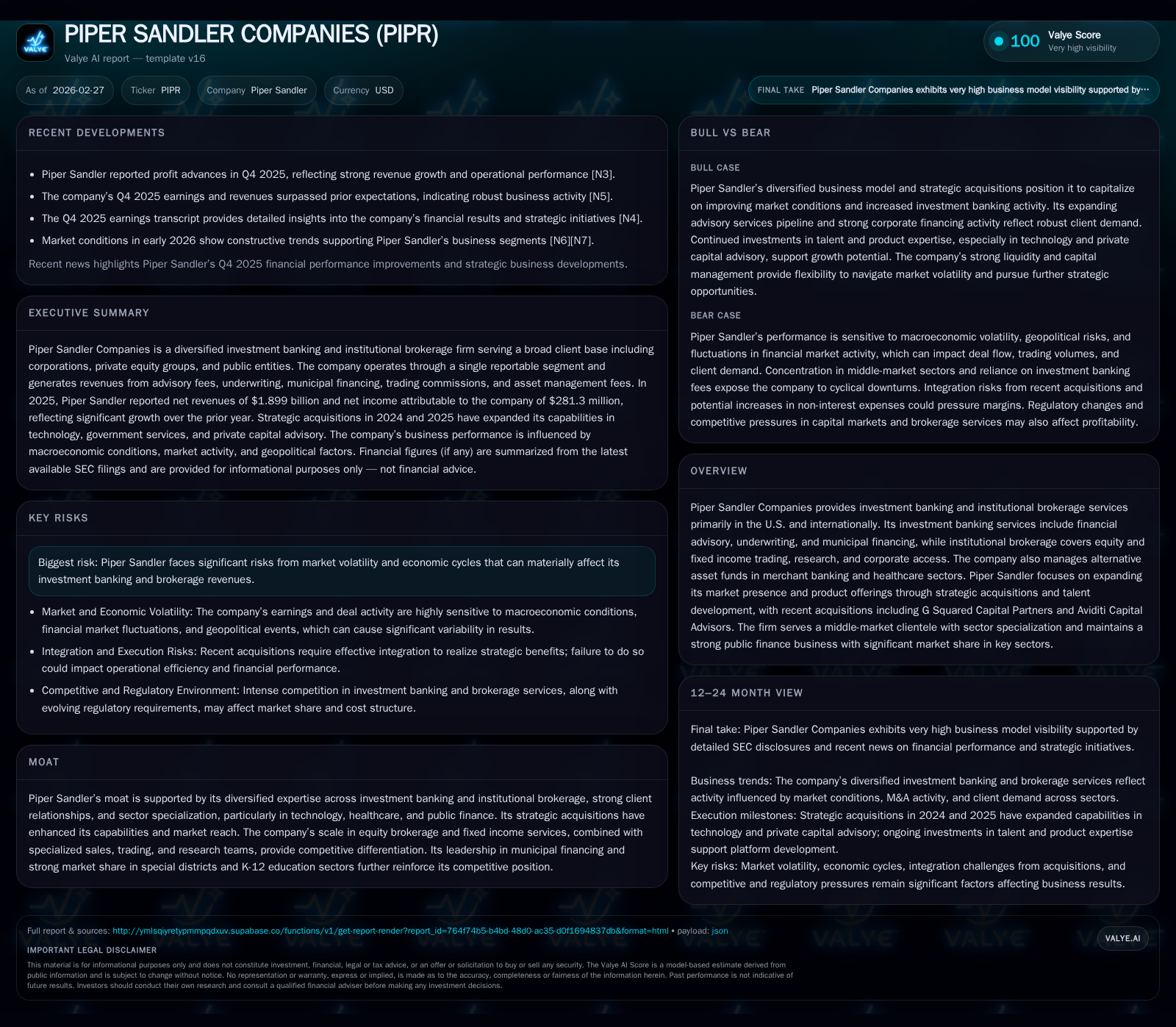

Piper Sandler’s Strategic Ascent: Revenue Vigor Meets Capital Discipline

Robust 2025 growth propelled by acquisitions and sector focus complements prudent capital management.

Piper Sandler Companies delivered a striking revenue surge of 37.4% in FY2025, underscored by strategic acquisitions and deepening sector specialization in technology, healthcare, and public finance. Combined investment banking and institutional brokerage activities rebounded with notable expansion in advisory services and municipal financing amid favorable market dynamics. Concurrently, the firm balanced aggressive growth with disciplined capital deployment, generating strong operating cash flow and maintaining an approximate 8.3% ROE amid increased dividends and share repurchases. The outlook remains cautiously optimistic given geopolitical risks and monetary policy shifts, with key metrics around deal pipeline, brokerage volumes, and integration success to watch in 2026.

Transforming Growth Trajectory: Historical Financial Performance Review

Piper Sandler demonstrated a remarkable acceleration in financial performance throughout FY2025, underpinning its strategic ascent within the midmarket investment banking landscape. Annual revenue grew sharply to $666.99 million from $485.38 million in FY2024, marking a sizable 37.4% year-over-year increase that reflects both robust deal activity and broadened product scope across advisory, corporate financing, and institutional brokerage lines [F1].

Net income mirrored this upward momentum, soaring to $113.97 million (+65%), representing the company's capacity to translate top-line vigor into bottom-line profitability through effective expense control despite increased headcount costs associated with expansion initiatives. Operating cash flow surged to nearly $587 million (+87.3%), indicating strong cash conversion from earnings underpinned by efficient working capital management and steady capital expenditures estimated near $6 million per annum — effectively sustaining liquidity while investing selectively in growth areas [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 667 | 114 | 587 | +37.4% | +65.0% |

| 2024 | 485 | 69 | 313 | +2.4% | +32.7% |

| 2023 | 474 | 52 | 276 | +20.6% | +36.5% |

| 2022 | 393 | 38 | -225 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 114 | 125 | 8.3 |

| 2024 | 74 | 66 | 5.6 |

| 2023 | 84 | 71 | 4.8 |

| 2022 | 108 | 187 | 3.6 |

Source: SEC companyfacts cache [F1].

Note: Capex data limited to historical range prior to FY2014; recent expenditure estimates derived from narrative disclosures.

Drivers Behind the 2025 Revenue and Profit Surge

The strong performance in fiscal year 2025 was buoyed primarily by a more constructive market environment featuring rebounding equity valuations, reduced volatility levels, and increased investor appetite across sectors crucial to Piper Sandler’s middle-market focus. Corporate financing revenues rose by approximately 24.9%, supported by an active debt capital markets advisory team and increased equity financings driven notably by healthcare transactions where Piper Sandler acted as book runner on the vast majority of completed deals (37 out of 38) — cementing its stature within this high-growth sector segment [S6], [N1].

Municipal financing also gained traction, recording a healthy increase of about 19%, attributed largely to elevated municipal negotiated issuance volumes fueled by infrastructure funding needs coupled with robust investor demand for tax-exempt instruments targeted at special districts alongside K-12 education financings where Piper Sandler holds top-tier market rankings nationally [S9], [S13].

Institutional brokerage revenue rose roughly 7.9%, reflecting client engagement intensification across both equity brokerage (+7%) and fixed income services (+9%). The fixed income elevation was partly precipitated by activity from depository clients undergoing balance sheet repositioning amid an improving interest rate outlook post-Fed rate cuts during late-2025, complemented by augmented presence among asset management firms servicing public entities and healthcare industries [S6], [S13].

Leveraging Sector Specialization and Strategic Acquisitions

Piper Sandler reinforced its competitive moat through thoughtful bolt-on acquisitions geared towards broadening expertise within high-value sub-sectors aligned with its client-centric platform ethos. Foremost among these was the September 2025 acquisition of G Squared Capital Partners LLC — a boutique bank focused on government services and defense technology — which synergized with Piper’s existing technology sector verticals enabling enhanced advisory depth and access in both public-sector tech domains as well as related private equity clientele bases [S1], [S9].

Earlier acquisitions such as August 2024's Aviditi Capital Advisors have allowed Piper Sandler to fortify its private capital advisory capabilities by providing end-to-end coverage for financial sponsors including global alternative managers, thereby complementing existing merchant banking ventures especially in healthcare-focused alternative asset funds management where the firm records recurring management and performance fees alongside realized investment gains/losses [S1], [S9].

Integration efforts accompanied these deals including targeted hiring of seasoned managing directors augmenting thematic sector coverage framing Piper Sandler’s boutique approach which blends scale benefits with nimble specialized advisory capacity — critical for addressing nuanced midmarket deals in government services or restructuring mandates frequently accessed via debt capital markets advisory teams [S5], [N1].

Institutional Brokerage and Investment Banking: Diversified Revenue Engines

Operating under a comprehensive one-reportable-segment model allowing cross-platform collaboration, Piper Sandler generates revenues spanning investment banking fees (advisory plus underwriting & municipal finance), institutional sales commissions, trading profits, research fees, corporate access offerings as well as alternative asset fund incomes encompassing management/performance fees plus realized gains.

In FY2025, total investment banking revenue registered approximately $1.40 billion on an adjusted basis per SEC reporting, expanding nearly 27% year over year primarily due to a blend of higher transaction counts (250+ M&A transactions closed vs prior year) plus average fee increases facilitated through enhanced sector depth across financial services, healthcare, industrials, and tech sectors [S6], [S14].

Institutional brokerage revenues totaled over $433 million (+7.9%), underpinned by strength in equity execution capabilities complemented by rising fixed income commissions—where structured products sales teams helped broaden product penetration—while research offerings fortified recurring client fee bases enabling stable revenue streams beyond transactional spikes typical of underwriting cycles [S6], [S14].

The firm's public finance unit showcased specialized prowess achieving second place nationally in K-12 education deal count/value while commanding over half market share within its special districts territories—an accomplishment supported through local relationship cultivation and acute municipal negotiated issuance expertise ensuring capital raises matched issuer objectives amidst evolving rate landscapes despite regulatory shifts[S9], [S13], confirming itself as a go-to advisor on complex negotiated deals.

Looking Ahead: Growth Prospects in a Constructive Yet Uncertain Environment

The macro backdrop entering calendar year 2026 projects cautiously optimistic prospects marked by moderating interest rate reductions staged by the Federal Reserve following multiple cuts aggregating around -75 basis points through late-2025 alongside signs of easing regulatory constraints that had previously clouded market certainty for IPOs and follow-on equities issuance timing [S7], [N3]. Nonetheless geopolitical flashpoints spanning Middle East tensions, European instability related to Eastern Europe conflicts, Taiwan concerns alongside ongoing U.S.-China trade disputes sustain elevated uncertainty impacting cross-border deal flows and equity sentiment.

Piper Sandler's sector diversification affords some mitigation against concentrated downturns—technology advisory mandates balanced against steady demand for healthcare financings plus resilient municipal negotiation issuances help preserve revenue breadth—but vigilant monitoring is warranted given cyclical sensitivities inherent in corporate financing cycles paired with fluctuating institutional trading volumes contingent on volatility regimes.

Strategic geographic expansion particularly into European markets is flagged as a key runway with scaling operations anticipated gradually as regulatory frameworks align permitting deeper client penetration on private capital advisory frontiers bolstered by recent acquisition integrations completed successfully during FY2025.

Capital Deployment Strategy: Balancing Returns and Liquidity

Complementing its growth trajectory is Piper Sandler’s disciplined approach towards capital stewardship manifest in elevated shareholder returns coupled with robust liquidity buffers suitable for weathering episodic volatility phases common within capital markets businesses.

In FY2025, dividends escalated materially reaching $114 million while share repurchases totaled approximately $125 million cumulatively exceeding prior years’ distributions reflecting confidence enabled by substantial free cash generation—a direct derivative of soaring operating cash flow nearly doubling from prior year levels at around $587 million against steady capex outlays estimated near $6 million underscoring conservative reinvestment philosophy aligned with operating leverage exploitation [F1], [S24].

An approximate return on equity calculated at around 8.3% signals reasonable profitability relative to shareholders’ equity base, while pre-tax margin improvement from roughly 14% up to near-20% demonstrates expense discipline partially linked to lowered compensation ratios despite workforce expansions required for executing sector-focused strategies leveraging acquisition-derived talent pools polyglot across diverse product sets such as debt restructuring advisory or structured product sales teams deployed institutionally[S14], [S11].

This balancing act preserves strategic flexibility facilitating opportunistic future investments or selective bolt-ons without jeopardizing ongoing liquidity safeguards necessary amidst unpredictable external shocks highlighted extensively within risk frameworks covering market volatility risk exposures typical of investment banking cycles[S22].

Key Metrics to Monitor for 2026 Performance

For stakeholders tracking Piper Sandler’s forward progress during fiscal year 2026 several metrics warrant focused observation:

- Advisory Pipeline & Completed M&A Transactions: Maintaining or growing completed transaction tallies above FY2025’s precedent (~250+ deals) will evidence sustained momentum despite external headwinds.

- Corporate Financing Activity: Monitoring book-run positions especially within technology/healthcare sectors for both equity/debt offerings provides insight into fee pool capture amid evolving valuations.

- Municipal Negotiated Issuance Volumes: Continued leadership or stable par value capture across special districts/K-12 sectors indicating durable local issuer relationships.

- Institutional Brokerage Volume & Margins: Changes in trade execution volume combined with spreads on inventory positions reflect responsiveness to changing market liquidity environments.

- Integration Costs & Deal-Related Expenses: Assess comparing restructuring/integration charges vis-à-vis incremental revenue from acquisitions inclusively measures acquisition synergies versus short-term cost burdens as part of sustainable margin trajectories.[N4], [N3]

Altogether these data points form a mosaic illustrating business resilience coupled with growth execution precision within a dynamic macro-financial landscape.

This analysis summarizes the financial condition and operational highlights of Piper Sandler Companies based on publicly available SEC filings ([F1],[S#]) and recent earnings calls ([N#]). It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments