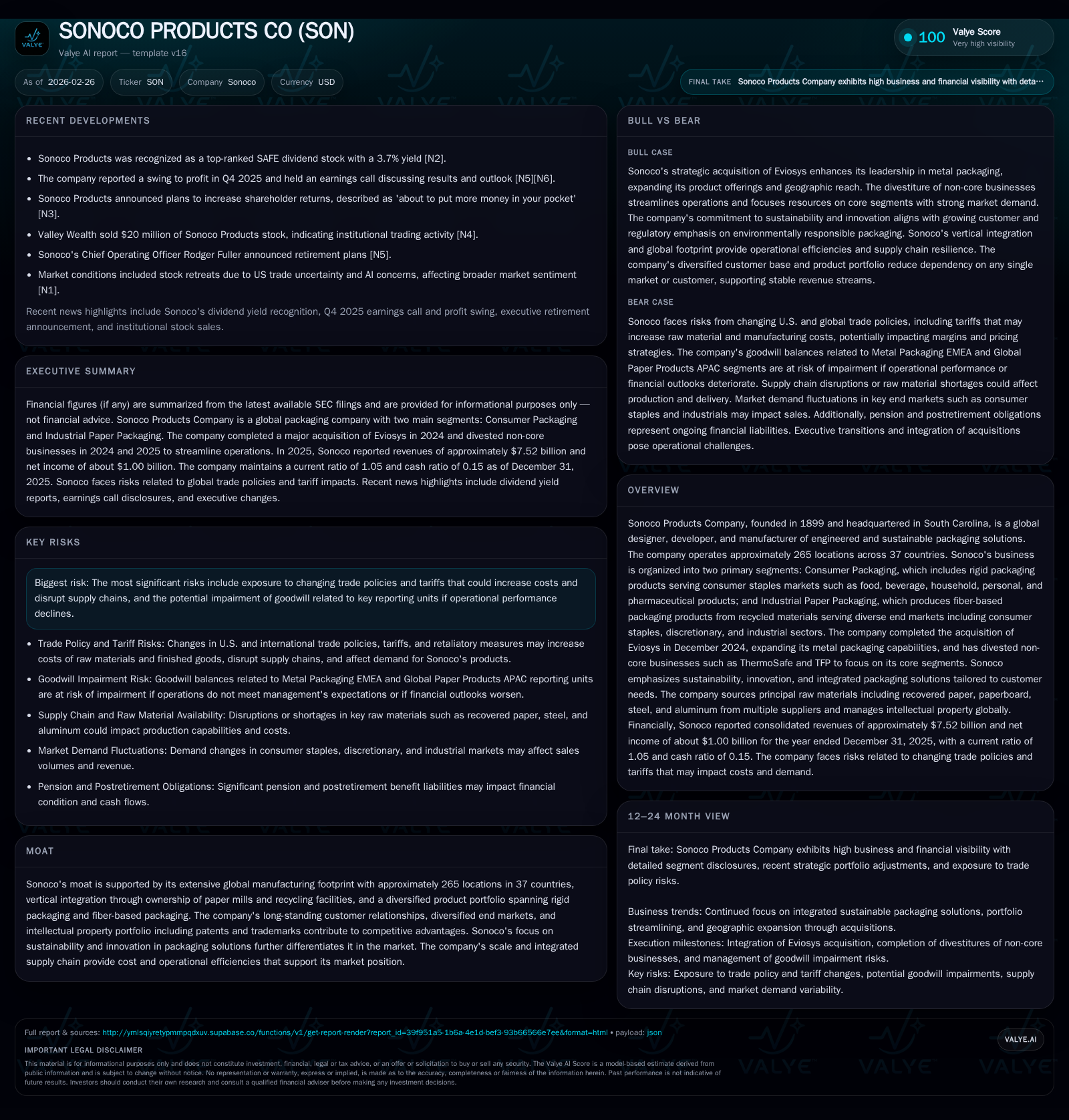

Sonoco Products Solidifies Market Leadership Through Strategic Portfolio Realignment and Sustainability

Sonoco’s transformative acquisition and divestiture strategy fuels record 2025 profitability and positions the company for sustainable growth.

Sonoco Products Company, with over a century-long heritage, achieved a dramatic financial turnaround in 2025 driven by its acquisition of Eviosys and the strategic divesture of non-core assets. The company reported a 451.5% revenue increase to $7.52 billion and net income surged from a loss in 2024 to $1.0 billion, reflecting operational improvements and portfolio realignment. With a fortified footprint in metal packaging and an expanding sustainable product platform, Sonoco is navigating growth opportunities while addressing risks such as goodwill impairment sensitivity and geopolitical pressures.

A Century-Old Legacy Meets Strategic Renewal: Overview of Sonoco's Evolution

Founded in 1899 in South Carolina as Southern Novelty Company, Sonoco Products Company has evolved from a niche paper cone manufacturer into a global packaging powerhouse with a footprint spanning roughly 265 locations in 37 countries [S1]. Its mission "Better Packaging. Better Life." underscores a commitment to sustainability, innovation, and tailored packaging solutions that extend beyond functionality to brand engagement. The company's strategic pivot crystallized with its December 2024 acquisition of Eviosys, Europe's foremost metal food cans, ends, and closures manufacturer, acquired for approximately $3.8 billion [S1]. This deal marked the largest in Sonoco’s history, substantially boosting its metal packaging expertise within the Consumer Packaging segment while signaling a deliberate move to streamline operations through selective divestitures like ThermoSafe [S1].

Historic Growth Performance: Earnings Surge Driven by Acquisitions and Operational Improvements

Sonoco's financial trajectory experienced a stark reversal between fiscal years 2024 and 2025. Full-year revenue soared to approximately $7.52 billion in 2025 from just $1.36 billion the prior year—a staggering year-over-year increase of about 451.5% as per reported figures [F1]. Operating income followed suit with a leap from $326.6 million to over $1 billion (up by an estimated 211.6%), while net income catapulted from a loss of $42.96 million to more than $1 billion (a remarkable swing exceeding 2400%) [F1].

This performance surge reflects multiple catalysts: integration gains from the Eviosys acquisition bolstered metal packaging revenues significantly, with segment operating profit nearly doubling following this portfolio expansion [S7][S18]. Operational efficiencies coupled with divestitures reduced overhead burden—ThermoSafe’s disposal removed non-core drag—while leveraging scale advantages across global manufacturing sites enhanced profitability.

Operating cash flow meanwhile declined modestly by about 17%, from approximately $833.8 million to $689.8 million year-over-year; this was accompanied by reduced capital expenditures down roughly 12.5% to $344 million as mature assets required less investment [F1]. Consequently, free cash flow remained positive at around $346 million, supporting capital returns despite acquisition-related financing.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 7.5 | 1003 | 690 | 1018 | +451.5% | +2434.8% |

| 2024 | 1.4 | -43 | 834 | 327 | -80.3% | -109.0% |

| 2023 | 6.9 | 475 | 883 | 716 | -6.7% | +1.8% |

| 2022 | 7.4 | 466 | 509 | 675 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 11 | 346 | 27.8 |

| 2024 | 9 | 441 | -1.9 |

| 2023 | 11 | 520 | 19.6 |

| 2022 | 5 | 180 | 22.6 |

Source: SEC companyfacts cache [F1].

Data per Sonoco filings indicates that Consumer Packaging drove much of this growth post-Eviosys acquisition—its share of consolidated sales increased to roughly 65% from under half in prior years—while Industrial Paper Packaging declined proportionally but still represented about 30% of total sales [S7][S18].

Portfolio Streamlining and Core Focus: Impact of Eviosys Acquisition and Divestitures

The Eviosys transaction redefined Sonoco's position in the metal packaging sphere, creating a more geographically integrated business spanning Europe, Middle East & Africa (EMEA), Americas, and Asia-Pacific markets under the Consumer Packaging umbrella [S1][S21]. Previously concentrated on rigid paper containers and select metal products like ends and closures, Sonoco acquired comprehensive capabilities for food cans and aerosol packaging that complement existing offerings [S18][S21].

Complementing this growth was the sale of ThermoSafe completed in November 2025, which concluded the company’s plan to shed less strategic business lines such as industrial insulated packaging [S1][S18]. Earlier disposals had similarly focused on sharpening core activities—to concentrate capital allocation on scalable consumer-facing rigid packaging alongside fiber-based paper products.

These moves collectively simplify the corporate architecture—reducing complexity—and enable focused investments into innovation pipelines emphasizing sustainability goals aligned across product lines [N1][S1].

Future Growth Outlook: Sustainability and Innovation in Metal and Fiber-Based Packaging

Sonoco has emphasized sustainability not only as an environmental imperative but also as a strategic differentiator enhancing customer value propositions across markets [S1][N1]. The company's vertically integrated fiber packaging business relies heavily on recycled materials processed through owned paper mills and recycling facilities worldwide—at around one-third capacity dedicated to internal consumption—contributing to circular economy credentials that increasingly resonate with brand partners.

In metal packaging via Eviosys incorporation, innovation revolves around lightweighting cans without compromising performance and improving recyclability metrics; these advances align with evolving regulatory frameworks targeting packaging waste reduction especially across EU jurisdictions [N1][S1].

While explicit forward guidance was limited in disclosures, management highlighted focus areas for margin improvement post-integration alongside continued R&D investment fostering new product development responsive to consumer trends toward sustainability-conscious brands [N1][S3].

Monitoring Key Milestones: Essential Indicators from Latest Earnings and Guidance

Following the Q4/Full Year 2025 earnings release on February 16, management underscored some integration achievements including operational synergies realized earlier than anticipated within the metal packaging franchise [N1][S3]. However, quantifiable full-year guidance metrics such as revenue or EBITDA projections were not provided explicitly.

Investors should monitor quarterly updates for signs of margin stabilization or expansion once Eviosys-related amortization charges normalize—alongside free cash flow consistency given ongoing capex discipline reflected already—and how geopolitical supply chain headwinds might affect cost structures amid fluctuating raw material prices [N1][N3].

Capital Allocation Review: Profitable Balance of Dividends, Buybacks, and Debt Management

Sonoco maintained disciplined capital deployment throughout its transformational year despite significant acquisition-related leverage increases; net long-term debt dropped from roughly $5 billion at end-2024 to under $3.8 billion by end-2025 due partly to proceeds from ThermoSafe divestiture used for debt repayment [F1][S15][S24].

The company continued returning capital via steady dividends representing about a 3.7% yield according to recent industry commentary; share repurchases were modest at nearly $11 million compared with historical levels but sustained alongside dividend stability supports shareholder value continuity [F1][N4][N5].

Operating cash flow generation remained solid albeit below prior year reflecting integration investments timing effects; capital expenditures decreased while free cash flow remained positive bolstering flexibility for future strategies [F1][S15]. Calculated approximate ROE stands near 27.8%, underscoring profitable equity utilization amid elevated asset base post-acquisition [F1].

Risks on the Horizon: Goodwill Impairment Sensitivity and Geopolitical Trade Pressures

Management explicitly identified the goodwill balances associated with Metal Packaging EMEA ($1.4 billion) and Global Paper Products APAC ($27 million) segments as sensitive to impairment risks if future operating performances fail expectations or discount rates shift unfavorably [S1][S2]. These units' fair values exceed carrying amounts narrowly (by low single-digit percentages), indicating relatively thin valuation cushions.

Trade policy volatility particularly affecting supply chains remains an overarching concern impacting cost inputs like steel/aluminum prices as well as logistics expenses given Sonoco’s multinational footprint [N3][S1]. While diversification mitigates concentration risk somewhat—the top five customers represent less than one-quarter of segment revenues—the company faces exposure to tariff changes or export restrictions that could pressure margins.

Sector-Specific Insights: Leveraging Vertical Integration in Paper Mills and Recycling Operations

Many industry participants struggle with raw material cost inflation exacerbated by supply disruptions; Sonoco's substantial vertical integration within fiber-based packaging - owning nineteen paper mills globally combined with sixteen recycling centers processing various recyclable materials - confers critical supply stability advantages absent at more asset-light competitors [S21][S6]. This seamless upstream control helps manage price variability while reinforcing sustainability narratives critical for client retention.

Moreover, continuous investment in recycling capacity allows efficient use of recovered paper inputs feeding core hermetic container production cycles—a strategy highly relevant amid increasing regulatory emphasis on recycled content standards internationally akin to EU mandates.

What Investors Should Watch Next: Cash Flow Trends, Margin Expansion, and Integration Progress

Key inflection points will revolve around achieving stable or improving operating margins once integration expenses wane fully alongside realizing projected synergy targets associated with Eviosys inclusion [N1][S3]. Monitoring operating cash flow movements relative to capex outlays will indicate free cash flow sustainability vital for funding dividends without accruing excessive leverage.

Additionally, signals concerning revenue diversification outside North America/Emerging Markets penetration may offer insights into long-term growth vectors tied to evolving consumer preferences towards sustainable packaging formats globally.

Disclaimer:

This analysis is based solely on information available through February 26, 2026, including SEC filings and verified news sources. It does not constitute investment advice or recommendations but seeks to provide an informed overview grounded strictly in reported data without speculative forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments