Rise Gold Corp. Advances Permitting and Legal Strategy at Idaho-Maryland Mine

Recent land sales, judicial rulings on environmental litigation, and debt restructuring define Rise Gold's critical development phase.

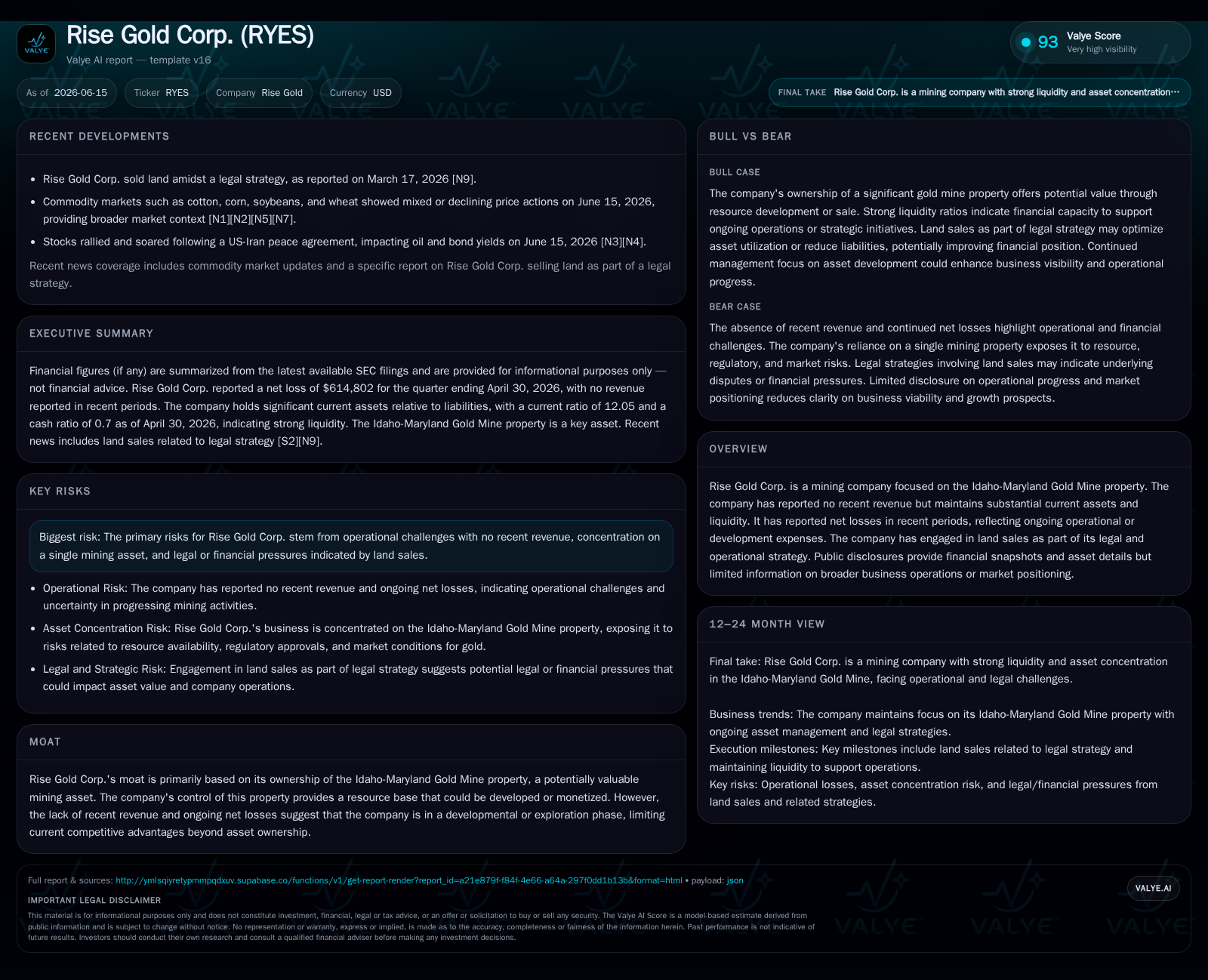

Rise Gold Corp.’s latest 10-Q filing for Q3 2026 reveals a completed $2.5 million land sale, a key adverse court ruling on Clean Water Act violations against its subsidiary, and debt refinancing maneuvers aimed at preserving liquidity. The company remains in the exploration and permitting stage focused on its Idaho-Maryland Gold Mine property with no current revenue, confronting operational hurdles in environmental compliance and legal challenges. Its business model centers on asset ownership leveraged through option agreements, monetization of non-core parcels, and cautious capital management amid ongoing losses.

Latest Operating Update: Land Sale Completion and Legal Judgments

In its latest quarter ending April 30, 2026, Rise Gold Corp. closed a significant non-core land sale covering approximately 50 acres for $2.5 million [S2]. Half of this amount was paid at closing on May 27, 2025, with the balance payable by May 27, 2027, alongside monthly installments made pre-closing credited against the purchase price. Post-closing payments carry a fixed annual interest rate of 5%, evidencing a monetization strategy for surface parcels outside core mineral rights that finances ongoing operational needs and legal costs

Concurrent with this transaction is a pivotal legal development: the U.S. District Court for Eastern California granted summary judgment in May 2026 favoring Community Environmental Advocates (CEA) in a suit alleging that Rise Grass Valley Inc., a wholly owned subsidiary operating the Idaho-Maryland property, discharged pollutants including arsenic into local waterways without necessary permits under the Clean Water Act (CWA). This ruling confirms regulatory scrutiny over historic mine pollution impacts and imposes reputational as well as compliance risks at a critical juncture for project permitting [S3]. These developments frame a complex operating environment balancing asset monetization against mounting environmental liability concerns.

Business Model: Asset Ownership Amid Exploration Stage Challenges

Rise Gold’s business model is characteristic of junior stage mining companies focused almost exclusively on the acquisition and advancement of mineral properties rather than immediate operational revenue generation. The company holds a controlling interest in the Idaho-Maryland Gold Mine via an option agreement established in August 2016 requiring a total purchase price of $2 million, with an initial non-refundable deposit credited upon eventual option exercise [S2]. This property forms the bedrock of the company's asset base.

At this stage, Rise does not recognize mining production or sales; instead, expenditures are directed toward exploration drilling, resource definition exercises, permitting efforts, feasibility studies (still pending), legal actions defending mineral rights claims, and managing environmental obligations. Revenue generation currently relies on strategic sales of peripheral surface land parcels to fund these activities while preserving core mineral assets.

Key financial characteristics include persistent operating losses reflecting exploration outlays and legal defense costs without offsetting cash flows from mined metal sales [F1]. To sustain operations amid these net losses, Rise utilizes secured loans combined with equity-linked instruments such as share warrants to raise working capital and extend financial runway.

Competitive Context: Peer Group Overview in Junior Gold Mining Development

Within the junior gold exploration sector, Rise Gold aligns somewhat with peers like Hecla Mining Company or Coeur Mining Inc., which operate similarly sized projects often mired in permitting complexities before achieving production scale. Compared to mid-tier producers such as Barrick Gold or Newmont Corporation—who command multi-mine portfolios with extensive infrastructure—Rise’s single-asset profile underscores its relatively concentrated exposure to project risk.

Permitting delays and environmental litigation are common challenges for junior miners attempting to unlock resource value amid stringent regulatory environments. While larger peers benefit from diversified geographies and established cash flows cushioning such risks, smaller operators like Rise depend heavily on successful resolution of legal disputes and access tenure affirmations to advance into production phases.

Exploration and Development KPIs

Filings provide limited disclosure on specific ore grade metrics or detailed reserve estimates at this time but confirm that permitting efforts remain active alongside incremental exploration drilling consistent with early-stage development norms [S1], [S2].

The continued advancement towards feasibility studies is tied closely to resource expansion validation through drilling meterages completed—an essential KPI indicating inches gained on the path to defining economically mineable reserves. Such activities also influence environmental impact assessments pivotal for obtaining necessary regulatory approvals.

Capital expenditures during this phase primarily reflect exploratory CapEx rather than full-scale mine development investments. Margins cannot be assessed given the absence of production revenues.

Permitting Risks and Legal Challenges

A defining issue facing Rise is ongoing litigation concerning its vested right to mine at the Idaho-Maryland property juxtaposed against environmental regulations mandating permits for pollutant discharges under the CWA. In late 2023 through mid-2024 filings, Rise petitioned local county authorities asserting constitutionally protected mining rights without use permits—a claim denied by local government resolutions resulting in court filings challenging county decisions [S1], [S4].

Most recently, a federal district court ruling sided with community environmental groups holding that pollutant discharges lacked requisite permits—a blow complicating forthcoming permit applications. These overlapping regulatory and legal hurdles create material uncertainty regarding timelines and cost escalation risks necessary before full mine development can commence.

Environmental compliance requirements are notably stringent in California jurisdictions where historical mining legacies trigger complex tailings management protocols and remediation liabilities potentially inflating OpEx post-production.

Capital Structure & Financing Strategies

To finance its operations during this developmental phase devoid of operating cash flow, Rise has engaged in multiple secured loan arrangements accompanied by warrant issuances as equity sweeteners reflecting higher financing costs typical for junior miners.

The February 2023 renegotiated loan with Eridanus extended maturity to September 2024 while reducing interest rates temporarily from an onerous 25% per annum compounding monthly to more manageable terms at 15% [S2]. Concurrently issued warrants augment potential dilution though provide near-term capital relief

An October 2024 four-year secured $500,000 loan from Myrmikan Gold Fund carries similar interest pricing at 15% per annum with accrued amounts payable at maturity alongside nearly three million warrants exercisable over four years—indicating high cost of capital reflective of project-stage risk profile.

A revolving credit facility entered in February 2024 imposes monthly fee deferrals accruing compound interest also payable after several years. Collectively these arrangements underscore the delicate balance between maintaining liquidity sufficient to fund exploration/legal costs while minimizing excessive dilution or leverage risk ahead of commercial milestones.

Growth Drivers: Commodity Prices & Resource Expansion Potential

Though still in exploration mode without revenue or production forecasts disclosed, Rise’s potential upside fundamentally rests on commodity price dynamics—particularly gold which underpins project economics once reserves reach commercially viable thresholds.

Successful incremental expansion of indicated resource through continued drilling would enhance reserve confidence levels—a prerequisite for future feasibility studies raising valuation metrics. Technological improvements enabling improved recovery rates or processing efficiencies could further improve economic parameters but remain speculative absent current data.

Infrastructure improvements enabling better access or permitting clearance would materially impact cyclical timing advantages given gold price volatility historically influences junior miner investment appeal.

Risk Factors: Environmental Compliance & Litigation Uncertainty

Environmental issues are central risks following judicial affirmation of violations linked to pollutant discharges into local creeks related to historical mine workings exposing liability potential both financially and reputationally.

Loss of social license or community opposition might exacerbate delays potentially increasing operating costs through additional remediation mandates or permit refusals.

Legal battles over vested rights challenge business continuity assumptions fundamental to long-term planning while external regulatory changes may impose more stringent emissions targets complicating compliance strategies further.

Climate considerations around mine closure obligations or tailings remediation add latent long-term liabilities beyond immediate operational concerns.

What to Watch: Permit Decisions, Capital Raises & Exploration Milestones

Key milestones affecting near-term value include:

- Final determinations on Nevada County’s recognition (or continued denial) of vested mining rights affecting operational scope,

- Resolution outcomes from ongoing federal court litigation influencing environmental permit conditions,

- Success in securing additional financing rounds balancing dilution versus liquidity needs,

- Progression toward defined resource estimates through drilling meterages completed,

- Execution of any further land monetizations improving cash position. Monitoring these updates will clarify whether operational runway can be extended sufficiently for meaningful project advancement.

Financial Snapshot: Liquidity And Debt Refinancing Update

As of April 30, 2026, Rise Gold reported working capital surplus approximating $7.4 million supported by current assets around $8.1 million against liabilities close to $670K—translating into a robust current ratio exceeding 12x indicating strong short-term liquidity headroom [F1], [S2].

However, notable debt exists including renegotiated facilities with Eridanus Capital featuring deferred payments and adjusted interest rates plus secured loans from Myrmikan accompanied by warrant issuances increasing future equity claims [S2]

Ongoing net losses—over $3 million in nine months ended April 30—highlight the burn rate pressure typical during extended development phases requiring careful capital management lest dilution jeopardizes shareholder value before any production commences.

This analysis synthesizes publicly available SEC filings up to June 15, 2026—emphasizing factual disclosures without projecting unsubstantiated outcomes or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments