Splash Beverage Group Advances Brand Distribution Despite Liquidity Pressures

The company reported modest revenue growth linked to expanded distribution but faces acute liquidity challenges amid leadership changes.

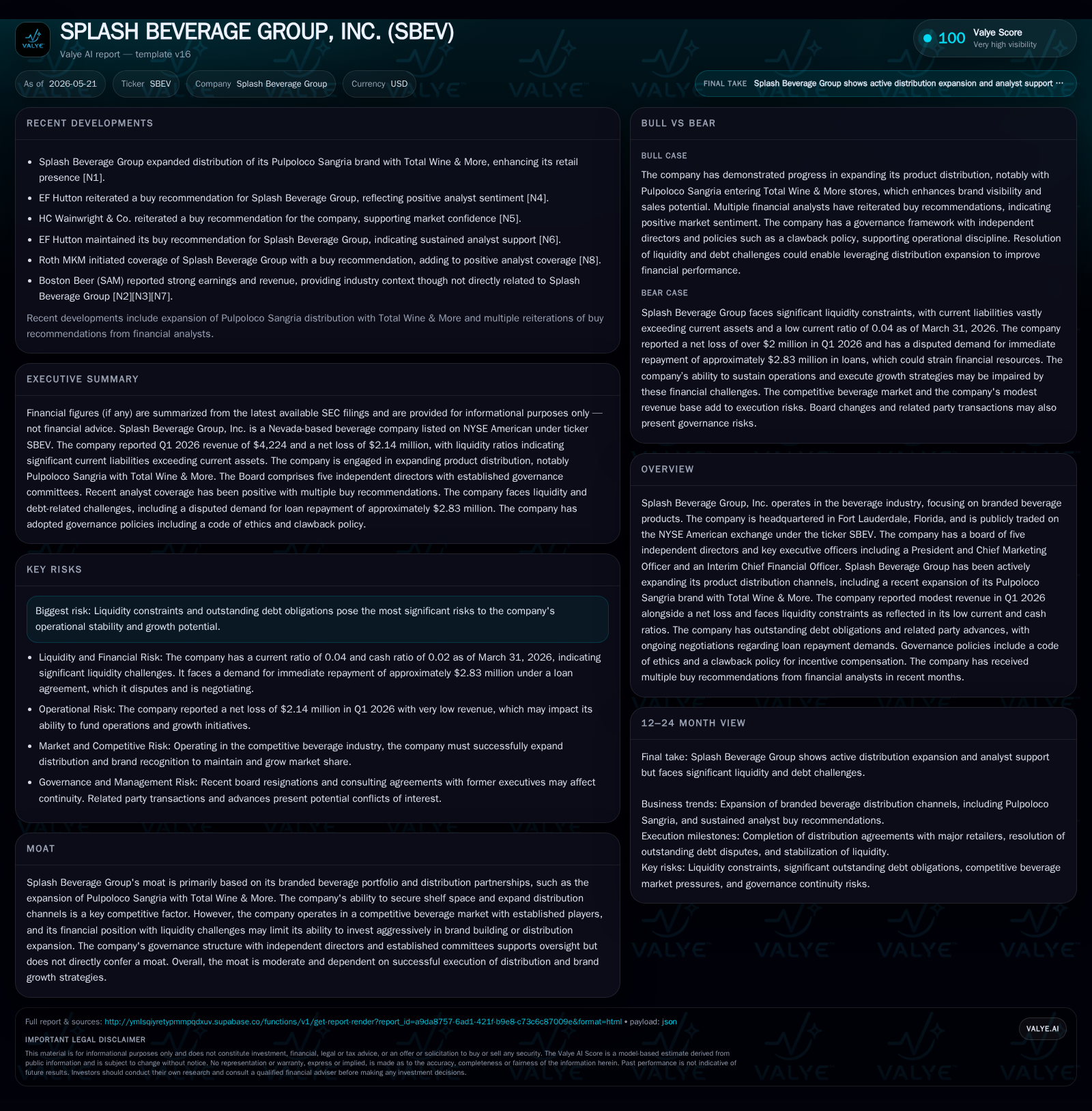

Splash Beverage Group's latest quarterly report highlights continued modest revenue of approximately $73,000 alongside a significant net loss and extremely low current ratio around 0.04, underscoring severe liquidity constraints. Despite these financial pressures, Splash is advancing its branded beverage portfolio, notably expanding its Pulpoloco Sangria distribution with Total Wine & More. The recent appointment of Brady Cobb as Interim CEO signals potential strategic shifts poised to strengthen brand presence in regulated wellness markets. However, the company’s capital structure stresses and debt obligations remain critical risk factors that may limit near-term growth and operational flexibility.

Recent Quarterly Operating Update Highlights

In its May 2026 Form 10-Q filing [S2], Splash Beverage Group disclosed a Q1 revenue figure of approximately $73,066 [F1], reflecting a continuing pattern of modest top-line scale. The company sustained a significant net loss consistent with prior periods—operating income for the trailing period remained deeply negative at more than $14 million [F1], underscoring ongoing cash burn challenges. Liquid assets stood at $381,195 as of March 31, 2026 [F1], starkly outweighed by $16.97 million in current liabilities [F1].

Complementing this financial snapshot was the announcement of Brady Cobb’s appointment as Interim Chief Executive Officer effective May 9, 2026 [S3]. Mr. Cobb’s background spans public and private enterprises primarily in emerging cannabinoid-regulated markets coupled with legal/regulatory expertise and brand development [S3]. His accession suggests a strategic pivot or intensified operational focus coinciding with the company’s pressing need for capital management and growth execution.

Business Model and Branded Beverage Portfolio

Splash Beverage Group generates revenues principally through branded ready-to-drink (RTD) beverages marketed under proprietary labels such as Pulpoloco Sangria [S1], which has recently secured enhanced distribution agreements including placement within over 350 Total Wine & More retail locations nationwide. Revenue mechanics depend on securing shelf space via distribution partnerships rather than manufacturing scale given that production is outsourced or contracted [S1]. Customers—retailers like Total Wine & More—purchase inventory wholesale, pricing being influenced by a combination of fixed contracts and promotional volume-based incentives.

Brand equity within the RTD segment hinges on curated product appeal aligned with consumer trends toward flavored alcoholic beverages—as well as emerging categories blending cannabis or wellness components. Limited production ownership reduces fixed asset burdens yet constrains control over supply chain cost efficiency. The company’s ability to increase consumer awareness amidst crowded brand shelves depends largely on incremental shelf penetration deals and marketing investments, which are constrained by weak liquidity.

Industry Dynamics and Competitive Positioning

Operating within a fragmented yet intensely competitive beverage landscape dominated by multinationals and aggressive challenger brands, Splash’s competitive leverages lie principally in securing distribution partnerships rather than scale economies or regulatory barriers. The procurement/supplier side remains exposed to volatility given lack of vertical integration while the retail wholesale customer base wields significant buying power exerting pricing pressure.

Switching costs for retailers are low given interchangeable SKUs across numerous brands competing for finite shelf space. Hence differentiation rests on brand curative efforts and targeted regional distribution agreements. Splash’s moat appears moderate; it lacks substantial capital-backed scale or proprietary technology but gains some insulation through established retail partnerships such as with Total Wine & More.

Growth Drivers: Distribution Expansion and Brand Building

Key near-term growth drivers center on further scaling retail footprint of flagship products like Pulpoloco Sangria through strategic expansions, notably ongoing rollouts in major store chains including Total Wine & More [S3]. Marketing initiatives under new leadership aim to capitalize on rising consumer preferences for flavored and possibly cannabinoid-infused beverages aligning with Cobb's regulatory market experience.

The recently announced merger talks with Medterra CBD—a prominent federally compliant cannabinoid wellness operator serving over two million domestic/international customers—signify a potential growth avenue into emerging THC/CBD infused beverage markets contingent on shareholder approvals and successful capital raises [S16]. Expanding into cannabinoid beverages could tap into structural demand growth insulated somewhat from traditional alcoholic beverage cyclicality.

Execution capability in retail channel expansion under limited capital remains pivotal given tight cash reserves impacting promotional spend and supply volume ramp.

Risks and Constraints: Liquidity and Debt Obligations

While reported total debt is nominal ($5,216 recorded end 2019) relative to liabilities [F1], related party advances nearing $0.4 million bear interest charges adding financial strain [S19]. The company faces demands from lenders including Knightsbridge Funding LLC enclosing claims exceeding $2.8 million as of March 2026 plus accrued interest—a dispute that has escalated into formal legal negotiations signaling precarious credit standing [S22].

The company's ability to invest adequately in marketing or increased inventory deployment is similarly constrained.

Leadership Transition and Strategic Implications

Brady Cobb’s elevation as Interim CEO intertwines operational leadership with strategic repositioning towards regulated cannabinoid wellness sectors—a field where he has built extensive legal, lobbying, regulatory compliance, brand creation, and capital markets expertise across cannabis/wellness/consumer packaged goods platforms [S3]. His role signals management's intent to bridge existing beverage operations with potential high-growth adjacent categories leveraging forthcoming Medterra merger synergies.

Board adjustments during April 2026 saw resignations from two directors including former CEO Robert Nistico accompanied by consultancy agreements aimed at stabilizing governance while reducing direct management involvement [S27]. Governance structure improvements emphasize independent oversight enhancing disciplined turnaround execution.

Cobb’s experience may prove vital navigating complex regulatory frameworks governing cannabinoid products rollout while optimizing brand curation strategies.

Next Milestones to Monitor

Attention centers on multiple upcoming catalysts: timely closure of the Medterra CBD merger remains critical both for expanding product lines towards cannabinoids and enhancing shareholders’ equity to regain NYSE American compliance following receipt of a delisting notice over equity deficits [S10]. Meeting May-end deadlines for submission of compliance plans to NYSE will indicate corporate strategic direction commitment.

Additional focus lies on progression of loan repayment negotiations amidst disputations with lenders [S22], along with effective ramping of Pulpoloco Sangria retail distribution during upcoming quarters evidencing execution strength under new leadership.

Management commentary around liquidity management plans, brand investment roadmap post-merger integration phases, and operational expense controls will be key to gauge trajectory towards stabilization.

Financial Summary and Liquidity Overview

Despite nominal reported direct debt balances (~$5K) per latest available figures dated December 2019 [F1], intangible liabilities balloon through accrued interest-bearing related party loans ($400K range) combined with substantial current liabilities nearing $17 million framed against current assets of approximately $0.7 million produce a significant liquidity gap fundamental to near-term survival challenges [F1], [S19], [S22]. Cash reserves approximating $381K provide limited buffer in light of heavy operating losses surpassing $25 million net annually indicating ongoing capital erosion without meaningful top-line growth acceleration or refinancing success [F1].

The company's financial profile poses immediate hurdles for re-investment in marketing or further expanding distribution footprint absent successful merger close or additional equity injections within coming months.

This report synthesizes public disclosures filed through May 20, 2026. All analysis is grounded strictly on cited evidence without speculative inference beyond documented facts. This document does not constitute investment advice or research views.

Financial position in context

As of 2026-03-31, companyfacts shows $381,195 in cash and equivalents [F1]. Current assets of $708,848 and current liabilities of $16,972,378 imply a current ratio near 0.04x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments