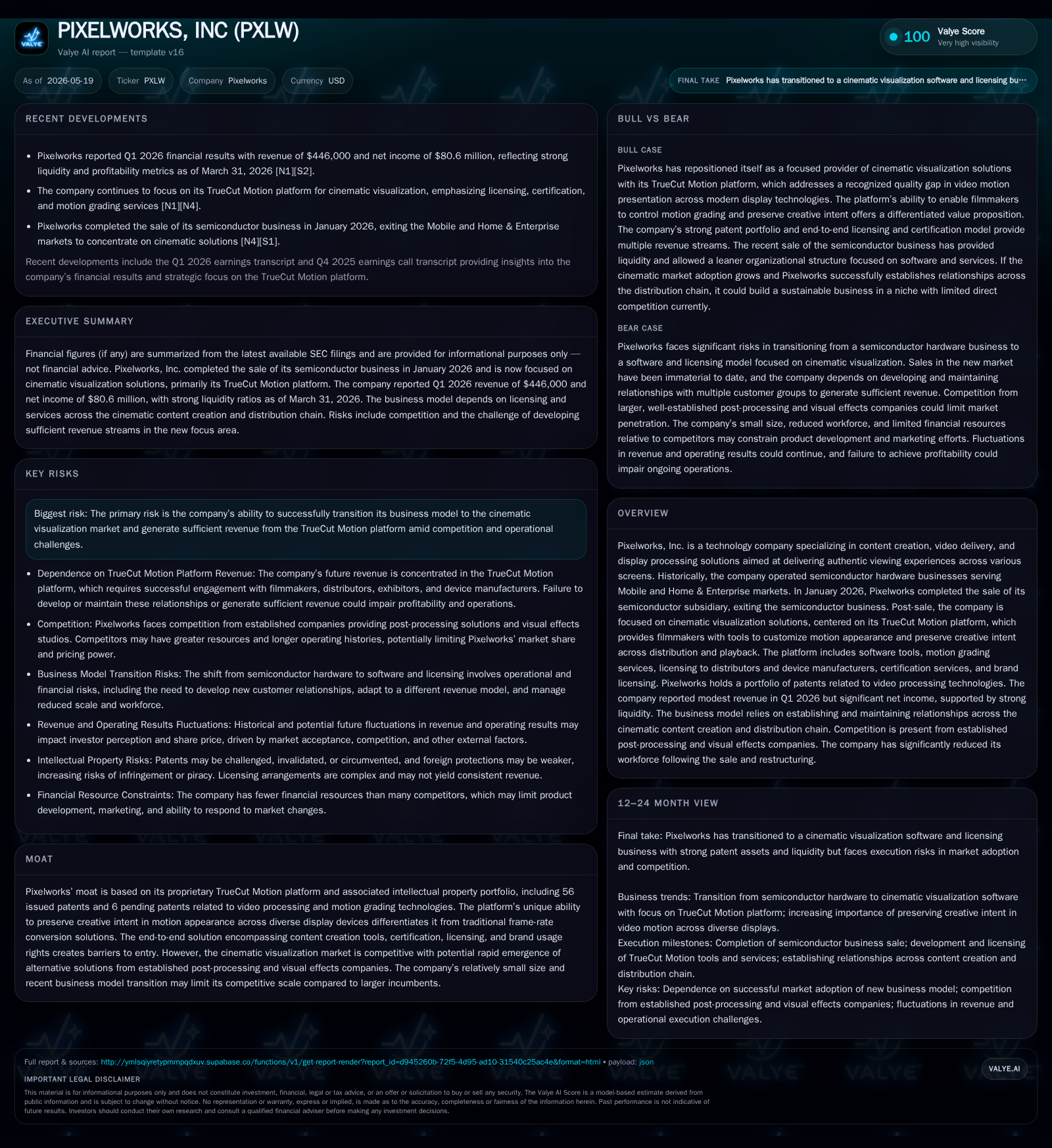

Pixelworks Unveils New Cinematic Era with TrueCut Motion Platform

Pixelworks completes semiconductor divestiture and pivots to cinematic visualization solutions centered on its proprietary TrueCut Motion platform.

In the first quarter of 2026, Pixelworks finalized the sale of its semiconductor subsidiary, signaling a full strategic pivot away from hardware toward cinematic visualization software and services. The company now focuses exclusively on its TrueCut Motion platform, which integrates motion grading tools, certification and licensing services designed to preserve filmmakers’ creative intent across display devices. While holding a sizable patent portfolio that underpins its unique technological moat, Pixelworks faces significant challenges from competition and market adoption as it strives to grow in a niche but complex cinematic content ecosystem. Its strong liquidity post-sale provides a runway for continued investment in product development and market expansion.

Latest Operational Update: Semiconductor Exit and Strategic Refocus

On May 14, 2026, Pixelworks filed its quarterly report (10-Q) confirming the completion of its divestiture of Pixelworks Semiconductor Technology (Shanghai) Co., Ltd. earlier this year [S2][S3]. The sale concluded on January 6, 2026 for approximately $51 million net of transaction costs and withholding taxes paid in China [S1][S9]. This transaction ended Pixelworks’ long-standing semiconductor hardware business that targeted Mobile (smartphones/tablets) and Home & Enterprise (projectors, personal video recorders) markets [S1][S8].

The divestment notably reduced operational complexity and freed capital resources, allowing management to streamline efforts toward growth in an entirely new direction: cinematic visualization technology. Post-sale, the company’s workforce dramatically downsized—from roughly 163 employees pre-sale to about 23 full-time staff focused exclusively on software-driven cinematic solutions [S4]. The company's liquidity position is strong with cash and equivalents near $57.8 million as of March 31, 2026 with almost no debt reported [F1], providing a solid financial foundation for continued investment.

Business Model Transformation: TrueCut Motion Platform Explained

With semiconductors behind it, Pixelworks now centers its entire revenue model around the TrueCut Motion platform—a complex offering aimed at addressing challenges in high-quality digital cinematic experiences [S1][N1]. Unlike legacy products sold as physical components, TrueCut operates primarily as a combination of software solutions, professional services, licensing fees, certification programs for device manufacturers, and brand licensing.

The platform comprises:

- Content Creation Tools: Software enabling filmmakers direct access to motion grading capabilities that precisely tailor motion appearance during production or finishing processes.

- Motion Grading Services: Professional grading executed by Pixelworks or partners that refine cinematic motion characteristics while preserving artistic intent.

- Licensing to Distributors and Devices: Fees charged for embedding TrueCut technology into content delivery chains (e.g., studios or streaming platforms) or into playback devices certified to properly display graded content.

- Certification Services: Validation programs ensuring hardware conforms to TrueCut standards.

- Brand Licensing: Allowing partners to leverage TrueCut branding as a quality mark signaling superior motion fidelity.

Revenue flows thus depend on building multi-level engagements: from filmmakers upstream creating graded content down through expanding distribution pipelines to device OEMs certified for playback accuracy [S15][S21]. Pricing dynamics involve a mix of project/service fees plus recurring royalties or flat license payments reflecting negotiated scope

Competitive Landscape and Industry Context in Cinematic Visualization

Pixelworks’ pivot places it within an emerging but competitive niche straddling content production tool providers, post-processing specialists, VFX studios, and IP licensors [S19][S6]. Traditional frame-rate conversion companies offer more generic artifact reduction methods but lack full creative-intent preservation that TrueCut targets.

Key competitors include major visual effects houses like Industrial Light & Magic (ILM), Digital Domain, Pixar Animation Studios which offer comprehensive digital effects suites that indirectly compete through artifact mitigation prior to distribution [S6][S16]. Software players such as Dolby Laboratories and Adobe provide overlapping tools but focus broadly on image/video enhancement without strict motion grading specialization [S19].

Pixelworks’ smaller scale (just over two dozen employees post-sale) limits its ability to rapidly innovate or market compared with these well-capitalized peers. Furthermore, the need for deep integration across multiple customers (content creators through device makers) presents organizational complexity uncommon among traditional single-layer solutions.

Intellectual Property Strength and Its Role in Differentiation

A cornerstone of Pixelworks’ positioning is its proprietary technology protected by a sizable intellectual property portfolio. The company holds 56 issued patents plus six pending applications covering innovations in motion estimation/compensation techniques, motion grading algorithms, image scaling/correction methods, automatic optimization procedures and video signal processing enhancements [S1][S4][S6]. These patents typically have between 1 to 16 years remaining term [S4], providing a moderate runway for exclusivity.

This IP portfolio underpins the unique capability of the TrueCut Motion platform to preserve the original filmmaker's intent regarding motion portrayal despite varying display refresh rates or viewing environments—an issue increasingly problematic given widespread HDR adoption and larger screen formats [S8]. This protection helps create barriers against commoditized frame interpolation solutions that do not meet artistic standards.

Beyond patents itself is a layered differentiation through combining software tooling with validation/certification programs plus brand recognition—all aimed at discouraging switching by embedding into multiple value chain points. However, risks remain if competitors innovate around or challenge these patents or replicate features without infringement issues [S11].

Growth Drivers: Expanding Film Industry Penetration and Licensing

Pixelworks is betting heavily on several vectors fueling demand for better cinematic visualization:

- Increasing theatrical/home consumption of high-fidelity video where judder artifacts are magnified by mismatches between standard film frame rates (24fps) and modern higher-refresh-rate displays.

- Demand from filmmakers prioritizing creative control over motion appearance, who seek advanced tools like TrueCut content creation software or grading services during production/post-production phases.

- Distributor/licensing uptake among studios/streaming providers wanting consistent consumer experience across devices, driving licensing revenue streams.

- Device manufacturer partnerships aiming for premium certification compliant with TrueCut standards, supporting brand placement on certified products.

- Potential expansion into adjacent media markets such as high-end home cinema systems or other professional video applications leveraging core IP.

Active pipeline progress includes client engagements highlighted in recent earnings commentary focusing on widening usage among independent filmmakers as well as early-stage collaborations with distributors/NAM OEMs [N1][S1]. The scalability largely depends on converting pilot projects into recurring licensed deployments.

Risks and Challenges: Scale, Competition, and Market Adoption

Despite promising IP differentiation and market focus shift, Pixelworks faces material hurdles:

- The small employee base (~23 post semiconductor divestiture) strains capacity needed for extensive product development while simultaneously managing multi-tiered customer relationships [S4].

- Intense competition from larger players with greater resources capable of bundling broader visual effects solve alternative problems which may encroach on Pixelworks’ target space [S19].

- Difficulty achieving critical mass adoption along all levels of distribution channel; failure to engage sufficient numbers of filmmakers/distributors/device makers could limit revenue generation below sustainable levels [S21].

- Pricing pressures may emerge if competitors offer lower-cost albeit less specialized solutions or if Pixelworks is compelled to invest heavily in marketing/sales efforts without immediate returns.

- Reliance on evolving industry standards poses unpredictability; rapid changes could outpace product development cycles reducing effectiveness or relevance [S5][S7].

- Operating losses continue due primarily to upfront investments behind TrueCut evolution; ability to manage cash burn versus longer-term revenue ramp remains uncertain [F1][S2].

Upcoming Catalysts: Product Developments and Market Partnerships

Key operational milestones investors might monitor include:

- Announcements of new releases or feature enhancements within the TrueCut Motion software toolset focused on usability or integration improvements.

- Expansion of certification programs targeting new device categories or OEM relationships reflecting broader market penetration.

- Signing multi-year licensing agreements with larger studios or streaming platforms validating commercial acceptance beyond pilot phases [N1].

- Entry into complementary markets such as professional broadcast or live content sectors leveraging patented algorithms.

- Potential acquisitions or partnerships enhancing technological offerings or accelerating go-to-market capabilities given current resource constraints.

Progress along these fronts will be crucial proof points confirming the viability of Pixelworks’ business model post-semiconductor era.

Financial Overview: Liquidity, Capital Structure, and Runway

Pixelworks enters this strategic phase backed by solid liquidity. As of quarter-end March 31, 2026 cash reserves stood at approximately $57.8 million with negligible debt outstanding [F1], translating into a very healthy current ratio (>28x) indicating strong short-term financial flexibility. The divestiture proceeded without residual liabilities related to the former semiconductor operations exceeding typical deal costs estimated around $2.2 million including escrow amounts held against tax contingencies [S9][S17].

However, sizable operating losses persist due primarily to ongoing spending on developing TrueCut technology alongside sales/marketing investments needed for platform commercialization. Revenue remains concentrated narrowly around early-stage TrueCut engagements totaling under $1 million yearly based on last reported figures indicating an early transition state from legacy streams [F1][S21]. Sustained profitability depends heavily on scaling licenses/contracts while managing fixed costs tightly going forward.

In sum, robust cash buffers mitigate immediate solvency risk but underscore urgency for revenue ramp-up amid competitive pressures requiring disciplined capital allocation aligned with business model transformation objectives.

This analysis leverages information available as of May 19, 2026 from Pixelworks’ latest SEC filings including Q1 Form 10-Q dated May 14, 2026 ([S2]) alongside related annual reports ([S1]), event filings ([S3],[S9]), news transcripts ([N1]), and companyfacts dataset ([F1]). It aims solely at providing a grounded operational/business perspective without investment research views.

Financial position in context

As of 2026-03-31, companyfacts shows $58mm in cash and equivalents [F1]. Current assets of $59mm and current liabilities of $2mm imply a current ratio near 28.21x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments