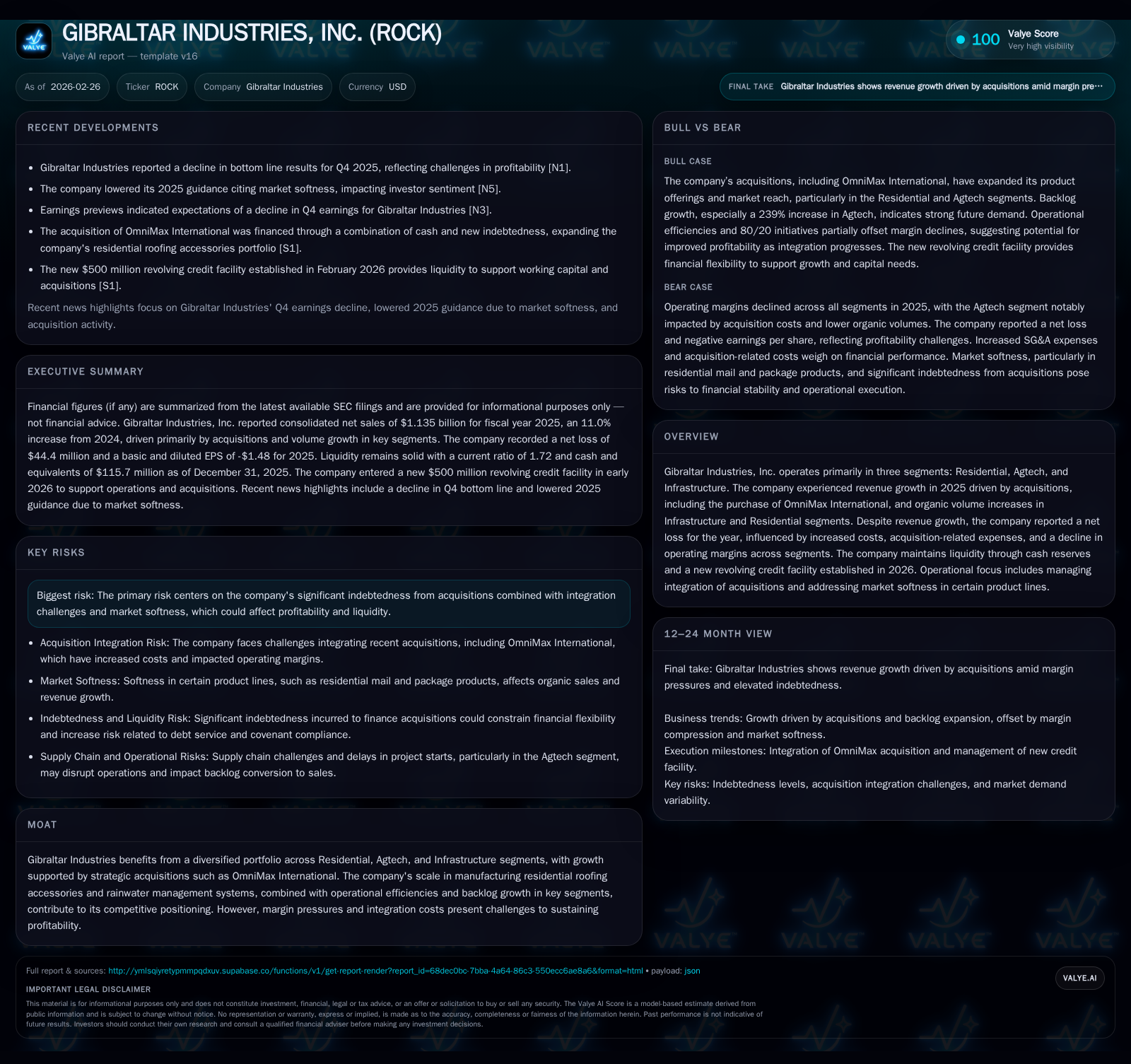

Gibraltar Industries Faces Margin Pressures and Integration Costs Following OmniMax Acquisition

The 2025 fiscal year saw Gibraltar Industries grow revenues through acquisitions yet incur a net loss driven by margin compression and acquisition-related expenses.

Gibraltar Industries expanded its top line in 2025 primarily through the acquisition of OmniMax International and other businesses, alongside organic volume growth in select segments. However, increased costs, challenging market conditions in some product lines, and integration expenses led to a net loss despite revenue gains. The company's liquidity remains supported by substantial cash reserves and a new revolving credit facility established in early 2026. Going forward, managing debt levels and successfully integrating acquisitions are critical for restoring profitability.

Overview

Gibraltar Industries, Inc. operates three principal business segments: Residential, Agtech, and Infrastructure.[S1][S6][S7] The company experienced top-line growth fueled by acquisitions completed during 2025, notably the February 2026 closing of OmniMax International, a significant player in residential roofing accessories and rainwater management systems.[S14][S18] Organic volume growth contributed as well within Infrastructure and Residential businesses; however, these gains were partially offset by softness in certain product lines such as residential mail/package products tied to new construction pace and project timing delays within Agtech.[S7]

Despite increasing consolidated net sales to approximately $1.14 billion in 2025 from $1.02 billion in 2024 (an 11% increase attributed mainly to acquisitions), total revenue actually declined versus the prior year figure of about $1.31 billion when adjusted for portfolio sales — highlighting underlying organic headwinds.[F1][S7] This discrepancy arises because the company sold off its electronic locker business segment previously included within Residential revenues.[S7]

Historical Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1136 | -44 | 167 | 123 | -13.2% | -132.3% |

| 2024 | 1309 | 137 | 174 | 143 | -5.0% | +24.3% |

| 2023 | 1378 | 111 | 218 | 151 | -0.9% | +34.1% |

| 2022 | 1390 | 82 | 103 | 130 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 64 | 121 | -4.7 |

| 2024 | 12 | 154 | 13.1 |

| 2023 | 29 | 203 | 12.1 |

| 2022 | 89 | 83 | 10.0 |

Source: SEC companyfacts cache [F1].

Revenue peaked at nearly $1.38 billion in FY23 before moderating through portfolio adjustments and market challenges into FY25.[F1] Operating income dropped consistently from a high of ~$151 million in FY23 to $123 million last year reflecting margin pressures resulting from shifting business mix and rising costs.[F1][S7]

Notably, net income swung dramatically from solid profits through FY24 ($137 million) into a loss position ($44 million negative) last year due to significant non-operating charges associated with acquisitions including impairment losses and integration-related expenses.[F1][S7] Meanwhile, operating cash flow has remained positive but contracted slightly amidst increased capital expenditures supporting acquired businesses’ integration and enhanced capabilities.[F1]

Segment Contributions & Operational Challenges

Residential: Revenues increased by around $42 million or over +5% in FY25 largely attributable to three acquired metal roofing manufacturers contributing roughly $65 million,[S7] offset by softness in mail/package products linked to residential construction activity declines.[N4,S7] Operating margin compressed from a robust ~19% margin in FY24 to about ~16.6% last year due to product mix changes and acquisition integration costs.[S11]

Agtech: This segment posted one of the sharpest revenue uplifts (+43%) driven predominantly by the Lane Supply acquisition accounting for over $106 million,[S7] but organic volumes were negatively affected by project start delays that weighed on margin performance (down from ~7.2% to ~4.5%).[S11]

Infrastructure: Growth was more modest (+4.7%), reflecting continued strength in execution but backlog shrank slightly (

4%). Margins held relatively steady (24%), though slight product line effects caused minor compression.[S7][S11]

Overall consolidated gross margin moved down from a healthy ~29.5% in FY24 to ~26.9%, reflecting unfavorable business mix changes partially offset by operational efficiencies like the ongoing "80/20" productivity initiatives common across industrial manufacturing sectors aiming to optimize product portfolios.[S7]

Liquidity & Capital Structure

Gibraltar's liquidity profile is anchored by approximately $115.7 million of cash & equivalents on hand alongside current assets totaling roughly $629 million versus current liabilities near $366 million — implying a healthy current ratio of about 1.72x at fiscal year-end '25.[F1]

To finance the sizeable OmniMax acquisition completed in early February ’26 — costing around $1.335 billion — Gibraltar secured senior secured credit facilities totaling about $1.8 billion comprising term loan facilities A & B ($650 million each) plus a newly arranged revolving credit facility with an initial commitment of $500 million maturing between five and seven years later.[S14][S15][S21]

These new debt instruments feature quarterly amortization schedules with interest rates tied to Term SOFR or base rate benchmarks plus applicable margins indexed on leverage levels.[S15] Covenants include maximum first lien net leverage ratios starting at up to approximately 5.25x stepping down over time along with minimum interest coverage requirements typical for sizable private equity-backed acquisitions or complex industrial rollups.[S15]

Capital Allocation & Returns

Despite its challenging results, Gibraltar continued active capital returns with share repurchases totaling about $63.9 million in FY25 versus roughly $12 million the prior year.[F1] Dividend payout figures were not explicitly disclosed for these periods.

Capex surged sharply by more than double year-over-year, rising to approximately $46.4 million from just under $20 million largely reflecting investments tied to newly acquired assets integration efforts along with maintaining existing manufacturing infrastructure.[F1][S11]

Operating cash flow remains positive at about $167 million, yielding free cash flow exceeding $120 million after subtracting capex – signaling sufficient internal liquidity generation even amid elevated expenditure needs.[F1]

Return on equity based on last fiscal year’s negative net income approximates -4.7%, underscoring near-term profitability pressures post-acquisition but tempered by solid equity capitalization expansion following issuance related to financing deals.[F1]

Future Growth Prospects & Risks

The company's immediate growth prospects revolve around fully integrating acquisitions such as OmniMax[N3][S14][S18] while harnessing demand tailwinds reflected by backlog doubling (+102%) up to around $281 million chiefly driven by strong order inflows within Agtech (+239%) and overall Residential segments.[S7]

Yet risks loom large including elevated indebtedness resulting from acquisition financing burdens coupled with execution challenges common when merging disparate industrial manufacturing platforms—particularly under volatile market conditions impacting construction starts and government infrastructure spending incentives like those embodied in the Infrastructure Investment & Jobs Act.

Other notable uncertainties include raw material pricing volatility affecting cost structures,[S12][S20] potential delays triggered by supply chain disruptions or regulatory scrutiny surrounding large-scale transaction closures,[S26][S27] competition intensification within specialized roofing accessory markets as well as emerging tariff implications currently subject to review.

Management emphasizes continual focus on operational efficiency improvements alongside selective portfolio optimization intended to mitigate softness seen notably in mail/package product lines which historically track new single-family housing construction metrics tightly[S7].

Forecasts / Milestones / What To Watch For

While official guidance revisions occurred downward during late-2025 citing market softness,[N4] subsequent communications tipped ongoing adjustment periods linked to integrating large targets like OmniMax with modest near-term earnings pressure expected[N3][N5]. Observers should note upcoming quarterly releases for signs of progressive margin recovery or sustained cash flow resilience.

Key performance indicators include:

- Progression of operating margins especially within Residential and Agtech segments,

- Conversion rates from backlog into revenue,

- Debt covenant compliance amid macroeconomic shifts,

- Capital expenditure discipline post-integration phase,

- Market demand signals for core product lines influenced by construction sector momentum.

Conclusion

Gibraltar Industries’ recent strategic acquisitions underpin revenue growth but have coincided with margin compression, integration costs, and a notable swing into net losses during fiscal ’25. The firm has bolstered liquidity via substantial revolver capacity while managing increased leverage stemming largely from the OmniMax purchase.

Successful realization of synergies, operational execution amid prevailing economic uncertainties, and prudent capital allocation remain crucial for re-establishing consistent profitability ahead.

This analysis utilizes publicly disclosed financial data and SEC filings as of February 26, 2026, alongside reputable news sources without offering investment advice or forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments