

As of December 31, 2025, OLAPLEX held cash & equivalents exceeding $318 million with current assets more than four times current liabilities—a current ratio near 4.58x—indicating strong liquidity [F1]. Equity stood robustly at $879 million reflecting accumulated retained earnings despite recent losses.

The company carries significant debt subject to restrictive covenants limiting operational flexibility including constraints on dividends—which have not been declared historically—and additional indebtedness without creditor approval [S18],[S23]. Capital allocation currently prioritizes reinvestment over shareholder returns.

Future Growth Prospects & Considerations

Key growth drivers include expanding international markets focused on selective tiers with tailored investment strategies; deepening Pro engagement; broadening DTC channel penetration supported by technological enhancements such as AI-enabled marketing initiatives mentioned but not detailed publicly [N1],[S25]. New product formats like curl-specific bond shaping services introduced recently offer innovation-led top-line expansion beyond foundational bond building treatments.

Risks include delays or failure in transformation plan execution prolonging margin pressure; intensified competition especially from large incumbents with scale advantages; evolving consumer preferences toward clean beauty requiring reformulation; supply chain shocks affecting availability; regulatory actions impacting key ingredients; concentrated customer exposure influencing bargaining power; and talent retention challenges potentially disrupting momentum [S1,S16,S21,S25].

Monitoring milestones such as progress on international distributor network resets; improvements reversing FY25 profitability declines; innovation pipeline cadence post-Purvala acquisition integration success; evolving channel mix shifts favoring DTC growth; plus regulatory review outcomes notably EU dossier assessments remain critical [N1,N3,S27,S29].

Conclusion

OLAPLEX occupies a distinctive niche underpinned by proprietary molecular haircare technologies supported by a leading global IP portfolio leveraged through omnichannel distribution spanning salons to e-commerce platforms worldwide. The recent profit compression reflects deliberate transformational investments recalibrating international presence amid intensifying competition.

Strong liquidity and an asset-light model provide financial resilience while rising indebtedness imposes operational constraints limiting near-term capital return options. Navigating complex global regulatory environments while preserving product efficacy perception is paramount given evolving requirements.

Ultimately, OLAPLEX’s ability to sustain its moat depends on successful execution of strategic initiatives alongside continued innovation leadership maintaining its competitive edge within premium haircare sectors reshaped by digital consumer engagement trends.

This analysis is based solely on documented filings and publicly available transcripts without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments