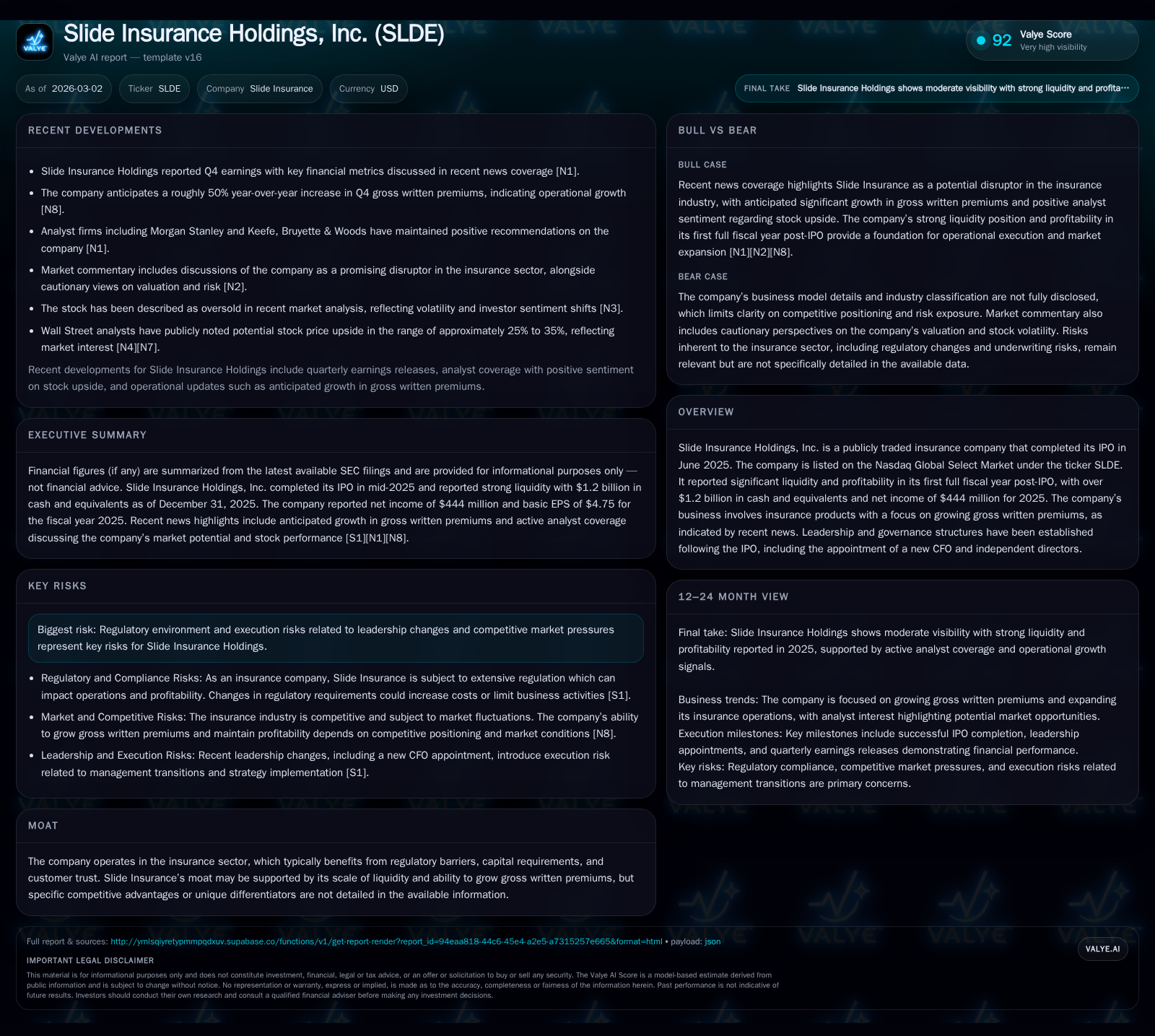

Slide Insurance’s Capital Strength and Leadership Changes Set Stage for Growth Trajectory

The company’s strong liquidity and governance overhaul following its 2025 IPO underpin a promising yet cautious outlook for premium-driven expansion.

Slide Insurance Holdings, after completing its IPO in mid-2025, reported an impressive $1.08 billion in revenue and $444 million in net income for its first full fiscal year as a public company, backed by over $1.2 billion in cash and equivalents. Growth has been fueled primarily by expanding gross written premiums, though the company faces regulatory scrutiny and market competition risks amid recent leadership restructuring. Future progress hinges on execution against strategic premium growth objectives and prudent capital allocation while navigating insurance-specific regulatory capital requirements.

IPO Catalyzed Leap: Slide’s First Fiscal Year Performance

Slide Insurance Holdings launched as a public entity via Nasdaq Global Select Market listing under ticker SLDE with its IPO closing on June 20, 2025[S16]. The offering generated gross proceeds of approximately $283 million before deducting underwriting fees[S16]. This capital injection underpinned Slide's transition into a publicly reporting company structure.

For the full fiscal year ended December 31, 2025, Slide Insurance posted total revenue of $1.08 billion alongside net income of $444 million[F1]. While no prior full-year public comparators exist due to the company’s recent market debut, this level of profitability underscores a significant inflection point driven by the IPO capital.[N1] Liquidity remained ample with cash and equivalents totaling nearly $1.2 billion at year-end, which positions Slide well to meet near-term operational and strategic investment needs.[F1]

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Gross Written Premium Growth as the Revenue Engine

Central to Slide Insurance’s business model is the aggressive expansion of gross written premiums — the total value of insurance contracts written before deductions for reinsurance.[N1][N2][S8] This metric forms the backbone of underwriting results and top-line growth within insurance companies. By emphasizing premium growth, Slide aims to scale its insurance footprint rapidly.

Recent disclosures suggest successful execution in increasing gross written premiums as part of their organic growth plan.[N1] This is consistent with sector practice where expanding premium volumes while managing underwriting risk distinguishes profitable insurers from peers. The company's management highlights this focus as key to sustaining momentum post-IPO.[N2]

Leadership and Governance Renewal Post-IPO

Following its public listing, Slide Insurance restructured several key leadership roles to enhance corporate governance and execution capabilities[N1][S14]. Notably, an experienced finance executive, Andy Omiridis—formerly with Amerisafe and Kemper Corporation—was appointed Chief Financial Officer effective December 1, 2025.[S22][S23]

Alongside leadership transition, the Board incorporated independent directors Andrew Wright and Beth W. Bruce who assume roles across Audit, Compensation (with Wright chairing), and Governance Committees.[S14] These appointments signal strengthened oversight consistent with public company standards that aim to mitigate execution risks flagged by investors.

Capital Allocation and Cash Flow Robustness Following Public Listing

The sizeable cash balance of over $1.2 billion combined with robust free cash flow generation ($795 million calculated as operating cash flow minus capex) illustrates strong liquidity management during Slide's inaugural year[F1][S9][S11]. This liquidity buffer offers operational flexibility to fund premium growth initiatives or meet regulatory capital demands common among insurers.

No dividends or stock repurchases have been declared during this period,[S14] which aligns with prudent capital preservation strategies typical for newly public insurance firms focused on establishing scale before returning capital.

Evaluating Return on Equity and Shareholder Value Metrics

Slide achieved an approximately 40% return on equity by dividing net income over reported shareholders’ equity at year-end,[F1] a figure that suggests efficient use of invested capital. For context, insurance industry ROE metrics vary widely due to differing lines of business but generally range between high single digits to low twenties percentage points.

This outsized ROE reflects favorable earnings leverage possibly related to underwriting performance or investment income during the early-stage post-IPO phase.[F1] However, direct peer comparison is limited given the recency of Slide’s public data set.

Regulatory Hurdles and Market Risks in 2026

Slide Insurance discloses material risk factors tied to regulatory supervision including capital adequacy mandates enforced by state insurance commissions that restrict leverage effectively and require ongoing compliance monitoring[S4][S5][S7].

Additionally, intensifying market competition among insurance providers introduces pricing pressures that could compress underwriting margins. Litigation exposure is also referenced broadly as an inherent sector risk.[S4][S5]

Leadership turnover amplifies execution risks particularly given CFO replacement less than six months post-IPO,[S23] although new appointments appear aimed at stabilizing financial stewardship.

Outlook Insights: Growth Prospects and Execution Challenges Ahead

There is considerable market interest around whether Slide can sustain its growth trajectory beyond an IPO-fueled initial spurt.[N2][N3] Analysts highlight premium volume growth rates and underwriting discipline as critical metrics to monitor.

Absent explicit company guidance,[N1] future milestones will likely revolve around meeting quarterly premium ramp targets while maintaining strong loss ratios—a common barometer of profitability in property-casualty insurance.

Moreover, regulatory developments impacting capital sufficiency rules warrant ongoing vigilance given their potential influence on cost structures and product offerings.

This analysis draws exclusively on publicly available SEC filings [S#], companyfacts numeric disclosures [F1], and reputable market commentary [N#]. It does not constitute investment advice but rather aims to present a grounded perspective on Slide Insurance Holdings' recent performance and outlook within the constraints of disclosed data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments