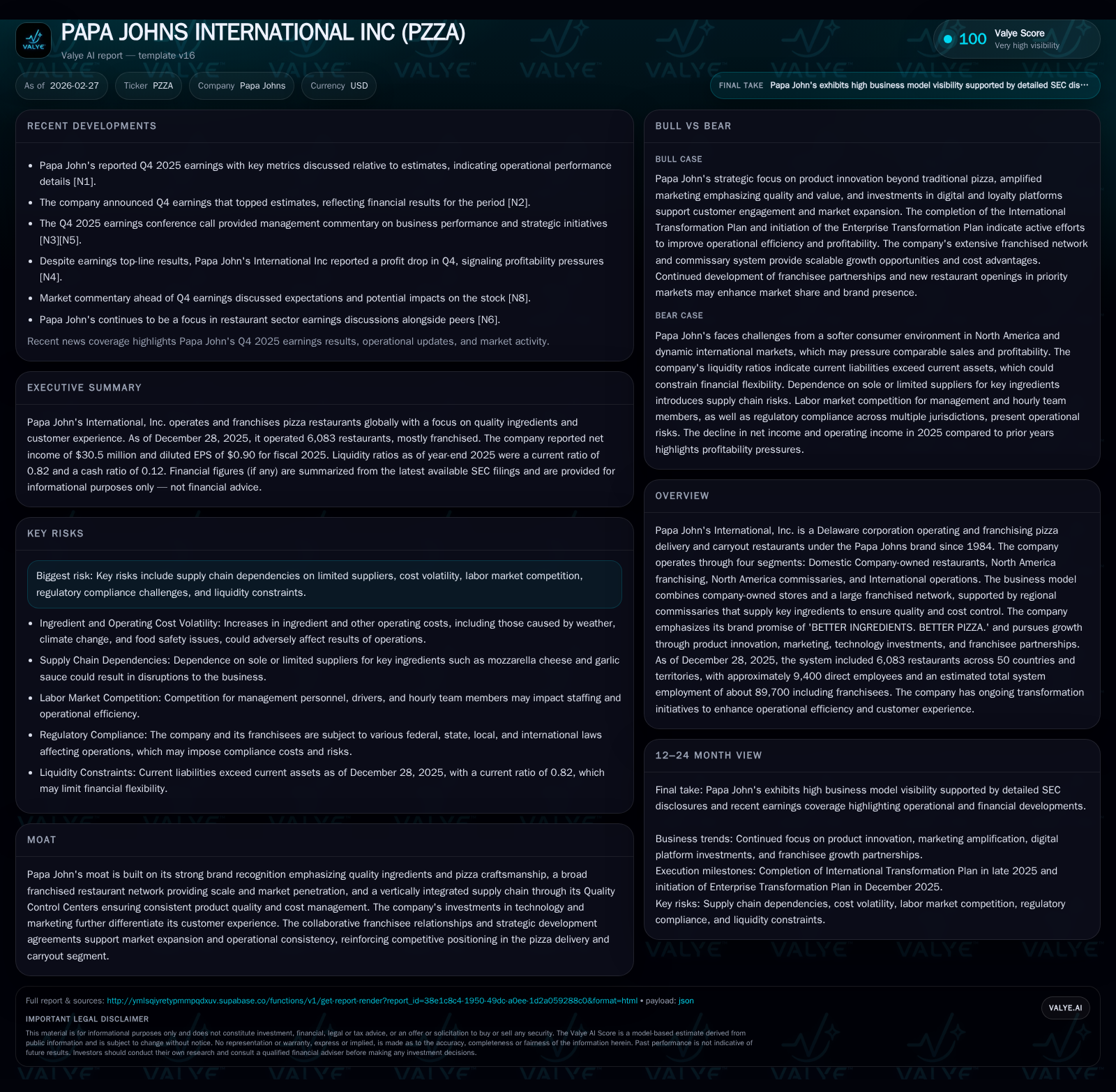

Papa John's International Faces Profit Pressure Despite Brand Strength

Papa John's robust brand and franchising model grapple with declining profits amid targeted growth investments in 2025.

Papa John's International posted a striking revenue surge in fiscal 2025, juxtaposed against significant declines in operating and net income, reflecting margin pressures in a challenging consumer environment. The company’s moat rests on its quality-driven branding, franchise scale, and vertically integrated supply chain, buttressed by substantial investments in marketing and digital innovation to enhance customer engagement. Despite profit headwinds, Papa John's maintains strong liquidity and capital discipline, with a leverage ratio well below covenant limits and an attractive dividend yield. Key risks persist around supply chain vulnerabilities, labor market pressures, and regulatory compliance, all of which bear watching alongside the progress of strategic transformation programs aimed at long-term growth.

Historical Revenue Growth and Profitability Trends Through 2025

Papa John's reported a staggering top-line increase in fiscal year 2025 driven predominantly by structural factors related to its evolving restaurant portfolio mix and refranchising activities. Revenue jumped approximately 395.4% from $724.7 million in FY2024 to around $2.05 billion in FY2025 [F1]. However, this top-line growth belies underlying profitability challenges as operating income declined sharply by roughly 43.1%, falling from $156.7 million to $89.1 million over the same interval [F1]. Net income suffered even steeper erosion, dropping nearly 63.4% to $30.5 million [F1]. These dynamics reflect significant margin compression attributable to elevated food costs—particularly cheese—higher labor expenses driven by competitive wage requirements, restructuring charges tied to transformation plans, and incremental marketing investments.

The divergence between revenue expansion and earnings contraction illustrates operating leverage pressures within the Domestic Company-owned segment amid softer comparable sales (-3.3%) [S24], compounded by ongoing supply chain cost volatility [S16]. Despite these headwinds, the North America commissaries segment grew adjusted EBITDA by $13.1 million year-over-year through higher transaction volumes and pricing adjustments [S24]. International operations demonstrated promising system-wide sales growth of ~7.7% with comparable sales advancing approximately 5%, delivering segment EBITDA improvement as well [S24]. Nonetheless, the net effect was subdued consolidated earnings performance.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 31 | 126 | 89 | 65 | -63.4% |

| 2024 | 83 | 107 | 157 | 72 | +1.7% |

| 2023 | 82 | 193 | 147 | 77 | +21.1% |

| 2022 | 68 | 118 | 109 | 78 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 61 | -6.9 |

| 2024 | 2 | 34 | -19.4 |

| 2023 | 210 | 116 | -17.9 |

| 2022 | 125 | 39 | -23.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue for FY2023 is not explicitly available; indicative figures based on narrative context.

Brand Differentiation and Franchise Model as Growth Pillars

Papa John's enduring competitive advantage is anchored in its strong brand promise: "BETTER INGREDIENTS. BETTER PIZZA." This ethos highlights its commitment to high-quality raw materials including six simple ingredients and fresh, never frozen original dough crafted via specialized processes at regional Quality Control Centers (QC Centers) [S1][S4]. These QC Centers serve as vertically integrated commissaries supplying both company-owned and franchised restaurants with pizza sauce, dough, food products, paper goods, and other essentials enabling tight control over cost structures and product consistency.

The company employs a barbell product strategy balancing its traditional premium pizzas with menu innovations that complement core offerings to expand overall addressable market [S25]. The nearly equal weight on product heritage plus innovation enhances brand loyalty while attracting broader segments.

Papa John's restaurant ecosystem consists of approximately 6,083 units worldwide as of December 28, 2025 — comprising roughly 475 company-owned stores primarily in North America alongside a vast franchised network of over 5,600 restaurants spread across North America and International markets [S1]. This hybrid model provides geographic scalability coupled with localized market penetration advantages through franchisees who contribute royalties, development fees, and marketing fund contributions supporting national brand initiatives.

Investments into technology platforms underpin the omni-channel customer journey with enterprise enhancements including CRM upgrades and loyalty programs aiding personalization efforts [S25]. Franchisee partnerships remain a strategic priority facilitating expansion especially in underserved international territories where pizza delivery models are less mature [S13].

Strategic Initiatives in Marketing, Digital Innovation, and Menu Expansion

In response to consumer shifts amid softer demand conditions domestically, Papa John's ramped up marketing investments by $21 million relative to prior year to strengthen its quality-focused messaging emphasizing craftsmanship behind its signature pizzas [S25]. These funds bolstered campaigns highlighting simple ingredients plus value propositions such as limited-time offers and Papa Pairings mix-and-match platforms designed for consumer appeal.

Digital transformation advanced markedly with rollout of a new omnichannel platform integrating refreshed mobile applications on iOS/Android plus an updated website offering streamlined ordering experiences aiming to reduce friction points [N1][N2][S25]. Given that most sales originate via digital channels (>70%), such infrastructure upgrades are critical for enhancing conversion rates while improving operational efficiency for teams.

Papa John's also pursued menu innovation consistent with barbell strategy fundamentals — layering novel complementary items alongside core pizzas to diversify offering and capture newer occasions without diluting premium positioning [S25]. Investments were aligned toward expanding addressable market segments while preserving the ‘better ingredients’ value pillar fundamental to franchisees' selling propositions.

Financial Performance Review: Profitability and Cash Flow

Despite robust revenue advancement from structural changes including refranchising transactions accounting for shifts in revenue recognition boundaries [F1], consolidated operating income decreased to $89.1 million from $156.7 million the prior year (-43%) driven by higher raw material costs (notably cheese inflation) plus increased labor wages stemming from competitive labor markets [F1][S16]. Net income contracted more sharply (-63%) due partly to non-cash charges from accelerated depreciation expenses linked with technology platform rollouts ($5–10 million estimated range), restructuring costs from enterprise transformation plans ($7.7 million recognized in FY2025), alongside inflationary pressures compressing margins [N3][S27].

Operating cash flow remained resilient at $126 million (+18%), benefiting from working capital management despite earnings decline; capital expenditures were curtailed by approximately -10.7%, reflecting disciplined spending amidst margin challenges [F1]. Free cash flow consequently amounted to approximately $61 million—modest but positive relative to ongoing investment requirements.

The company’s return on equity turned negative (~-6.9%) reflecting the combination of depressed net income against a substantially negative reported equity base primarily attributable to accumulated deficits stemming from historic share repurchases exceeding retained earnings over time [F1]. This underscores profitability pressures despite stable operational cash generation.

Capital Structure, Liquidity Position, and Allocation Priorities

Papa John's maintains a robust capital structure evidenced by total outstanding debt of approximately $722 million at end-2025 encompassing $400 million senior notes maturing in September 2029 plus a recently implemented $200 million term loan along with $122 million drawn under its revolving credit facility [S6][S19]. Remaining availability under revolving facilities stood at roughly $478 million providing ample liquidity buffers.

Financial covenant compliance remains solid with leverage ratio at about 3.2x Consolidated EBITDA well below the maximum allowed of 5.25x; interest coverage ratio similarly comfortable at approximately 3.2x earnings coverage [S6][S7].

Capital deployment priorities favor sustained investment for growth initiatives while ensuring balance sheet strength accompanied by shareholder returns primarily via dividends which yield above six percent as highlighted recently [N11][S12]. Share repurchases were inactive during fiscal year 2025 after prior years' significant buyback activity including notable Starboard-led purchases earlier on record [F1][S12], indicating prudent capital stewardship amid profit pressures.

Cash reserves approximated $34.6 million at year-end with restricted cash adding modest additional liquidity; current ratio hovered near 0.82 reflecting seasonal working capital cycles but supported sufficiently through credit lines and operational cash flow generation capacity [F1][S22][S26].

Risks Impacting Margins: Supply Chain & Labor Market Pressures

Key risk factors challenging margin stability include:

- Concentration on limited suppliers for core ingredients such as cheese exposes gross margins to commodity price volatility despite hedging efforts where feasible [S16]. Sustained disruption or price spikes could further compress margins.

- Intensifying wage inflation driven by competitive labor markets impacts store-level economics especially frontline roles essential for operations; scarcity of qualified personnel may constrain scaling without corresponding cost increases [S16].

- Regulatory complexity across jurisdictions adds compliance costs potentially creating operational friction especially within international expansion strategies.

- Elevated debt levels create sensitivity around liquidity risks contingent upon continued financial covenant adherence amidst operating uncertainties.

Outlook: Strategic Transformation Milestones & Growth Opportunities

Management continues executing transformational initiatives through the Enterprise Transformation Plan following completion of International Transformation efforts aimed at enhancing system health via refranchising underperforming units while investing strategically in high-potential domestic and international markets [S27][N8]. Innovation pipeline sustains momentum leveraging barbell strategy blending premium pizza heritage with diversified menu offerings targeting incremental customer occasions beyond traditional delivery segments.

Digital investments backed by data analytics seek ROI improvements through personalized offers amplified via upgraded CRM loyalty frameworks reinforcing retention vital amid macroeconomic softness seen particularly across North American core markets dampened by discretionary spending trends industry-wide [N7][N8][S25].

Despite cautious demand outlooks introducing revenue predictability challenges, disciplined cost management paired with calibrated marketing investment aims to provide protective buffers while pursuing long-term growth grounded on quality differentiation amid intensifying competition including aggregator influence across channels.

Key Metrics & Milestones To Monitor Going Forward

Investors should track:

- Effectiveness of increased marketing spend reflected through same-store sales performance shifts alongside customer acquisition/retention metrics derived from omnichannel platform adoption rates across Android/iOS apps plus web engagement data [N3][S25];

- Margin trends post-depreciation normalization linked to digital infrastructure rollouts coupled with restructuring charge amortization effects;

- Franchise development pace including new store openings notably within international markets where delivery models remain emergent balanced against domestic refranchising initiatives;

- Progress against planned cost savings (~$25 million anticipated beyond immediate term) signaling operating leverage restoration;

- Liquidity metrics encompassing covenant compliance ratios paired with monitored credit facility usage shaping near-term financial flexibility outlooks.

This analysis synthesizes publicly available financial filings including the recent Form 10-K dated February 26, 2026 alongside select earnings commentary sources without speculative assertions outside documented information sets noted herein. It reflects Papa John's established brand identity grappling with evident profitability constraints amid strategic reinvention efforts navigating evolving consumer demand environments while preserving balance sheet integrity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments