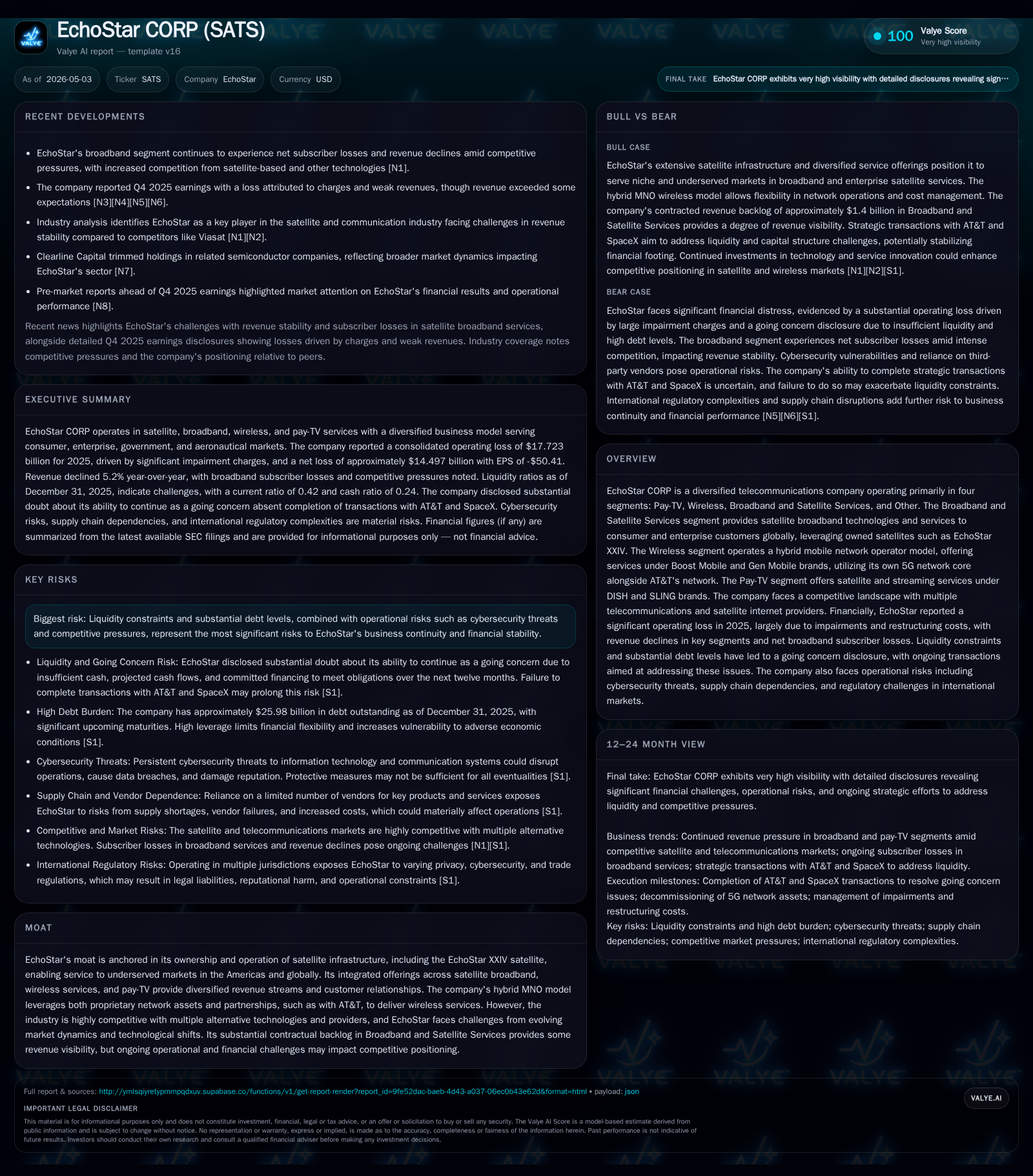

EchoStar’s 2026 Strategic Reset: Deleveraging and Spectrum Monetization Redefine Growth Path

EchoStar’s latest filings highlight a major debt restructuring and spectrum sale, reshaping its position in satellite broadband, pay-TV, and wireless industries.

In early 2026, EchoStar entered into a Restructuring Support Agreement that targets significant deleveraging by prepaying over $1.6 billion in high-cost debt, alongside advancing a landmark $19.6 billion spectrum sale deal with SpaceX. These transactions mark pivotal near-term operational and financial inflection points following a period of revenue declines and operating losses in the Broadband, Wireless, and Pay-TV segments. EchoStar operates an integrated multi-segment telecom model with satellite infrastructure ownership underpinning its competitive moat. The company faces both structural challenges from industry commoditization and cyclical pressures amid evolving wireless partnerships and regulatory scrutiny. Key growth drivers include expansion in underserved satellite broadband markets and monetization of spectrum assets, balanced against risks such as liquidity constraints and intense competition from alternative technologies.

Recent Operating Update and Strategic Transactions

EchoStar Corporation’s most consequential recent development stems from the March 19, 2026 filing disclosing the entry into a Restructuring Support Agreement (RSA) with an ad hoc debtholder group owning over 82% of debt issued by DISH DBS Corporation (DDBS) and affiliates [S3][S21]. The RSA initiates a prepayment without penalty of approximately $1.6 billion in high-interest term loans and preferred memberships related to DDBS subsidiaries—a decisive step towards reducing the company’s leverage.

This moves follows sustained financial pressure including a steep $17.7 billion operating loss for fiscal year-end 2025 driven by impairments and restructuring charges [F1][S1]. Concurrently, EchoStar amended its License Purchase Agreement with Space Exploration Technologies (SpaceX) pushing total consideration upward to approximately $19.6 billion from $17 billion initially announced [S15][S17]. This transaction schedules transfer of substantial AWS band spectrum licenses (1695–1710 MHz range) primarily compensated through SpaceX Class A common stock valued at $212 per share.

Completion timelines for this spectrum acquisition are targeted near late 2027 but remain contingent on multiple regulatory approvals including FCC and antitrust clearances [S25][S27]. The RSA aligns capital structuring flexibility enabling EchoStar to address outstanding debts linked to these spectrum assets and facilitates potential M&A optionality [S3].

Business Model Overview

EchoStar’s revenue generation scales across four principal segments:

- Pay-TV: Delivers satellite delivered pay-TV content principally through DISH Network’s legacy satellite platform alongside internet streaming services via Sling TV.

- Wireless: Operates under the Boost Mobile and Gen Mobile brands using a hybrid mobile network operator (MNO) structure where EchoStar controls the network core infrastructure while leasing radio access network elements mostly from AT&T.

- Broadband & Satellite Services: Provides consumer and enterprise customers worldwide with broadband connectivity relying on owned geostationary satellites such as the EchoStar XXIV. This segment targets coverage over rural and underserved regions where terrestrial networks lack presence.

- Other: Includes support services, emerging investments, satellite ground infrastructure management, and corporate functions.

Revenue mechanics are complex: pay-TV revenues derive mostly from subscriber fees within bundled packages dictating mix dynamics between traditional subscription pay-TV versus streaming offerings. Wireless top-line depends on SIM activations, average revenue per user (ARPU), wholesale data traffic volumes influenced by network usage agreements notably with AT&T’s RAN leasing terms [S16], while broadband revenues hinge on terminal equipment sales plus recurring service contracts backed by satellite capacity leases.

However, competitive headwinds are pronounced:

- Satellite internet rivals such as Viasat and SpaceX Starlink pursue high-capacity LEO constellations offering lower latency alternatives disrupting traditional GEO-based operations [N1].

- Terrestrial 5G rollout accelerates competitive capacity especially in urban/suburban markets constraining cellular-based MVNO growth prospects.

- Streaming services erode legacy pay-TV subscriber bases requiring adaptation toward bundled ecosystem offerings.

These dynamics demand continuous investment balancing innovation against prudent cost controls amid volatile consumer demand patterns.

Growth Drivers

Despite challenges EchoStar showcases structural avenues for expansion:

- Satellite Broadband Expansion: Leveraging owned orbital assets like EchoStar XXIV offers scalable broadband connectivity addressing global digital divides especially in Latin America, remote US regions, and developing countries where fixed infrastructure lags.

- Spectrum Asset Sales: The ongoing $19.6 billion deal unlocking AWS spectrum licenses provides immediate liquidity inflows to reduce leverage while mapping strategic refocusing toward core operational excellence beyond asset holdings.

- Wireless Network Evolution: Transitioning from reliance on wholesale RAN elements toward deployment of proprietary standalone 5G core networks enhances service differentiation potential over time [S16].

- Cross-Segment Synergies: Integration across Pay-TV content delivery combined with hybrid wireless bundles may generate incremental ARPU through multi-service crossover targeting younger digital-native demographics.

Each driver depends on Execution Excellence markers such as successful regulatory navigation for spectrum transfers; effective capital redeployment post-deleveraging; renewal/expansion of long-term customer contracts in broadband; achieving milestones in network modernization efforts; and managing churn trends in pay-TV subscribers effectively.

Risks & Constraints

Primary watchpoints include:

- Leverage & Liquidity Constraints: As of December 31, 2025, EchoStar reported net debt of approximately $24.47 billion against cash and equivalents of about $1.88 billion, resulting in a current ratio of 0.42, indicating limited short-term liquidity and constrained flexibility for opportunistic investments or adverse shocks without external financing or asset sales [F1].

- Regulatory Dependencies: Successful closure of spectrum sales hinges on multi-year FCC approvals subject to national security reviews and antitrust considerations introducing timing & conditionality uncertainties.

- Competitive Pressure & Technological Shifts: Rapid advancements in terrestrial wireless technologies, LEO satellite deployments challenging GEO incumbents, evolving consumer video consumption habits putting pay-TV under secular pressure induce heightened competition affecting pricing power.

- Cybersecurity & Operational Risks: Complex digital infrastructure spanning network cores exposes EchoStar platforms to cyber threats potentially resulting in service disruptions or liability exposures documented historically among peers.

What to Watch Next

Key developments to monitor over coming quarters involve:

- Completion status of the proposed Spectrum Acquisition Closing scheduled around November 2027 including any extensions invoked due to pending regulator decisions [S25][S27].

- Execution progress on the RSA’s debt prepayment obligations with perspectives published during quarterly results highlighting leverage reduction effectiveness [S3][S21].

- Metrics around subscriber additions/churn rates within the Pay-TV segment tracking success against cord-cutting trends plus improvements or deterioration in Sling TV performance signaling streaming traction.

- Wireless segment investments aimed at shifting DISH networks toward standalone operation including milestone deployments of billing/provisioning software upgrades discussed under Network Services Agreement amendments extending through end of 2031 [S16].

- Revenue backlog or contract renewals within Broadband & Satellite Services indicative of continued expansion into underserved territories sustaining medium-term growth aspirations.

Financial Profile Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1.88bn | |

| 2025-12-31 | ||

| Total debt | $26.35bn | |

| 2025-12-31 | ||

| Net debt | $24.47bn | |

| 2025-12-31 | ||

| Current assets | $5.13bn | |

| 2025-12-31 | ||

| Current liabilities | $12.36bn | |

| 2025-12-31 | ||

| Current ratio | 0.42x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

FY 2025 |

(Evidence: [F1])

This heavily leveraged profile underscores management’s motivation behind ongoing deleveraging initiatives crucial for sustaining operational continuity amidst capital-intensive satellite fleet upkeep, wireless network evolution costs, and competitive market pressures.

EchoStar's trajectory is emblematic of mature telecom incumbents navigating disruptive technological waves while unlocking value trapped within substantial infrastructure assets amid shifting consumption patterns. Success hinges critically on stringent execution against complex debt restructuring roadmaps paired with innovative leveraging of spectrum equity holdings fueling next-generation connectivity solutions focused on global reach beyond conventional metropolitan-centric models.

This analysis is developed solely from publicly available SEC filings dated November 6, 2025 through March 19, 2026 plus curated news references published through early May 2026. It is intended for informational purposes only without making investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments