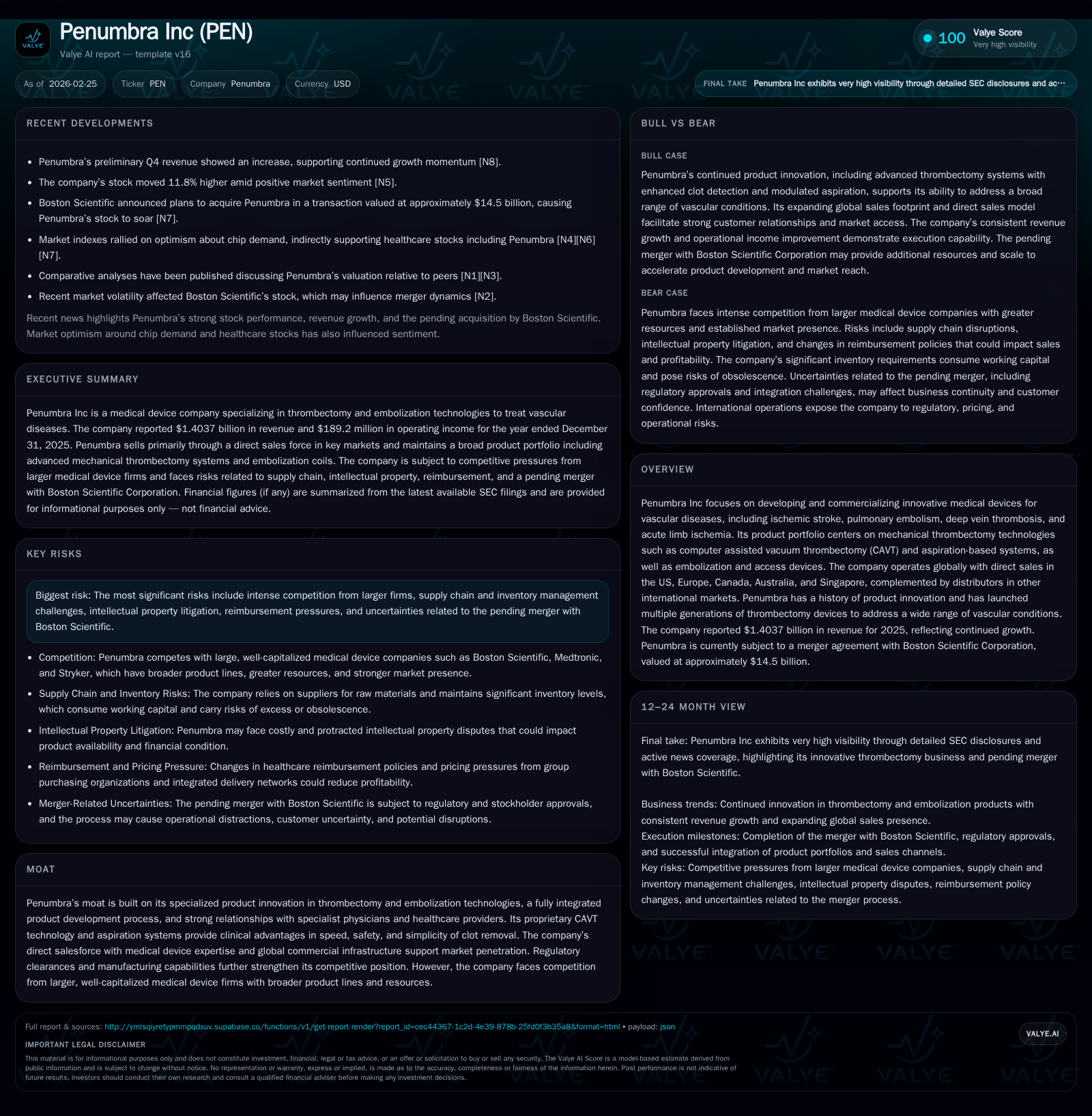

Penumbra Inc’s Thrombectomy Innovation Fuels Revenue Growth Amid Boston Scientific Merger Uncertainties

Penumbra has demonstrated strong financial momentum driven by product innovation in thrombectomy devices but faces strategic and regulatory risks amid its acquisition by Boston Scientific.

Penumbra Inc has achieved notable top-line growth over recent years primarily through its specialized thrombectomy and embolization medical devices. The company reported revenues of $1.4 billion in 2025, representing a 17.5% increase year-over-year, supported by robust sales of its aspiration and computer assisted vacuum thrombectomy technologies. However, profitability experienced volatility due to a strategic business exit and merger-related distractions. Penumbra’s ongoing merger with Boston Scientific introduces both synergies potential and substantial execution risk in operational continuity, talent retention, and customer relationships. Regulatory complexities and competitive pressures from larger industry players remain structural challenges.

Company Overview

Penumbra Inc focuses on designing and commercializing innovative medical devices targeted predominantly at vascular conditions such as ischemic stroke, pulmonary embolism, deep vein thrombosis, and acute limb ischemia. Its core technologies center on mechanical thrombectomy—removal of blood clots using aspiration-based systems and their proprietary computer assisted vacuum thrombectomy (CAVT) technology. Penumbra complements these with embolization products and access devices used mainly by specialist physicians including interventional radiologists, neurologists, neurosurgeons, vascular surgeons, and cardiologists across multiple regions globally including the U.S., Europe, Canada, Australia, Singapore, plus international distributors.

Historical Performance and Growth Drivers

From FY2022 to FY2025 Penumbra exhibited rapid revenue growth:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1404 | 178 | 239 | 189 | +17.5% | +1168.1% |

| 2024 | 1195 | 14 | 168 | 9 | +319.6% | -74.2% |

| 2023 | 285 | 54 | 97 | 74 | +28.7% | +1298.5% |

| 2022 | 221 | 4 | -56 | 6 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 175 | 12.4 |

| 2024 | 100 | 147 | 1.2 |

| 2023 | 82 | ||

| 2022 | -75 |

Source: SEC companyfacts cache [F1].

[Note: The large jump in revenues between FY2023 to FY2024 reflects changes not detailed here such as reporting scope or acquisitions.] [F1]

Growth has been driven by aggressive investment in next-generation thrombectomy products that offer clinical advantages such as faster clot removal with improved safety profiles. Their proprietary CAVT technology distinguishes them by addressing speed and simplicity of use which appeals strongly to treating physicians. Penumbra has expanded its global footprint through direct sales teams while managing distributor partnerships especially in China via licensing agreements allowing local manufacturing—a strategy aimed at mitigating regulatory risk and capturing emerging market share.

However, growth was punctuated by a strategic portfolio adjustment during FY2024 involving exit from an immersive healthcare business segment resulting in substantial impairments ($115 million), temporarily weighing on operating results [S1].

Future Growth Prospects & Milestones

Looking ahead, Penumbra aims to sustain momentum through iterative innovation on existing platforms alongside clinical trials designed to support regulatory submissions for new indications or product extensions. Key opportunities include:

- Continued expansion of thrombectomy procedures worldwide driven by aging demographics.

- Broadening product applications beyond current indications such as acute limb ischemia.

- Leveraging synergies from integration with Boston Scientific for broader distribution channels and complementary technologies.

- Strengthening presence in international markets via licensing partnerships.

Critical milestones will include regulatory clearances for next-generation devices and expanded indications which can materially influence adoption rates. Progress on the Boston Scientific merger approvals is also pivotal for future operational strategy.

Challenges constraining growth encompass intense competition from larger firms with broader portfolios capable of bundled offerings; regulatory hurdles including increasingly stringent global standards; possible loss of key personnel or customers amid merger uncertainties; and pricing pressures within hospital procurement driven by group purchasing organizations tightening cost controls [S21][S4].

Financial Returns & Capital Allocation

Penumbra demonstrates solid financial health with improving profitability metrics:

- Operating cash flow rose steadily from negative $56 million in FY2022 to $239 million in FY2025.

- Capital expenditures increased significantly in FY2025 ($63.7 million vs $21.2 million prior year), reflecting investments in manufacturing capabilities or infrastructure expansion.

- Free cash flow approximated $175 million in FY2025 after capex deductions [F1].

- Approximate return on equity was about 12.4%, indicating effective capital utilization.

No dividends were paid during this period nor were any stock repurchases executed in FY2025 due to merger-related restrictions; however, $100 million was spent on buybacks in FY2024 prior to intensified merger activities [F1][S1].

These figures indicate an operational emphasis on reinvestment ahead of strategic transition rather than shareholder returns through dividends or buybacks at this stage.

Strategic Merger & Associated Risks

In January 2026 Penumbra agreed to be acquired by Boston Scientific Corporation at approximately $374 per share with transaction consideration split roughly as 73% cash /27% stock after proration. The transaction promises synergy realization but also introduces significant uncertainty including:

- Potential disruptions affecting customer purchase decisions due to merger-related distractions or uncertainty.

- Risk of attrition among key employees undermining innovation pipeline or sales effectiveness.

- Restrictions imposed by merger covenants limiting business development activities until closing.

- Regulatory approvals required from antitrust authorities that may delay or prevent completion exposing Penumbra’s stock price to downside if deal fails [N2][S1][S11].

Management acknowledges that transaction-related costs are accruing while operational focus is divided which could adversely affect near-term financial results [S3]. Litigation risks related to shareholder lawsuits accompanying such corporate transactions could consume additional resources.

Competitive Landscape & Industry Dynamics

Penumbra competes with major incumbents including Boston Scientific itself along with Medtronic, Stryker (recently acquiring Inari Medical), Terumo plus smaller niche players competing regionally or by procedure type. Competitors benefit from larger R&D budgets enabling faster innovation cycles; broader sales forces offering bundled solutions increasing switching costs; established relations with group purchasing organizations influencing hospital buying heavily.

Penumbra’s competitive edge lies in its distinctive CAVT technology combined with an agile development culture emphasizing speed-to-market backed by strong physician collaboration networks [S21]. Maintaining this technological moat while navigating reimbursement shifts towards cost-effectiveness remains vital.

Operational & Regulatory Risks

Penumbra operates under stringent FDA oversight supplemented by foreign regulatory regimes requiring premarket clearances followed by post-market surveillance subjecting them to inspections periodically. Non-compliance risks suspension or recall harming reputation.[S4][S10] Product liability exposure inherent due to invasive device nature presents litigation risks which could adversely affect financials.[S6][S17] Global compliance demands add complexity especially under evolving frameworks like EU MDR increasing evidence requirements.[S25] Intellectual property challenges persist given uncertain patent enforcement internationally posing litigation threats both defensively and offensively.[S8][S16][S18] Pricing pressures arise from healthcare cost containment strategies including group purchasing organization negotiations shifting competition beyond differentiation into discount arenas.[S22] Legal compliance under anti-kickback statutes requires constant vigilance given jurisdictional variances raising complexity.[S13][S20]

Conclusion & Monitoring Points

Penumbra has scaled its specialized vascular portfolio translating into solid revenue growth accompanied by improved cash generation despite restructuring costs linked to exited businesses. Its core competency centers on advanced aspiration thrombectomy platforms favored clinically for speed and safety. The imminent Boston Scientific acquisition offers substantial opportunity via complementary line-building but elevates execution risk amid operational distractions plus regulatory/legal hurdles which should be closely monitored through deal approval timelines along with integration progress post-close. Investors should track:

- Regulatory milestones for next-generation device approvals including any delays;

- Updates on Boston Scientific merger approval process;

- Signs of attrition among senior technical/commercial staff;

- Quarterly financials highlighting margin trends post-distraction;

- Competitive moves from larger incumbents expanding thrombectomy portfolios; Given complex industry dynamics shaped around innovation cadence combined with regulatory complexity plus payer pricing constraints Penumbra remains technologically well positioned but must navigate multifaceted risks carefully going forward.

This analysis is based solely on publicly available information as of February 25, 2026. It does not constitute investment advice nor recommendations regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments