Triumph Financial Expands Integrated Trucking Finance Platform with Solid Q1 Execution

Triumph Financial’s latest quarterly update highlights steady revenue mix shifts and strategic acquisitions bolstering its niche in trucking financial services.

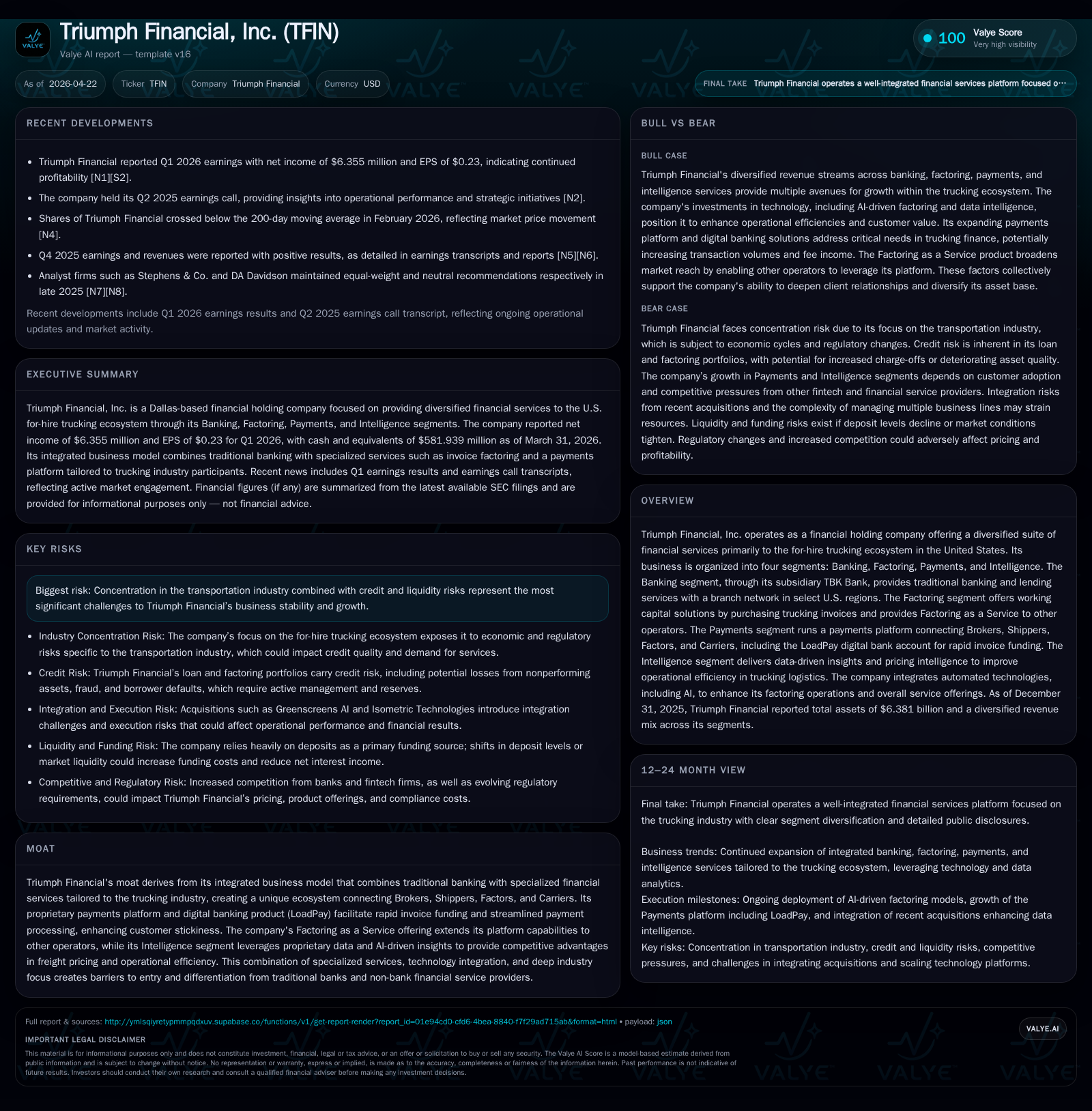

In early 2026, Triumph Financial, Inc. reinforced its position as a specialized financial ecosystem for the U.S. for-hire trucking industry by delivering stable quarter-over-quarter results and expanding its Intelligence segment through acquisition. The company’s integrated business model—comprising banking, factoring, payments, and data intelligence—supports differentiated service delivery across Brokers, Shippers, Factors, and Carriers. While industry concentration and credit risks remain key challenges, ongoing technological investment and unique payment and lending offerings underpin durable customer relationships and moderate growth prospects.

Recent Operating Update

Triumph Financial's latest quarterly filing (10-Q as of April 21, 2026) outlines a steady operating performance through Q1 2026. The company announced results that beat earnings expectations ([S2], [N1]) reflecting continued strength in its integrated model servicing the U.S. trucking ecosystem. Alongside organic growth drivers, Triumph completed an acquisition of Greenscreens AI earlier in 2025—a strategic addition enhancing its Intelligence segment with advanced freight market pricing analytics ([S1], [S21]).

Payments continue to grow as critical infrastructure linking Brokers, Shippers, Factors, and Carriers through their LoadPay digital platform provides rapid invoice funding—a material value add enabling working capital efficiency within the fragmented trucking sector ([S1], [N2]). The robust liquidity position (~$582 million cash & equivalents at March 31) supports ongoing investment in tech-driven services ([F1]).

Business Model

Triumph Financial monetizes its specialization in the for-hire trucking logistics industry through four distinct but integrated segments: Banking, Factoring, Payments, and Intelligence ([S1], [S8], [S10]).

Banking: TBK Bank offers traditional deposit-taking and commercial lending with regional branch networks concentrated in Colorado’s Front Range, Quad Cities area (Iowa/Illinois), and Dallas. Its commercial loans portfolio includes asset-based loans, mortgage warehouse lending nationwide, equipment financing, and liquid credit offerings. Deposits generated through community banking feed a low-cost funding base supporting loan originations ([S8], [S15]).

Factoring: Serving predominantly small to mid-sized trucking operators, Triumph purchases accounts receivable invoices at a discount to provide immediate liquidity—critical given typical payment lags of 30-60 days for carriers needing working capital. The company also offers "Factoring as a Service" allowing partners to leverage its platform capabilities for back-office support or full-service factoring ([S11], [S28]).

Payments: Its proprietary payments network digitally connects ecosystem participants for seamless freight invoice settlement workflows—ranging from audits to final carrier remittance. Fees derive from transaction volume charges plus interest income on factored receivables funded rapidly via LoadPay accounts ([S1], [S15]).

Intelligence: Launched in late 2024 following acquisitions like Isometric Technologies and Greenscreens AI, this division leverages data from payment flows combined with AI-driven algorithms to provide real-time pricing intelligence and operational analytics—aspects increasingly important in competitive freight marketplaces ([S10], [S21]).

This hybrid financial-technology ecosystem creates stickier client relationships by integrating capital provision with operational tools that are difficult for generalized banks or fintechs lacking industry-specific knowledge to replicate ([S16], [S24]).

Industry Structure & Competitive Position

Triumph operates at the intersection of traditional banking regulation (as a bank holding company) and rapidly evolving fintech-enabled logistics finance—the latter being a niche yet critical vertical within commercial finance.

Competition spans from large regional/national banks offering general purpose loans toward non-bank lenders focusing on commercial factoring or payment processing technology providers. However, Triumph's moat is anchored by:

- Deep specialization in trucking operations facilitating tailored products.

- An integrated platform combining lending/factoring with payments and data intelligence.

- Partnerships across different supply chain parties ensuring network effects.

- Use of AI-powered automation enhancing underwriting efficiency and decision-making.

Still, competitive pressures could emerge from better-capitalized incumbents or new entrants deploying alternative payment rails or disruptive pricing models ([S16], [S24]). There also exists an inherent risk from customers developing own-platform technologies potentially bypassing intermediaries like Triumph.

Growth Drivers & Constraints

Drivers:

- Rising demand for faster financing solutions amid tight cash flow cycles of trucking carriers.

- Expansion of Payments segment leveraging digital wallet innovations supporting rapid carrier pay.

- Adoption of Intelligence products augmenting customer profitability through market data analytics.

- Factoring volume growth supported by broadening Factoring as a Service partnerships extending platform reach.

- Cross-selling opportunities unlocking higher customer lifetime value within the ecosystem.

Constraints:

- Heavy concentration in trucking exposes revenue streams to cyclicality in freight volumes & spot rate swings influenced by macroeconomic factors.[S13],[S27]

- Credit risk heightened by industry bankruptcies like Tricolor Holdings’ default triggers collateral uncertainty impacting loss provisioning efforts.[S22]

- Regulatory compliance costs related to banking activities including anti-money laundering measures impose ongoing operating expenses.[S13]

- Competition pricing pressure may force fee erosion especially if higher-capital players intensify marketing incentives.[S16],[S24]

- Pace of technology integration & customer adoption determines returns on recent acquisitions fueling Intelligence segment.[S27]

What to Watch Next

Key milestones ahead for stakeholders tracking Triumph include:

- Quarterly updates on Payment transaction volumes signaling traction scaling digital invoicing among Brokers and Carriers.

- Progress on integrating Greenscreens AI product suite into the Intelligence offering with expanded market penetration metrics.

- Credit quality trends especially monitoring exposure risks linked to troubled transportation counterparties.

- Management commentary on margin trends amid competitive pricing pressures across products.

- Deposit growth versus lending expansion providing insight on funding cost trajectory.

- Any regulatory developments impacting banking or fintech regulations affecting product features or compliance costs.

Financial Profile

Supporting its operational narrative is a financial profile characterized by measured profitability gains alongside solid cash generation ability:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 25 | 67 | +57.6% |

| 2024 | 16 | 59 | -60.8% |

| 2023 | 41 | 43 | -59.8% |

| 2022 | 102 | 74 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | 2 | 2.7 |

| 2024 | 3 | 3 | 1.8 |

| 2023 | 3 | 82 | 4.8 |

| 2022 | 3 | 77 | 11.5 |

Source: SEC companyfacts cache [F1].

(Figures sourced from recent annual filings with SEC [F1])

The net income increase of +57.6% YoY (2024–25) partially reflects increased scale in Payments and Intelligence revenues while maintaining prudent loss management within credit portfolios ([N1], [S2]). Operating cash flow remains robust relative to net income highlighting consistent high-quality earnings supporting dividends on preferred stock series ([S20]) and maintained share repurchase activity albeit at reduced levels post major buybacks in prior years.

However, ROE remains modest (~2.7%) indicating room for enhanced capital efficiency amid growth investments ([F1]). Liquidity is ample with cash balances nearing $582 million at quarter-end reflecting strong operational cash generation capacity supportive of ongoing platform investments ([F1],[S2]).

This analysis abstracts from specific investment recommendations but aims to contextualize Triumph’s continuing evolution within the competitive niche of transportation-focused commercial finance augmented by fintech innovation—an interplay shaping its medium-term trajectory amidst sectoral cyclicality risks.

Disclaimer: This report is an analytical summary based strictly on publicly available SEC filings dated up to April 21, 2026 () supplemented by reputable news sources () without speculative assumptions beyond disclosed facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments