Ryder System Boosts Flexibility and Profit Amid 2026 Market Headwinds

Ryder leverages its fleet renewal and integrated logistics platform to drive operational resilience and improved profitability in Q1 2026.

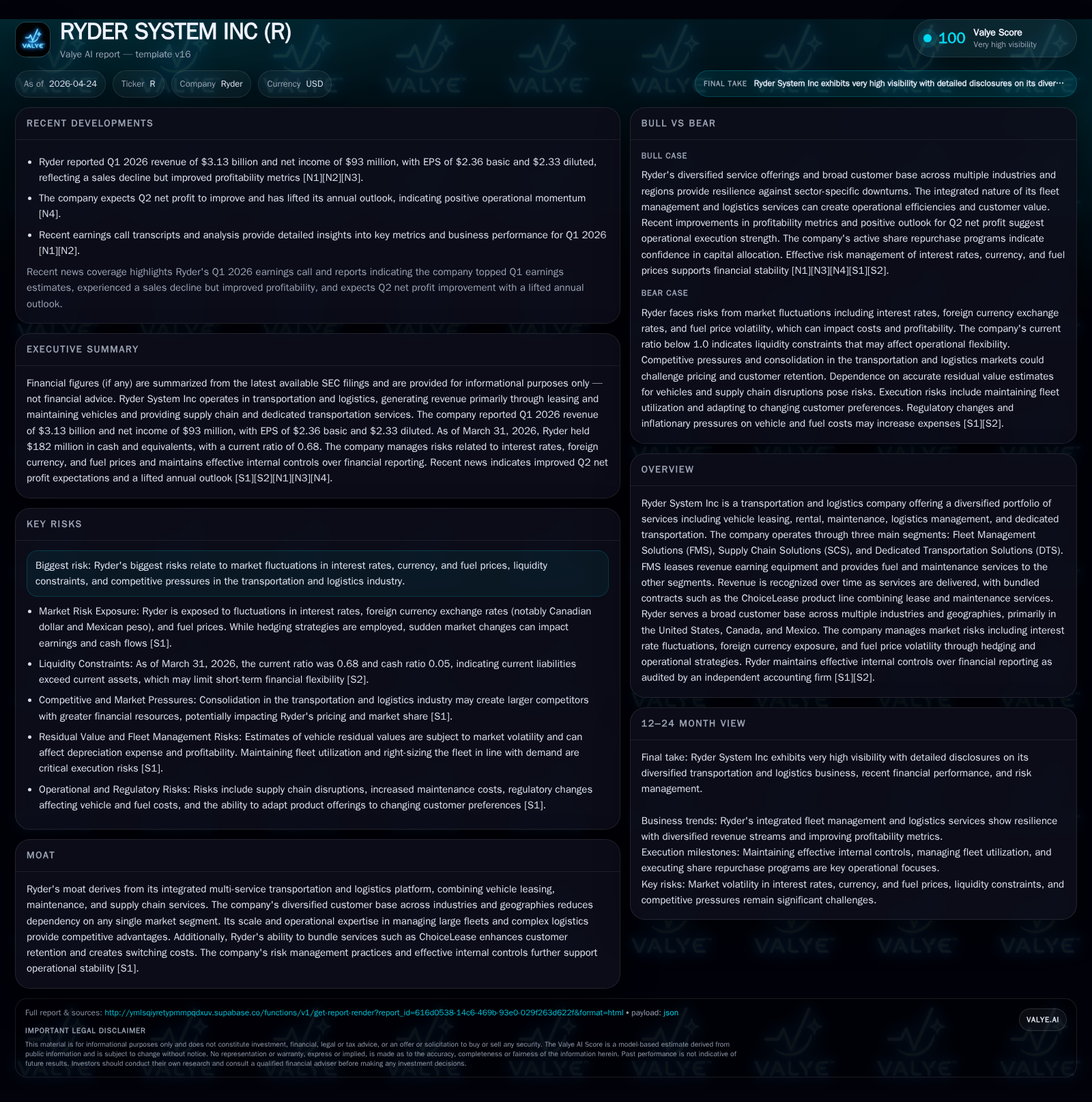

In its latest quarterly filing [S2], Ryder System Inc. reported solid operational performance despite modest revenue declines, attributing growth to strategic fleet investments and service bundling. The company’s integrated business model combining vehicle leasing, maintenance, and supply chain solutions continues to underpin steady cash flows and customer retention. While market risks including interest rate fluctuations and fuel price volatility pose constraints, Ryder’s diversified portfolio and scale advantage support steady growth. Share repurchases remain active, signaling management’s confidence in capital allocation.

Latest Quarterly Update: Operational Momentum and Financial Signals

Ryder System Inc.'s Q1 2026 10-Q filing [S2] reveals a company maintaining operational momentum despite near-term market pressures marked by modest declines in top-line rental revenue and fuel services. Importantly, the firm increased investment in its ChoiceLease fleet—a bundled leasing and maintenance offering—reflecting management’s confidence in sustaining recurring revenue streams. Concurrent event filings [S3] affirm ongoing share repurchase activity with over 1.25 million shares bought back at an average price of approximately $211 during the quarter, illustrating disciplined capital deployment during macro uncertainties.

Earnings call insights from April 23, 2026 ([N1],[N3]) suggest that while first-quarter revenues were slightly softer on commercial rental volumes aligned with broader transportation sector trends, net profits surpassed analyst estimates bolstered by operational efficiencies and pricing adjustments within the maintenance services component.

Reported current assets of $2.49 billion against liabilities of $3.67 billion yield a current ratio near 0.68 [F1], indicating working capital demands closely tie up short-term assets relative to liabilities requiring prudent cash flow management.

Table 1 below summarizes key operating metrics indicating segmental revenue breakdowns and fleet investment trends:

| Metric | Q1/FY2025 |

|---|---|

| Total Revenue (Annualized) | $12.67 billion [F1] |

| FMS Revenue | $5.85 billion Annually [S7] |

| ChoiceLease Revenue | ~$3.5 billion Annually [S9] |

| Commercial Rental | ~$937 million Annually [S9] |

| Fleet Renewal Capex | $1.51 billion (Revenue Earning Equipment) FY2025 [S22] |

Integrated Business Model and Product Quality: Leasing, Maintenance, and Logistics Bundling

Ryder’s core strength lies in its Fleet Management Solutions (FMS) segment that orchestrates revenue-earning equipment leases bundled with complementary maintenance services under ChoiceLease [S1]. This bundling builds durable switching costs by integrating lease contracts with upkeep services typically spanning three to seven years for trucks and tractors—a horizon enabling stable margin capture through lifecycle economics.

The comprehensive maintenance provisions enhance customer stickiness beyond mere asset leasing and include proactive fuel management services enhancing cost control for clients.

Additionally, dedicated transportation services (DTS) integrate vertically with Supply Chain Solutions (SCS), which provides end-to-end logistics management tailored primarily toward omnichannel retail and automotive clients—two sectors experiencing evolving demand patterns shaped by e-commerce penetration and just-in-time inventory models [S6,S17].

Ryder's capability to offer these combined services via long-term contracts drives predictable revenue recognition over time while diversifying exposure away from commoditized rental operations.

Competitive Environment and Industry Structure: Scale, Diversification, and Risk Management

Operating predominantly across the US, Canada, and Mexico presents Ryder with significant scale advantages relative to competitors such as Herc Rentals or smaller regional players who lack multi-service breadth or geographic reach [S6,S17]. With revenue diversified across industries—Omnichannel retail ($1.88B), Automotive ($1.54B), Consumer Packaged Goods ($1.21B)—concentration risk is minimized allowing cyclical shocks in one vertical to be absorbed without disproportionately impacting consolidated results.

The company's risk management framework addresses key exposures related to interest rate fluctuations given the significant fixed-rate debt portfolio (~$6.1B fixed rate at ~5.10% average) alongside variable-rate components hedged via swaps targeting SOFR benchmarks [S1]. Fuel price volatility is partially managed through contractual pass-through mechanisms in commercial rental contracts coupled with active commodity hedging when appropriate.

Strategic procurement of new vehicles considers supply chain complexities such as semiconductor shortages or chassis availability that have intermittently hampered capacity expansion industry-wide but appear easing currently based on recent signing activities for replacement units [N10].

Growth Drivers: Fleet Renewal, Service Expansion, and Geographic Penetration

Investment prioritization remains focused on renewing the ChoiceLease fleet capex which stood at approximately $1.51 billion in FY2025 representing a reduction from prior years but signaling ongoing commitment to maintaining a modern asset base capable of commanding premium pricing through efficiency gains—integration of telematics devices among them adds value both for safety monitoring and route optimization.

Beyond fleet renewal, Ryder seeks incremental growth through enhanced logistics technology offerings within SCS including real-time supply chain visibility platforms aimed at high-demand verticals adapting to rapid order fulfillment requirements brought on by ecommerce acceleration.

Geographic diversification continues to moderate dependence on any single national economy—a prudent approach amid disruptive factors like US-Mexico trade policy shifts or currency volatility in Canadian operations that could otherwise adversely impact margins.

Growth Constraints: Market Risks and Capital Intensity

Despite these growth avenues, Ryder remains capital intensive; vehicle acquisitions require upfront outlays driving sustained leverage levels visible in the net debt position of roughly $7.55 billion as of March 31, 2026 versus cash reserves near $182 million highlighting operational gearing constraints [F1]. Exposure to fuel price swings persists despite hedging; sudden spikes can widen operating costs affecting contract profitability particularly where pass-through clauses are limited.

Operating in a competitive landscape pressures pricing especially within the commercial rental segment where spot rentals remain sensitive to economic cycles affecting utilization rates.

Interest rate risk also looms given refinancing needs for maturing medium-term notes although staggered debt maturities provide some cushion through 2030 appreciating management’s careful balancing act between fixed vs floating exposures [S15,S16].

Upcoming Catalysts: Guidance, Execution Benchmarks, and Demand Indicators

Looking ahead, Ryder’s forthcoming second quarter results are anticipated to reflect margin expansions derived from contract repricing initiatives alongside improved utilization metrics in rental fleets as reported at recent earnings events ([N10]). Key milestones include tracking new contract signings within integrated logistics solutions which may proffer higher-margin recurring revenue profiles than legacy leasing operations.

Success of tech-enabled offerings targeting supply chain optimization will serve as an early demand gauge for long-term SCS segment growth potential amid evolving customer expectations towards digital transformation.

Monitoring capital expenditure pacing particularly on replacement vehicle deployments will reveal management's appetite for growth investment versus cash preservation under prevailing macro conditions.

Current Financial Profile: Liquidity, Debt Positioning, and Capital Allocation

At March 31, 2026 balance sheet levels reveal cash & equivalents of approximately $182 million against total debt nearing $7.73 billion placing net debt around $7.55 billion—figures consistent with Ryder’s history of leveraging asset ownership supporting lease operations [F1]. Reported current assets of $2.49 billion against liabilities of $3.67 billion yield a current ratio near 0.68 [F1], indicating working capital demands closely tie up short-term assets relative to liabilities requiring prudent cash flow management.

Operating cash flow generation was robust at nearly $2.59 billion annually recently with free cash flow positive but tempered by capex reductions reflecting cautious fleet spending post Covid-related surges ([F1],[S1]).

Share repurchase activity remained elevated into Q1 under board-approved discretionary programs totaling over 1.25 million shares at an average cost upwards of $210/share signaling confidence amidst a challenging environment but balanced against maintaining conservative leverage targets ([S2],[S18]). Dividend distributions continue at a consistent pace providing income stability while preserving flexibility for opportunistic acquisitions or selective reinvestment.

Table 2: Latest Financial Snapshot as of March 31, 2026

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | Capex ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.7 | 499 | 2.6 | 2.1 | +0.2% | +2.0% |

| 2024 | 12.6 | 489 | 2.3 | 2.7 | +7.2% | +20.4% |

| 2023 | 11.8 | 406 | 2.4 | 3.2 | -1.9% | -53.2% |

| 2022 | 12.0 | 867 | 2.3 | 2.6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 145 | 519 | 459 |

| 2024 | 135 | 321 | -418 |

| 2023 | 128 | 337 | -881 |

| 2022 | 123 | 557 | -321 |

Source: SEC companyfacts cache [F1].

This analysis is grounded exclusively on verified SEC filings ([S1]-[S3]), recent earnings call transcripts ([N1],[N3],[N10]), company facts data ([F1]) as of Q1 2026 quarter-close without speculative extrapolation or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments