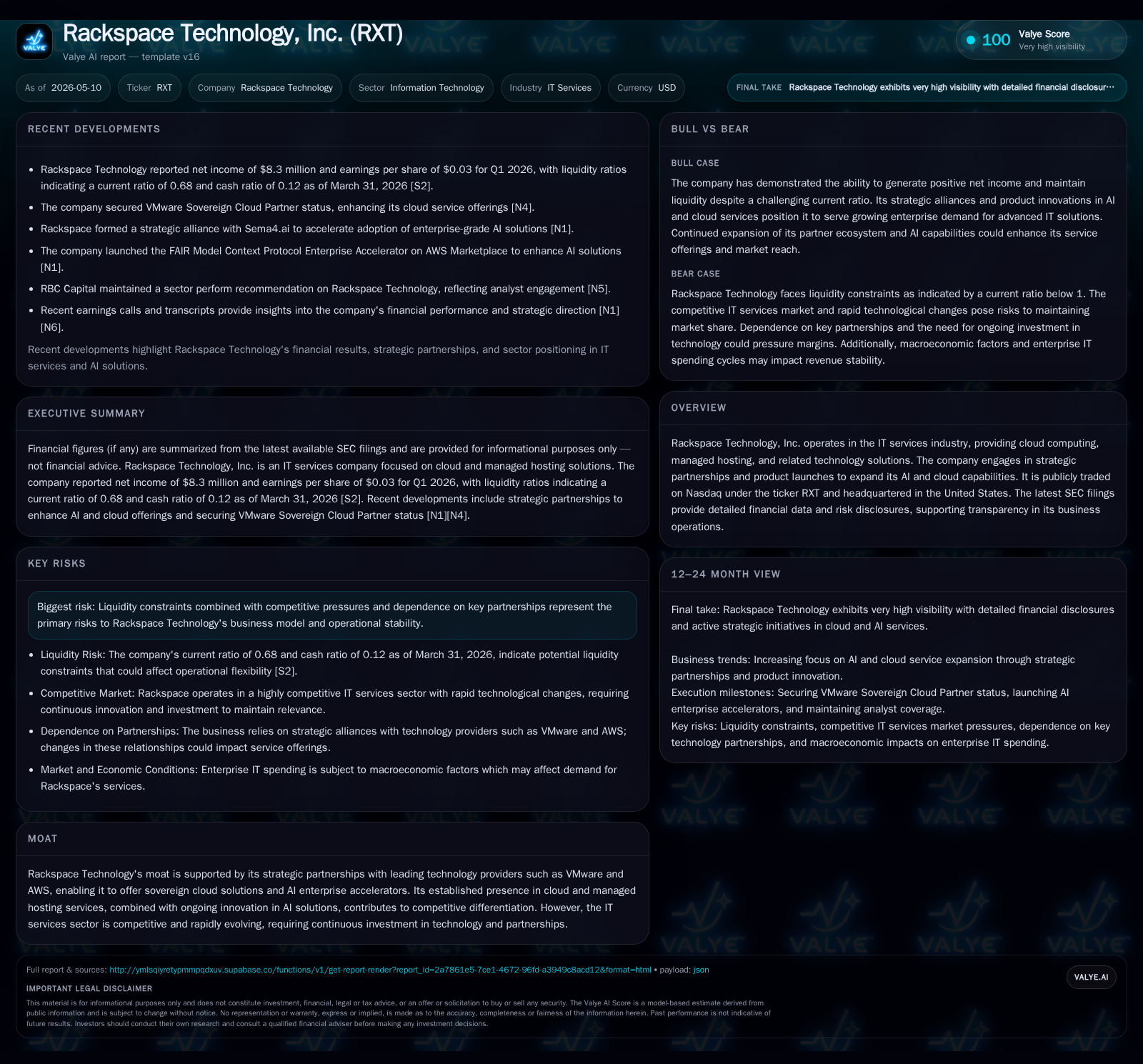

Rackspace Technology Builds Momentum with AI Cloud Partnership and Resilient Services Model

Latest quarterly disclosures reveal Rackspace's strategic pivot into AI-enhanced cloud solutions while navigating financial leverage and competitive industry pressures.

In its May 2026 quarterly filing, Rackspace Technology detailed a growing focus on AI-driven cloud capabilities, sparked by a notable partnership with AMD that boosted investor sentiment. The company's revenue model centers on multi-cloud managed services, underpinned by key alliances with VMware and AWS that support sovereign cloud offerings critical to regulated sectors. Despite these growth catalysts, Rackspace faces liquidity constraints and high leverage that temper operational flexibility amid fierce competition. Monitoring contract renewals, alliance expansions, and margin trends will be essential indicators of execution progress.

Latest Quarterly Operating Update: A Shift Toward AI-Driven Cloud Solutions

Rackspace Technology's first quarter fiscal 2026 results, reported in the May 8, 2026 10-Q [S2] and supplemented by the May 7 event filing [S3], cement a clear strategic pivot towards embedding artificial intelligence capabilities within its cloud service portfolio. The company disclosed progress in commercializing ‘‘AI enterprise accelerators,’’ specialized solutions designed to complement core multi-cloud services with enhanced intelligence layers.

A key near-term catalyst was the announcement of a strategic partnership with AMD, leveraging AMD’s AI-focused chipsets within Rackspace’s sovereign cloud framework [N2]. This deal sparked a significant market reaction as detailed in Nasdaq reports [N4], positioning Rackspace as a more differentiated player amidst intense competition from hyperscalers and traditional IT service vendors.

Management commentary during the April-May earnings call [N1] emphasized ongoing investments in AI capabilities integrated with existing VMware and AWS partnerships, reflecting a mix-shift toward higher-value offerings. However, the company also flagged margin headwinds common to this transformation phase and reaffirmed controls on operating expenditures to balance profitability aims.

Rackspace Business Model: Multi-Cloud Managed Services Anchored by Partnerships

Rackspace generates revenue primarily through comprehensive managed services spanning public clouds (AWS, Azure), private/compliant sovereign clouds, and hybrid IT environments [S1]. This includes infrastructure management, migration support, security operations, and increasingly AI-enabled service layers branded as enterprise accelerators.

Strategically significant are Rackspace’s partnerships which provide access to leading-edge technologies without requiring full-stack platform ownership. VMware integration enables hybrid cloud orchestration with strong cross-platform management tools; AWS relationships facilitate scalable public cloud consumption alongside Rackspace's managed hosting.

This ecosystem-centric approach fosters higher switching costs for customers due to integrated workflow complexity and governance compliance requirements particularly in regulated sectors reliant on sovereign cloud functionalities — a niche Rackspace exploits for differentiation.

Competitive Positioning within the IT Services Ecosystem

Operating amid giants like Accenture, IBM, and hyperscale providers’ own professional services arms keeps pricing discipline under constant pressure [S1]. The IT services market demands rapid innovation cycles driven by client demand for AI/ML-enabled analytics plus cost-effective data sovereignty solutions.

Rackspace sustains competitive positioning through partner-enabled offerings rather than direct platform ownership — allowing agility but constraining margin expansion potential given partner revenue sharing. Its recognized brand in managed hosting coupled with emerging AI competency supports retention but also exposes it to commoditization risks if hyperscalers scale similar integrated offerings.

Customer adoption reflects structural industry shifts toward multi-cloud deployments but remains sensitive to macroeconomic oscillations impacting IT budgets.

Expansion Catalysts: Partnerships, AI Enterprise Accelerators, and Cloud Sovereignty

The recent AMD agreement represents more than an incremental contract; it signals an effort to align hardware innovation tightly with software-managed service value adds to capture share in the nascent AI cloud acceleration segment [N2], [S2]. These AI enterprise accelerators embed machine learning processing capabilities designed for enterprises aiming to deploy scalable AI workloads compliant with data privacy mandates.

Complementing this are sovereign cloud initiatives targeting government and highly regulated industries seeking geographic data control coupled with advanced compute functionality—an area where Rackspace leverages VMware and AWS platform strengths consolidated under its management umbrella.

Such differentiated products create potential upsell paths yielding improved pricing power and customer stickiness amid competitive headwinds.

Risks and Constraints: Liquidity Stress, Partnership Dependence, and Market Dynamics

On the risk front highlighted in the May quarter filing [S14], liquidity constraints are prominent. With $93.6 million cash versus $785.6 million current liabilities at quarter-end March 31, 2026 ([F1]), Rackspace’s current ratio stands at a tight 0.68 — below conventional comfort thresholds posing operational risks especially if revenue growth slows or capital markets tighten.

Total debt of approximately $2.48 billion ([F1]) leaves little room for aggressive capex or acquisitions without careful refinancing or deleveraging strategies. Heavy reliance on partnerships for core technology stacks introduces exposure to shifts in supplier policies or technology roadmaps that could disrupt service delivery or margins.

Competitive intensity continues amid tech convergence accelerating client demands for integrated AI/cloud ecosystems — requiring sustained investment that may further weigh on short-term profitability.

Key Milestones and What to Monitor Next

Stakeholders should monitor subsequent quarters for:

- Traction metrics around AI enterprise accelerator adoption reflecting true demand beyond early deals.

- Renewal terms of major partner agreements signaling stability or risk of displacement.

- Any announcements regarding refinancing actions or capital restructuring aimed at mitigating leverage concerns.

- Margin progression indicating whether operational efficiencies offset incremental investments.

- New contract wins within regulated sectors validating sovereign cloud positioning. These indicators will reveal whether Rackspace moves beyond proof-of-concept into scalable growth phases supporting long-term competitiveness.[S2],[N1],[S3]

Financial Position Snapshot: Liquidity, Debt Structure, and Profitability Challenges

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $94mm | |

| 2026-03-31 | ||

| Total debt | $2.5bn | |

| 2026-03-31 | ||

| Net debt | $2.4bn | |

| 2026-03-31 | ||

| Current assets | $535mm | |

| 2026-03-31 | ||

| Current liabilities | $786mm | |

| 2026-03-31 | ||

| Current ratio | 0.68x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | $93.6M |

| Total Debt | $2.48B |

| Net Debt | $2.38B |

| Current Assets | $535.1M |

| Current Liabilities | $785.6M |

| Current Ratio | 0.68 |

As of March 31, 2026 ([F1]), this snapshot underscores the financial headwinds described earlier: constrained liquidity juxtaposed with substantial debt obligations limits operational flexibility amid necessary innovation investments. Continued net losses illustrated by prior period results (operating income was negative in late 2025) frame urgency around achieving sustainable margin improvements through product mix optimization and cost controls.[F1],[S2]

This analysis draws solely on SEC filings and verified company disclosures without extrapolation or forecast beyond stated facts. The focus remains on interpreting evidence-based operational shifts and their implications within the evolving IT services sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments