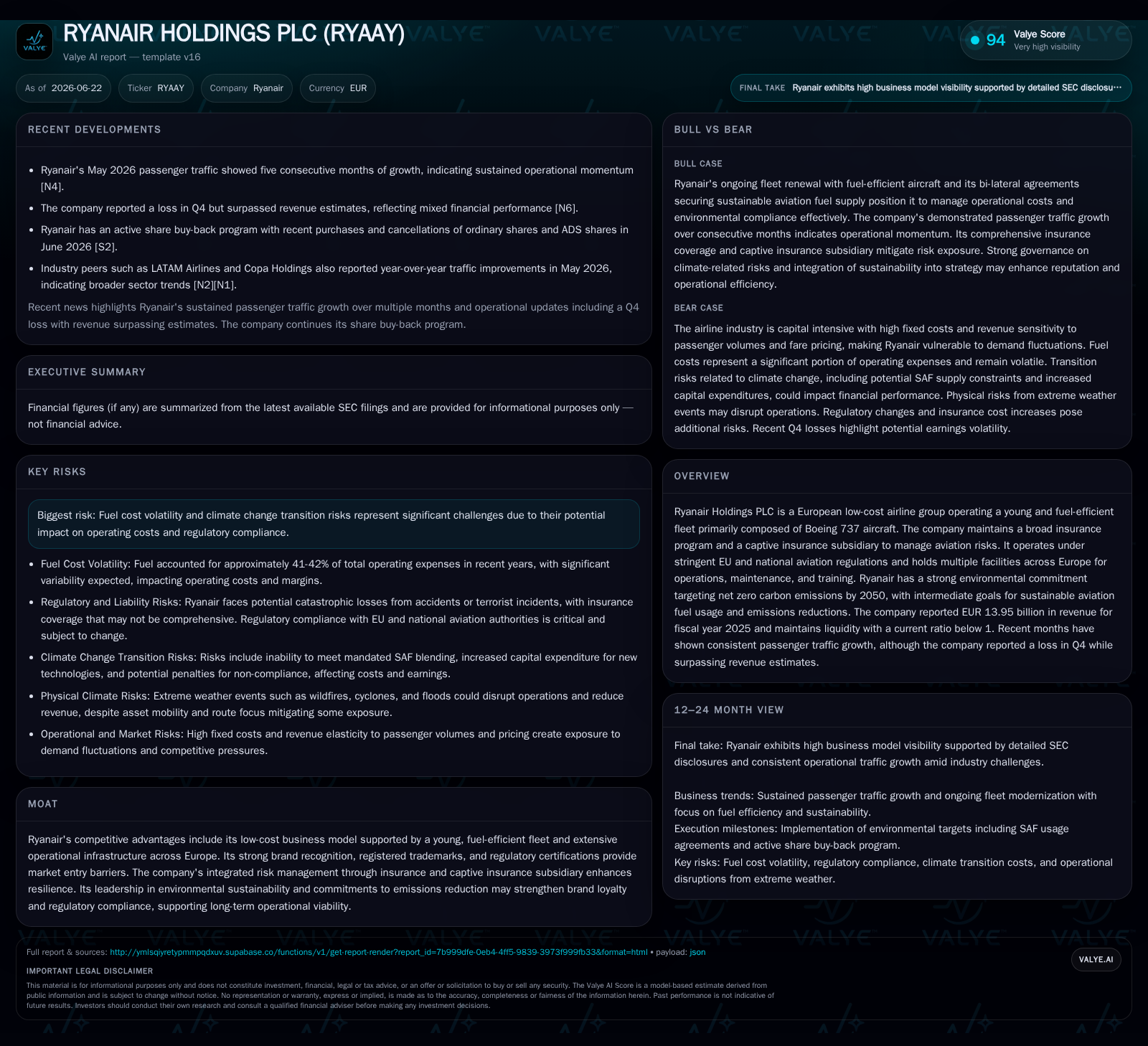

Ryanair Expands Fleet and Navigates Regulatory Hurdles Amid Rising Passenger Demand

Ryanair's recent share buyback and fleet expansion underscore its low-cost leadership despite regulatory and fuel cost challenges.

Ryanair’s latest filings reveal ongoing share repurchases aligned with its capital return strategy alongside steady growth in passenger traffic and revenue. The airline continues to push fleet modernization with a large order of Boeing 737 MAX-10 aircraft, emphasizing fuel efficiency and cost control. However, it faces regulatory risks including significant fines for alleged market dominance abuses in Italy. Ryanair’s entrenched low-cost model, supported by high aircraft utilization and ancillary revenue growth, sustains its competitive edge in the European market amid persistent fuel price volatility and tightening environmental regulations.

Recent Operating Update

Ryanair Holdings PLC’s latest regulatory filings from June 2026 disclose active share repurchase activity under its existing buy-back scheme announced in May 2025. Specifically, it bought back more than 9,500 ordinary shares plus nearly 242,000 shares underlying American Depositary Shares for cancellation in mid-June, signaling ongoing capital return efforts consistent with shareholder value policies [S2]. Concurrently, the company reported financial year fiscal 2026 results demonstrating robust operational momentum despite sector headwinds. Revenues rose to approximately €15.55 billion, up 14% from the prior year due to passenger volume growth of 4% to over 208 million and a roughly 10% increase in average fares [S1][S7]. Ancillary revenues contributed substantially to total income via a +6% increase fueled by higher per-passenger spending.

Business Model Analysis

Ryanair operates one of Europe’s largest low-cost carrier (LCC) fleets dominated by Boeing narrow-body aircraft—mainly Boeing 737s—with a young average age designed for fuel efficiency and cost savings. As of FY26 end, its principal fleet comprised approximately 621 Boeing jets including about 210 Boeing 737-8200 “Gamechanger” variants known for lower fuel burn,[S1][S19] plus a supplemental roster of leased Airbus A320s across subsidiaries like Lauda Europe. The company plans an expanded fleet approaching approximately 800 aircraft by FY34—with firm orders placing heavy emphasis on the next-generation Boeing 737 MAX-10 model, which offers improved economics through reduced fuel consumption per available seat kilometer (ASK) and higher seating density [S1][S19].

Revenue generation derives primarily from scheduled passenger ticket sales augmented by ancillary streams such as baggage fees, priority boarding charges, onboard sales, and internet services—collectively contributing roughly one-third of total revenues [S7][S16]. This multi-revenue model supports unit economics resilience against fare volatility. Pricing power is supported by the brand’s vast route system spanning about 235 airports and its established operating bases at roughly 95 European airports, enabling optimized slot utilization and multiplier effects on load factors.

Cost discipline remains central to Ryanair’s model with operating expenses around 85% of total revenues in FY26 versus nearly 89% in FY25—a positive margin trend despite inflationary pressures [S7][S16]. Fuel costs consumed about 41% of operating expenses but per-passenger fuel costs remained stable year-over-year due to hedging strategies and newer aircraft offsetting higher flight activity and carbon charges [S16][S23]. Staff expenses rose modestly but benefited from fleet-driven efficiencies. Maintenance escalated slightly owing to higher utilization rates and aging legacy assets.

Risk management is further supported through Ryanair’s comprehensive insurance framework including third-party liability coverage backed in part by its own captive insurance subsidiary based in Malta. This entity underwrites portions of aviation-related risks while reinsuring residual exposure via global aviation markets—mitigating potential catastrophic losses related to accidents or geopolitical hazards like terrorism [S1].

Industry Structure & Competitive Position

The European airline industry is characterized by high fixed costs with intense pricing competition especially within the LCC segment where Ryanair competes alongside peers such as easyJet and Wizz Air. These competitors vie primarily on cost leadership achieved through high aircraft utilization rates typically exceeding daily averages of around 11 flight hours per plane (Ryanair targets similar or better metrics), minimal frills service offerings, direct digital distribution channels minimizing travel agent commissions, and aggressive ancillary revenue initiatives.

Ryanair's significant scale—with over double the passenger volumes of many regional LCC competitors—and broad geographic footprint affords it economies unavailable to smaller operators. Its large owned-fleet base reduces dependency on volatile leasing markets compared to peers reliant primarily on leased aircraft stock.[F1] The company’s early adoption of the Boeing Gamechanger series provides fuel efficiency advantages critical amid volatile jet fuel markets.

Regulatory compliance complexity is nontrivial given EU environmental mandates including sustainable aviation fuel (SAF) requirements aiming at net zero carbon emissions by mid-century, along with noise restrictions at major hubs which constrain scheduling freedom. Ryanair actively invests in SAF usage piloting initiatives aligning operational sustainability with cost containment objectives.[S1]

Growth Drivers

Passenger traffic growth remains structurally driven by expanding intra-European leisure travel demand supplemented by business trip recoveries post-pandemic disruptions [S1]. Ryanair's historic increase from roughly five million passengers in FY99 to over two hundred million in FY26 exemplifies robust secular demand trends coupled with network densification via new routes or added frequencies on profitable corridors.

Fleet modernization will underpin future cost efficiencies as the delivery ramp-up of up to three hundred Boeing MAX-10 jets over several years promises lower fuel consumption—critical as fuel accounts for approximately two-fifths of operating costs.[S1][S19] This transition is anticipated to support competitive pricing even amid rising carbon pricing pressures.

Ancillary revenues remain a key layer boosting average revenue per passenger through targeted product offerings like priority boarding or baggage add-ons that command premium pricing yet incur limited incremental costs [S7][S16]

Digital transformation initiatives aimed at enhancing direct online bookings reduce distribution fees incurred when flights are sold via third-party travel agencies. Maintaining strong customer loyalty through consistent low fares combined with sustainable commitments could enhance brand strength relative to full-service legacy carriers struggling with higher cost bases.

Risks & Watchpoints

Fuel price volatility constitutes a perennial risk impacting margins unpredictably despite hedging; shortages or spikes due to geopolitical crises can exacerbate costs unexpectedly.[S5][S21] Strict environmental regulations mandating SAF blending may also increase operating expenses unless cost-effective supply chains scale adequately.

Regulatory litigation risk crystallized recently when Italy’s competition authority fined Ryanair €256 million alleging abuse of dominant market position regarding relationships with online travel agents between April 2023–April 2025; management disputes these claims vigorously with appeals underway that could span years.[S5] Ongoing scrutiny over pricing algorithms or distribution practices could invite further fines or corrective action curtailing commercial flexibility.

Labor relations represented occasional challenges historically; pay rises have incrementally increased personnel expenses albeit offset partially via productivity gains linked with additional newer aircraft utilization [S16]

Lastly, operational disruption risks—from extreme weather events impacting flight schedules through air traffic control strikes prevalent across Europe—can erode revenue during peak seasons thus pressuring quarterly earnings variability [S9]

What To Watch Next

Key upcoming milestones include monitoring capacity buildup as new MAX-10 deliveries commence more broadly starting calendar year-end frameworks into early next decade towards the target ~800-aircraft fleet by FY34.[S19] Traffic trends reported monthly remain crucial indicators reflecting short-term demand resilience amid macroeconomic uncertainty.[N6]

Regulatory developments related to competition law appeals in Italy represent critical overhangs potentially influencing risk premiums attached to Ryanair shares.[S5] Additional legal outcomes regarding EU261 passenger compensations may impact future liabilities.

Fuel market dynamics including jet fuel price fluctuations combined with SAF mandate implementations require attentive observation given their outsized influence on CASK (cost per available seat kilometer).[N8]

Operational KPIs like load factor stabilization above break-even thresholds (~80%) during off-peak quarters will signal pricing strength amid rising airport charges or staff cost inflation [S7]

Financial Profile Commentary

Debt maturities are manageable with repayments completed recently on certain unsecured Eurobonds complemented by undrawn credit facilities amounting close to €1 billion providing flexible liquidity buffers ahead of accelerated delivery schedules on firm aircraft orders valued around multiple billions euros under long-term Boeing agreements [S11][S12]

In summary, Ryanair’s financial posture supports strategic expansion but necessitates careful monitoring of external shocks including funding environment shifts or regulatory penalties which could stress margins or cash flow conversion temporarily.

This analysis synthesizes publicly filed disclosures without offering investment advice. Operational insights derive strictly from verified regulatory reports excluding unsubstantiated forecasts or opinions beyond documented evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments