Phathom Pharmaceuticals' Revenue Surge Reflects Shifts in Pipeline and Market Dynamics

Strong topline gains in 2025 underscore Phathom's advancing clinical assets amid persistent net losses and strategic capital raises.

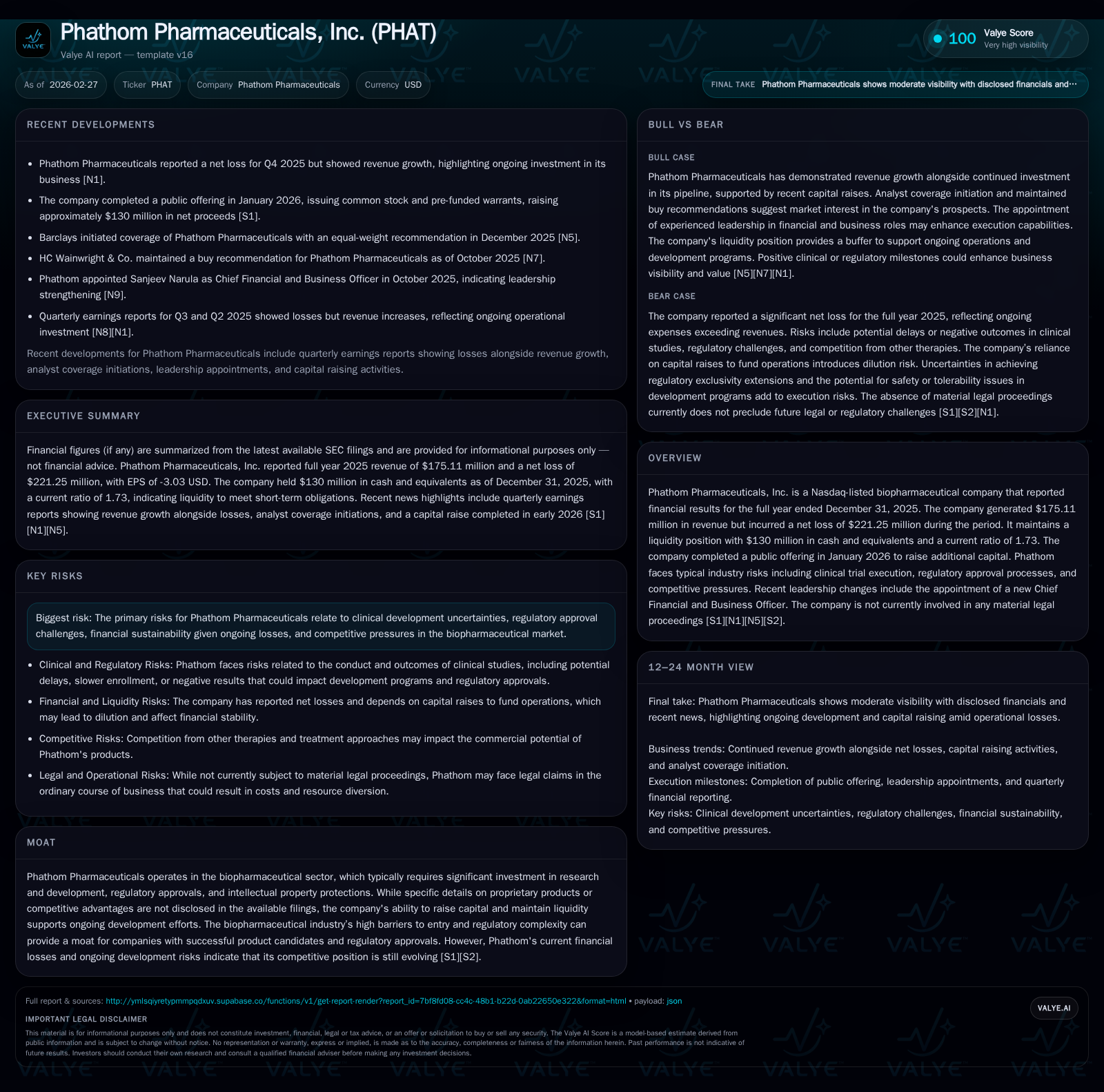

Phathom Pharmaceuticals posted a remarkable 216.9% revenue increase in 2025 driven by pipeline maturation and commercialization progress, yet the company remains unprofitable with a sizable net loss of $221 million. Operational improvements have narrowed losses, reflecting some efficiency gains amidst sustained R&D investment. A January 2026 equity offering bolstered liquidity to $130 million, extending the runway for ongoing development, notably in eosinophilic esophagitis and GERD indications. Leadership changes signal strategic recalibrations as the firm navigates clinical risks and regulatory hurdles typical of the biopharma sector.

Strong Revenue Growth Signals Pipeline Momentum

Phathom Pharmaceuticals experienced a dramatic acceleration in revenue during fiscal year 2025, reaching $175.11 million from a relatively modest $55.25 million recorded in 2024—a massive increase of approximately 217% year-over-year [F1]. This surge aligns closely with the company's progression from primarily development-stage activities toward commercialization phases for its lead product VOQUEZNA (vonoprazan). The growth trajectory reflects successful late-stage clinical advancements, particularly around gastroesophageal reflux disease (GERD) indications where VOQUEZNA has demonstrated differentiated efficacy against nocturnal symptoms that affect an estimated majority of GERD patients [N1][S25][S26].

The transition of biopharmaceutical products through regulatory milestones into market launch stages typically results in step-function revenue uplifts due to initial sales intake combined with expanded patient access. Phathom’s FY2025 leap is consistent with this pattern, though the company remains early in its commercialization curve.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 175 | -221 | -167 | -160 | +216.9% | +33.8% |

| 2024 | 55 | -334 | -267 | -277 | +8001.5% | -65.8% |

| 2023 | 1 | -202 | -138 | -167 | -2.0% | |

| 2022 | -198 | -147 | -172 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -167 | 50.5 |

| 2024 | -267 | 131.8 |

| 2023 | -139 | 277.1 |

| 2022 | -148 | 264.3 |

Source: SEC companyfacts cache [F1].

Evolving Earnings and Loss Dynamics: Decoding Operating Performance

Despite significant top-line growth, Phathom continues to operate at a loss reflective of ongoing high expenditures associated with clinical development programs and commercial infrastructure buildout. Operating income improved markedly by over 42% year-over-year to a loss of approximately $160 million in FY2025 compared to a much larger operating deficit of $277 million in FY2024 [F1]. The net loss similarly reduced by roughly one-third to -$221 million.

This improvement suggests that while absolute spending remains substantial, efficiencies or milestone-driven progress are beginning to moderate the burn rate relative to growing revenues. The passage from expansive R&D outlay toward incremental operational leverage—typical for biopharma transitioning firms—is evident here.

| FY | Operating Income (USD) | OpInc YoY % | Net Income (USD) | Net YoY % |

|---|---|---|---|---|

| 2025 | -159,986,000 | +42.3% | -221,247,000 | +33.8% |

| 2024 | -277,467,000 | -334,326,000 |

Liquidity Position and Capital Markets Activity Support Growth Initiatives

Maintaining robust liquidity is critical for companies like Phathom that depend heavily on sustained funding for multiple clinical trials and commercial investment simultaneously. At year-end 2025, Phathom reported cash and equivalents of approximately $130 million alongside a current ratio of 1.73 — signaling ample near-term financial stability relative to short-term obligations [F1].

This liquidity was materially boosted through a public equity offering completed in January 2026 raising net proceeds close to $130 million before expenses [S8][S13][N1]. Such capital injections extend operational runway beyond typical venture-backed horizons that focus narrowly on trial readouts alone.

The use of pre-funded warrants alongside common stock issuance allowed Phathom flexibility towards ownership structure management while securing non-dilutive capital from key investors.

Leadership Changes and Strategic Direction Insights

Recent leadership appointments have introduced seasoned executive expertise aimed at refining Phathom’s financial stewardship amid its evolving commercial footprint [S1]. The new Chief Financial and Business Officer brings anticipated shifts towards disciplined capital deployment balanced against aggressive clinical timelines.

Management turnover at senior levels often correlates with evolution from pure research-led operations into commercially oriented biopharmaceutical enterprises focused on scalable revenue generation and shareholder value creation.

Industry Risks and Regulatory Environment Impacting Development

Phathom operates within an industry characterized by extraordinary clinical development risks including enrollment challenges and unpredictable trial outcomes that can sharply affect valuation trajectories [S4][S6]. Regulatory pathways involving FDA approvals remain complex—any delay or negative verdict could derail near-term plans.

The competitive landscape also features multiple biologics and small molecules targeting similar gastrointestinal conditions complicating market share capture post-approval. In addition, sustaining financial sustainability amid persistent cash burn places pressure on capital management strategies.

What to Watch: Milestones, Clinical Trials, and Market Entry

A key upcoming inflection point will be the topline results expected from the Phase 2 pHalcon-EoE-201 trial testing VOQUEZNA as an investigational therapy for eosinophilic esophagitis (EoE)—anticipated during calendar year 2027 [N1][S24]. Positive outcomes may enable label expansion opportunities accompanied by potential regulatory exclusivity extensions via pediatric program discussions.

Furthermore, ongoing readouts from expanded real-world experience data around nocturnal GERD symptomatic relief could strengthen VOQUEZNA’s market positioning versus conventional proton pump inhibitors.

Monitoring timing for subsequent pivotal trials or submission filings will be critical signals regarding trajectory toward broader market penetration.

Capital Allocation Strategies Underpinning Future Sustainability

Operating cash flow remained deeply negative at approximately -$166.8 million in FY2025 despite operational improvements seen elsewhere [F1]. Capital expenditures were minimal ($229k), reflecting typical asset-light biopharma models focused more on intangible R&D investment than fixed assets.

Phathom’s sizable negative equity position (-$438 million) further accentuates reliance on external financing sources versus internal free cash generation at this stage [F1]. No dividends or share repurchases were recorded as all available funds prioritize pipeline advancement and commercial capability establishment [S16].

Disclaimer: This report is prepared solely for informational purposes without any investment recommendation or advice. Data presented reflect information available as of February 27, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments