PEGASYSTEMS Faces Q1 Revenue Decline Despite Strong Cloud Growth and Litigation Overhang

Pegasystems reports slower overall subscription revenue in Q1 2026, with Pega Cloud showing robust growth amid legal uncertainties.

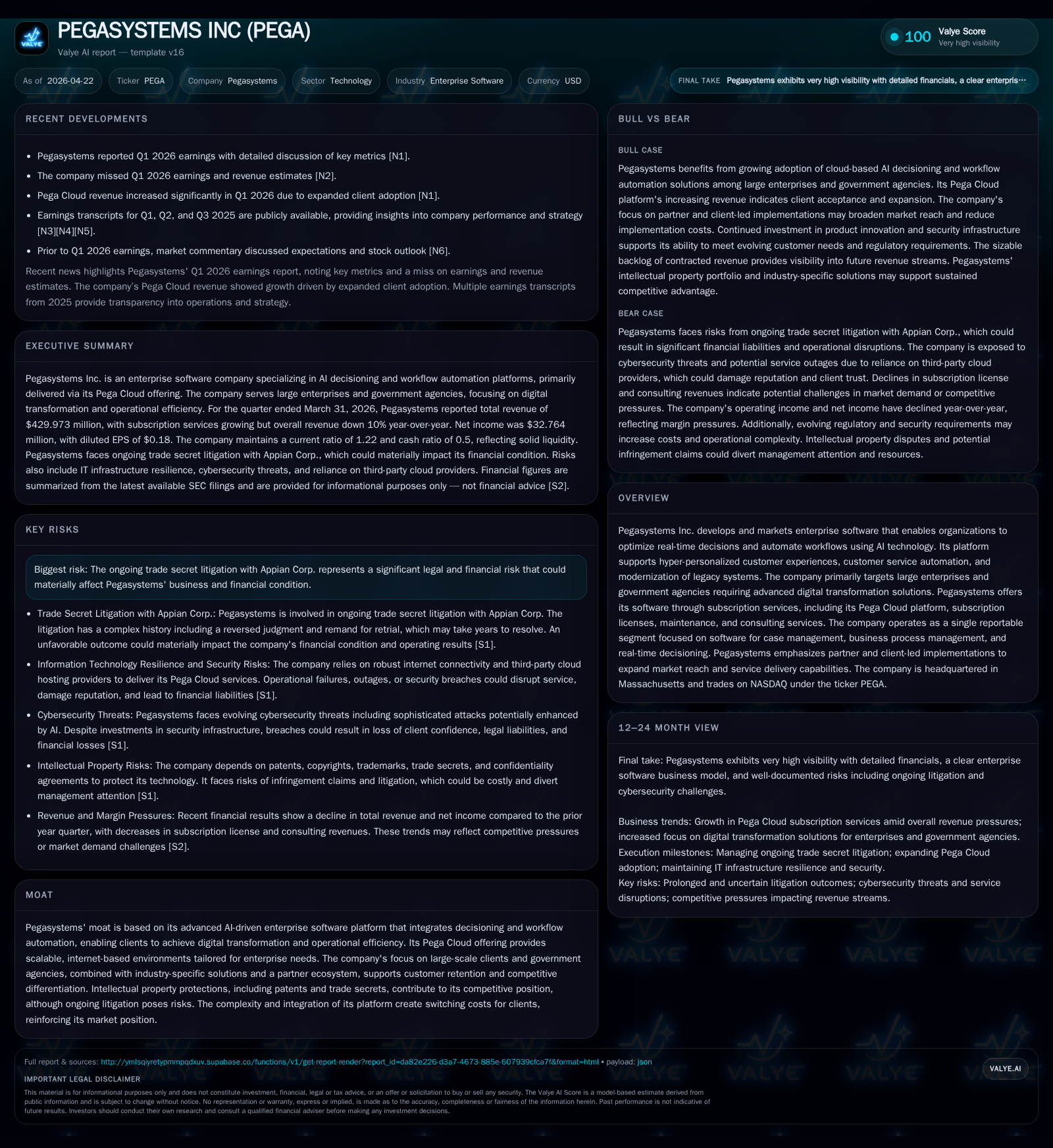

In its latest quarterly filing for Q1 2026, Pegasystems reported total revenues of $430 million, down from $476 million a year ago, mainly due to a nearly 50% decline in subscription license revenue. However, its Pega Cloud segment grew 36%, signaling strong adoption of its cloud offerings. The company continues to navigate substantial legal risks stemming from ongoing trade secret litigation with Appian Corp., which could materially impact future operations. Pegasystems maintains a single reportable segment focused on AI-powered decisioning and workflow automation software sold primarily to large enterprises and government agencies. Growth drivers remain anchored in the cloud transition and AI integration, while execution risks arise from litigation and consulting service capacity limitations.

Recent Operating Update

Pegasystems' latest quarterly filing (10-Q dated April 21, 2026) shows mixed operational developments that underscore both opportunity and risk in the near term [S2]. Total revenue for Q1 2026 hit $429.97 million, down from $475.63 million a year earlier (a ~10% decline). A key driver was the drastic fall in subscription license revenues by nearly half (down from $187.7 million to $94.9 million), indicating waning demand or strategic de-emphasis on legacy licensing models.

Conversely, Pega Cloud revenues surged 36% year-over-year to $205 million, reflecting healthy adoption of their cloud-based SaaS platform amidst broader enterprise IT transitions [S2]. Overall subscription services—which bundle cloud and recurring licenses—declined by just 10%, highlighting that cloud growth partially offset legacy declines.

Maintenance revenues were essentially flat at $75 million, while consulting fees dropped 9% to $54.8 million as Pegasystems scaled back direct staff-led implementations in favor of partner- and client-led approaches [S2]. This aligns with the firm’s strategic pivot toward enabling an ecosystem-led delivery model intended to expand capacity without proportionally increasing internal consulting headcount.

The company also disclosed other liabilities reductions on deferred revenue reflective of changing billing cycles or contract composition [S2]. Notably, net income declined sharply to $32.8 million from $85.4 million previously owing partly to restructuring costs and ongoing legal expenses associated with protracted trade secret litigation [S2].

Business Model Overview

Pegasystems operates a single reportable segment specializing in AI-powered enterprise software that combines business process management (BPM), real-time decisioning, case management, and customer relationship management (CRM) capabilities [S1], [S19]. The firm primarily targets large enterprises and government organizations seeking digital transformation through automation and personalized customer experiences.

Its revenue streams comprise subscription services (inclusive of Pega Cloud SaaS hosting), subscription licenses (traditional perpetual or term licenses), maintenance contracts providing updates/support, and consulting services focused on software implementation and integrations [S1], [S2]. The growing importance of the Pega Cloud subscription model signals a transition away from upfront license fees toward predictable recurring revenues.

Consulting services are integral to onboarding new clients as well as managing complex implementations that require customization and integrations with legacy systems [S1]. However, Pegasystems emphasizes expanding partner- and client-led implementations thereby reducing dependency on internal consultants—a double-edged sword impacting consulting top-line but aimed at improving scalability.

Technologically, Pega's platform integrates AI-driven decision engines with workflow automation capabilities facilitating hyper-personalized interactions at scale—a critical differentiator given market demand for flexible low-code/no-code platforms supporting continuous change [S1], [S14]. Their proprietary intellectual property includes patents covering decisioning technologies fueling their competitive moat.

Industry Structure and Competitive Position

Enterprise BPM/CRM software is highly competitive featuring several large incumbents such as Salesforce, IBM (via IBM Automation), Microsoft Dynamics, and emerging specialized players focusing on AI-driven automation like Appian—the latter notably involved in ongoing patent/trade secret litigation against Pegasystems [S4], [S15].

Pegasystems positions itself as an AI-first platform vendor targeting complex enterprise use cases requiring real-time decisions coupled tightly with adaptive process flows rather than pure CRM or task management solutions . This focus on integrated decisioning plus case management builds stronger switching costs compared to point solutions.

The company’s cloud offering benefits from internet-scale architecture tailored for enterprise workloads—meeting evolving regulatory/compliance demands while maintaining ISO/IEC certifications essential for government sector customers [S1]. Partner ecosystems extend reach but also introduce execution risk if partners underperform or client satisfaction wanes during indirect implementations.

Litigation risk stemming from the Appian trade secret dispute poses material uncertainty about potential damages or injunctions that could impact product development or sales strategy [S4], [S7]-[S10]. Nevertheless, Pegasystems maintains robust IP protections underpinning its moat plus an experienced senior leadership team spearheading strategic pivots towards SaaS/cloud models.

Growth Drivers and Constraints

Structural tailwinds underpinning Pegasystems include accelerating digital transformation mandates across industries requiring cloud migration, AI embedding within workflows, process modernization replacing legacy BPM systems, and customer experience personalization expansion powered by machine learning algorithms , [S14]. These trends favor Pega’s value proposition directly.

Near-term growth is particularly driven by expanding Pega Cloud subscriptions now accounting for nearly half the company’s quarterly revenues (~48%) [S2]. The firm’s ability to cross-sell cloud upgrades into installed base customers while winning net-new accounts hungry for agile SaaS delivery underpins recurring revenue expansion.

On the flip side:

- Legacy subscription licenses are declining sharply (-49%), indicating erosion of older licensing agreements possibly pressed by shifts to cloud adoption or competitor displacements.

- Consulting revenue contraction (-9%) risks slower client onboarding tempos especially where partner capacity cannot fully fill gaps.

- Legal uncertainties around trade secret litigation pose capital allocation distractions and potential cash outflows if judgments go against Pegasystems despite appeals ongoing through various courts including remands ordered after recent Supreme Court ruling [S5], [S7], [S9], [S10].

- Competitive pressures from hyperscale cloud vendors bundling automation tools into broader platforms continue ramping up.

- Maintaining security certifications (ISO/IEC 27001 & 22301) and resilient infrastructure is increasingly capital-intensive given rising demand volumes for Pega Cloud services [S1].

What To Watch Next

Key upcoming milestones include:

- The May 7, 2026 status conference for the remanded trade secret trial proceedings following Supreme Court actions will clarify timelines and potential court expectations regarding this material litigation risk [S10].

- Further quarterly results will reveal whether Pega can arrest subscription license declines while sustaining strong Pega Cloud growth critical for overall revenue recovery.

- Execution success of expanding partner-led implementations impacting consulting revenues directly affects service margins and client satisfaction metrics.

- Monitoring non-GAAP backlog (remaining performance obligations) growth comparison with constant-currency figures may provide leading indicators of contract health given FX impacts reported late last year (constant currency backlog grew ~14% YoY as of March’26) [S25].

- Management commentary on structural cost investments related to AI-first R&D intensification measured against operating leverage effects will show scaled innovation capability sustainability.

- Share repurchase program progress since Board extended authorization adding $1 billion available provides insight on capital allocation priorities versus litigation defense needs [S6], [S18].

Financial Profile Summary

Financially Pegasystems has demonstrated solid long-term improvement trends supported by digital transformation demand but recently faced some cyclical softness:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 393 | 505 | 263 | 15 | +296.7% |

| 2024 | 99 | 346 | 124 | 8 | +46.3% |

| 2023 | 68 | 218 | 81 | 17 | +119.6% |

| 2022 | -346 | 22 | -109 | 35 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 15 | 500 | 491 |

| 2024 | 10 | 68 | 338 |

| 2023 | 10 | 0 | 201 |

| 2022 | 10 | 26 | -13 |

Source: SEC companyfacts cache [F1]. *Annualized approximation based on trailing data including Q1'26 dynamics[F1]

Q1 2026 reported net income declined sharply YoY to $32.8M vs. $85.4M as restructuring costs increased alongside legal expenses related to ongoing litigation exposures reflecting risk premium provisions.[S2], [S14]

Operating cash flow remains strong at over $200 million annually with Capex modestly increased aligned with infrastructure investments supporting Pega Cloud expansion per disclosures shifting focus towards scalable internet delivery platforms.[F1],[S14]

Liquidity remains solid with cash/equivalents at ~$270 million as of March’26 supporting operational needs amid legal contingencies.[F1],[S12] Leverage is low with no significant borrowings drawn under revolving credit facilities.[F1],[S12]

The Board’s active share repurchase program authorized through June’27 announced earlier this year targets returning capital efficiently given free cash flow generation even while balancing litigation spend.[S18]

Conclusion

Pegasystems is navigating a transitional phase characterized by accelerating adoption of its AI-powered Pega Cloud offering contrasted by pronounced declines in older licensing models. Its core strategic strength lies in integrated workflow automation combined with real-time AI decisioning designed for complex enterprise applications addressing emerging digital transformation needs. However, near-term financial performance is tempered by reduced consulting involvement rates due partly to moves towards partner-enabled deployments plus material legal overhangs around trade secret disputes involving competitor Appian Corp., which remain unresolved after multiple appellate steps.

Investors should monitor developments around the May court status hearing as it sets direction on prolonged litigation exposure while also watching evolving top-line mix dynamics emphasizing SaaS/cloud booking acceleration relative to legacy product attrition. Execution effectiveness on partner expansion efforts will be critical to stabilizing services revenue outside subscription growth as Pega pushes further into an AI-first technology stack enabling scalable modernization solutions amid intensifying competition from mega-vendors moving downstream into BPM/CRM markets.

This analysis is based solely on publicly available information including SEC filings dated through April 21st, 2026 ([S1]-[S29]), company financial data ([F1]), and relevant market commentary ([N1]-[N14]). It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments