Paramount Skydance Corp Confronts Integration and Competitive Challenges While Pushing for Streaming and Content Expansion

The 2025 consolidation of Paramount Global and Skydance under one corporate umbrella presents both significant growth opportunities and operational risks as the newly combined entity maneuvers in a fiercely competitive media landscape.

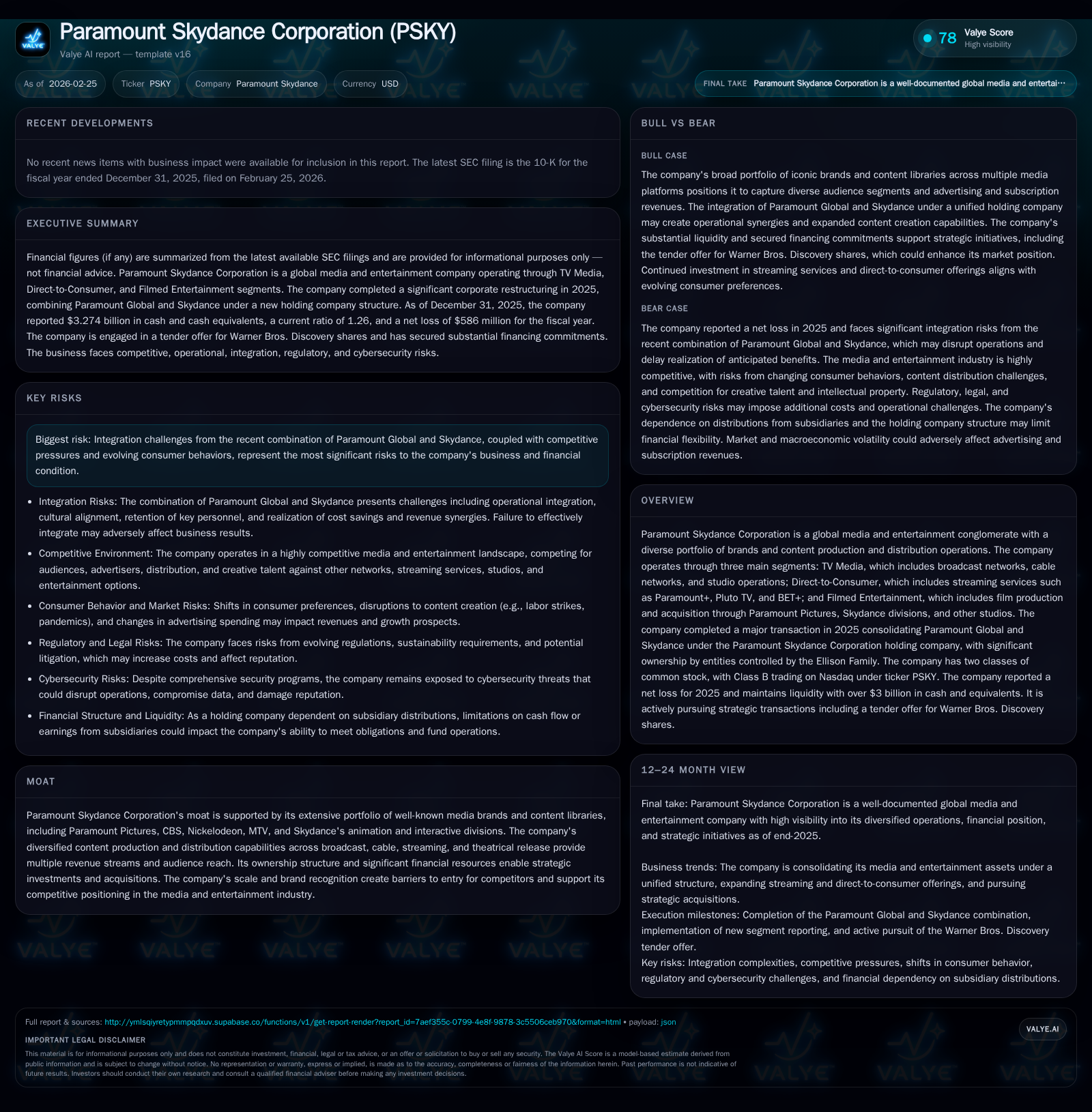

Paramount Skydance Corporation, established through the 2025 merger of Paramount Global and Skydance, operates across TV Media, Direct-to-Consumer streaming, and Filmed Entertainment segments. Despite robust brand assets and diversified content channels, the company reported net losses in fiscal 2025 amid heavy investments in streaming and content production. Paramount Skydance is actively pursuing a major acquisition of Warner Bros., signaling ambitions to expand market presence. Key risks include integration complexities, fierce competition in streaming and advertising markets, and evolving consumer behaviors that pressure traditional revenue sources.

Historical Performance: Growth Through Consolidation Amid Operating Losses

Paramount Skydance Corporation was formed through the consolidation of Paramount Global's assets with Skydance Media's diversified entertainment operations in August 2025. This combination brought together a wide portfolio of iconic media brands spanning broadcast (CBS), cable (MTV, Nickelodeon), streaming (Paramount+, Pluto TV), film production (Paramount Pictures), interactive gaming, animation, and scripted series production via Skydance. The strategic rationale centered on leveraging scale across multiple distribution platforms to compete more effectively within an increasingly crowded global entertainment marketplace [S1][S8][S13][F1].

Despite the high-profile merger bolstering its brand cachet and content library depth, Paramount Skydance posted an operating loss of $95 million for fiscal year 2025. More significantly, it recorded a net loss of $586 million due primarily to investments in scaling streaming services, restructuring costs associated with integrating two large media entities, and elevated content production expenses [F1]. However, the company generated positive operating cash flow of approximately $485 million while spending $162 million on capital expenditures, resulting in healthy free cash flow near $323 million [F1]. This cash flow positivity hints at operational stability underlying strategic growth initiatives into direct-to-consumer platforms.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures were not explicitly provided; focus is on profitability metrics from latest filings.

Current Business Segments: Multi-Platform Reach Balances Opportunity with Execution Risk

Paramount Skydance operates through three major reporting units: TV Media; Direct-to-Consumer; and Studios—this last newly consolidated to unify filmed entertainment with TV studio operations starting Q1 2026 [S27].

TV Media comprises domestic broadcast networks like CBS Television Network, domestic cable offerings including MTV and Nickelodeon brands, premium channels such as Showtime bundled with Paramount+, as well as international network extensions. Revenues stem largely from advertising sales across these channels as well as affiliate fees from distributors.

Direct-to-Consumer encompasses flagship subscription streaming services including Paramount+, ad-supported Pluto TV, BET+ among others. These services represent Paramount Skydance’s thrust into global streaming competition against Netflix, Disney+, Amazon Prime Video, among others.

Studios integrates film production including theatrical releases under Paramount Pictures plus television studio content creation centralized from prior segregated operating structures.

The multi-segment structure provides diverse revenue streams but also complexity around capital allocation priorities particularly given intensifying competition forcing increased content spend to satiate subscriber demand while defending legacy advertising revenue pools that have experienced declines due to audience fragmentation [S13][S21][S24].

Drivers of Future Growth: Content Investment and Strategic M&A Ambitions

Streaming drives the business outlook though with important caveats. Paramount Skydance acknowledges that profitable scaling depends heavily on consistently delivering differentiated original content attractive at scale globally and achieving sufficient subscriber penetration to leverage fixed cost structures [S1][S7]. Growth hinges on:

- Sustained investment in original scripted programs, films, sports rights acquisitions, which are intensive but essential to user retention.

- Effective windowing strategies balancing theatrical releases with timely streaming availability for maximizing total franchise value.

- Strategic partnerships or bundles advancing reach via third-party distributors or emerging MVPD hybrid models.

- Expansion into international markets where incremental subscriber growth can compound long-term value.

However, execution risk remains high amid evolving consumer preferences that pressure traditional linear TV ratings and advertisement volumes while increasing competition from both established media conglomerates and tech-driven disruptors deploying AI-enhanced production methods [S6][S10].

In addition to organic growth initiatives, Paramount Skydance’s recent increased takeover bid for Warner Bros.—backed by $57.5 billion in committed debt financing plus $46.6 billion equity funding from Ellison family-controlled entities—signals bold ambitions to amplify content ownership scale quickly through transformative acquisition [N4][N5][N6][S1]. This transaction remains subject to regulatory approvals with termination fees scaled according to timing failures or regulatory setbacks [S1]. Approval would potentially create one of the largest combined entities competing directly against Netflix’s global footprint.

Operating Forecasts & What to Monitor

Explicit guidance was not detailed in current SEC disclosures; however investors should track key upcoming milestones:

- The expiry date for Warner Bros.’ tender offer set for March 2, 2026.

- Regulatory reviews concerning antitrust or market concentration implications impacting deal closure probabilities.

- Post-merger integration updates affecting synergy realization timelines given challenges noted around legacy system consolidation.

- Quarterly subscriber count trends across Paramount+ suite compared against peer services.

- Advertising revenue performance amid shifting digital measurement methodologies pending industry-wide standardization efforts.

Staying alert to announcements regarding changes in content licensing deals or new strategic partnerships will also be critical as they directly affect monetization avenues.

Capital Allocation & Returns:

While Paramount Skydance generates free cash flow supporting internal needs, profitability metrics underscore current balance sheet pressures stemming largely from integration expenses and competitive pricing dynamics. The company paid out dividends totaling approximately $90 million during fiscal year 2025 while share repurchases were not noted as active during this period [F1][S28].

With equity exceeding $11.6 billion yet a net loss recorded last year leading to an estimated negative ROE near -5%, the firm appears focused on reinvestment over return maximization presently—a reasonable posture given its scale transformation objectives [F1]. Liquidity remains robust with over $3.2 billion cash reserves against current liabilities around $10.6 billion indicating capacity to meet near-term obligations despite sizable balance sheet leverage [F1][S23].

Risks Spotlight: Integration Complexity & Market Pressures

Key risks elaborated extensively include:

- Operational risks tied to melding disparate corporate cultures, IT systems integration challenges compounded by litigation resulting from the transactions’ consolidation process [S12][S26].

- Competitive threats intensified by rivals with deeper financial resources or superior technology infrastructure applying AI/ML tools for rapid content iteration or enhanced personalized user experience delivery [S6][S10].

- Consumer behavioral volatility prompted by emergent entertainment options fragmenting audiences away from traditional networks impacting affiliate fees & advertising income streams [S1][S21][S24].

- Regulatory uncertainties surrounding major mergers amplifying potential costs or deal delays beyond pre-agreed termination penalties [S1][N4][N5].

- Privacy law compliance demands adding operational burden especially concerning children’s programming data restrictions affecting monetization strategies in digital channels [S7][S9].

Conclusion: A New Media Powerhouse Under Construction With Material Execution Demands

Paramount Skydance Corporation stands at an inflection point where its heritage assets converge with cutting-edge demands embodied by intense streaming wars and aggressive M&A activity exemplified by its enlarged Warner Bros. bid. The company benefits from broad brand recognition spanning multiple generations but must successfully integrate diverse operations while competing effectively against entrenched rivals investing heavily in technology innovation.

Careful attention should be focused on how Paramount manages subscriber growth trajectories amidst rising content costs alongside outcomes associated with its ambitious acquisition strategy which may ultimately determine whether it emerges as a dominant media conglomerate or faces prolonged financial adjustments attributable to merger-related complexities.

This report summarizes publicly available information regarding Paramount Skydance Corporation as of early 2026 without offering investment advice or price predictions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments