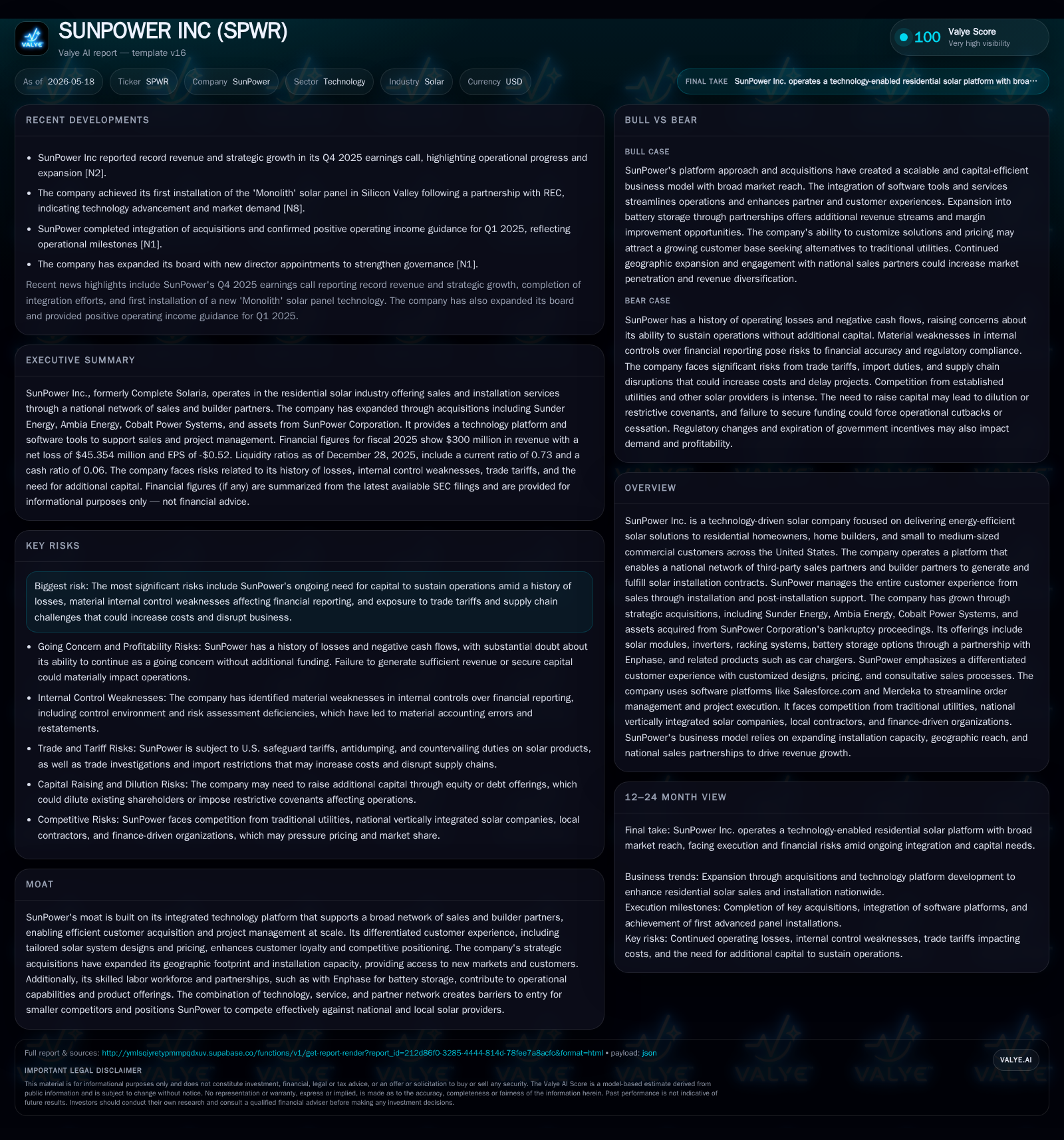

SunPower Inc. Advances National Solar Expansion Amid Operational and Financial Challenges

SunPower leverages strategic acquisitions and integrated technology platforms to scale residential solar offerings while addressing liquidity and reporting risks.

SunPower Inc.'s recent SEC filings highlight its ongoing efforts to expand its national footprint through acquisitions including Sunder Energy, Ambia Energy, and Cobalt Power Systems, integrated via a sophisticated platform that supports a broad network of sales and builder partners. The company is focused on cost control, capital raises including insider investments, and transitioning legacy software systems. Its partnership with Enphase aims to grow battery storage offerings, enhancing revenue potential amid rising energy costs. Despite liquidity pressures and required financial restatements, SunPower’s platform-driven model positions it for growth across new U.S. markets.

Recent Operating Developments

SunPower's December 19, 2025 quarterly report [S2] alongside its May 2026 event filing [S3] provide insight into the company's current operational landscape. Preliminary unaudited results for Q1 2026 indicate revenue approaching $300 million while operating losses persist due to growth investments and integration costs. The company is implementing headcount reductions and cost controls concurrently with capital raising initiatives, including a notable $5 million insider-funded SAFE issued in April 2026 [S25]. Additionally, SunPower is addressing material weaknesses in internal controls that necessitate restatements covering multiple quarters in 2025 [S9], with amended filings forthcoming.

These factors reflect immediate challenges related to financial reporting reliability and tight liquidity conditions evidenced by a current ratio of approximately 0.73 [F1]. Working capital pressures accompany scaling activities as the company seeks to stabilize cash flows while advancing strategic growth initiatives.

Business Model and Platform Integration

Operating under the rebranded SunPower Inc., formerly Complete Solaria, the company delivers residential solar solutions primarily to homeowners, home builders, and small-to-medium commercial clients through a nationwide network of third-party sales partners [S1],[S6]. This model leverages a technology-enabled platform that facilitates contract origination by sales agents while coordinating fulfillment via local builders or internal installation teams.

SunPower manages the entire customer lifecycle—from pre-qualification through site audits, permit acquisition, customized system design, installation management, to post-installation service—using proprietary software such as Merdeka (acquired with Sunder Energy) alongside Salesforce.com implementations set to replace legacy Albatross systems by late 2026 [S6]. This integrated platform streamlines workflows across diverse geographies enhancing operational efficiency.

The company’s revenue derives from contract volumes generated via partner networks weighted toward residential solar installations. Tailored pricing models enable competitive differentiation while offering diverse financing options [S11]. Expansion through acquisitions like Ambia Energy and Cobalt Power Systems increases installation capacity in targeted markets including the San Francisco Bay Area [S7], supporting scalable growth beyond simple product delivery.

Competitive Positioning

SunPower faces competition from traditional utilities supplying grid power; national vertically integrated solar providers with proprietary financing; small local installers operating with lower overhead; and sales aggregators focusing on contract generation [S18]. The company's competitive edge arises from its scale-enabled partner network supported by robust technology infrastructure that lowers customer acquisition costs.

Its consultative sales approach featuring customized home-specific solar designs and configurable pricing creates strong switching barriers in markets accustomed to volatile utility rates. This strategy empowers partner sales agents to align offers closely with homeowner needs fostering loyalty.

Moreover, SunPower’s ability to integrate acquisitions enables national partners to access standardized operational processes across previously unserved territories [S11]. The combination of differentiated customer experience and streamlined builder interactions distinguishes SunPower from transactional or localized competitors. Battery storage offerings via its partnership with Enphase further extend its market reach into emerging segments.

Growth Drivers

Strategic acquisitions underpin SunPower’s expansion: Sunder Energy adds a dedicated national sales force for efficient contract origination; Ambia Energy expands geographic installation capacity; Cobalt Power Systems enhances presence in competitive Bay Area markets [S7]. These acquisitions increase contract volumes while capturing downstream installation margins.

Synergies emerge from technology platforms that connect sales bookings directly to energization workflows, driving operational cost efficiencies over time. Battery storage integration through Enphase represents a key opportunity for margin enhancement cited in the April 2026 annual report [S1], enabling bundled product offerings that address rising energy costs and grid reliability concerns.

National-scale partners benefit from unified execution processes facilitating rapid market entry where SunPower had limited prior penetration [S11]. These combined factors support medium-term revenue growth driven by volume scaling complemented by higher-margin product suites.

Risks and Operational Challenges

Liquidity constraints are notable with a current ratio below one (0.73), reflecting working capital stress despite cash reserves of approximately $9.6 million versus substantial current liabilities near $155 million [F1]. Ongoing net losses exacerbate cash consumption necessitating capital raises such as the insider-backed SAFE transaction totaling $5 million [S25].

Financial reporting has been challenged by material internal control deficiencies leading to restatements for multiple fiscal quarters in 2025 [S9], elevating risks related to audit scrutiny and investor confidence.

Supply chain disruptions remain a concern due to tariffs impacting solar component pricing which could erode cost advantages or delay projects despite vendor diversification efforts [S22]

Cybersecurity risk management is overseen by the Audit Committee with executive leadership involvement ensuring incident response preparedness across the organization’s extensive partner ecosystem [S1].

Integration complexity following multiple acquisitions introduces execution risks particularly as legacy systems like Merdeka require phased convergence without disrupting service continuity.

Forward-Looking Considerations

Key near-term milestones include amended quarterly filings finalizing Q1 2026 results alongside retroactive restatements for earlier quarters clarifying revenue recognition trends [S3],[S8]. Progress on workforce rationalization coupled with cost containment will signal operational discipline post-acquisition expansion phases.

The scheduled sunset of Albatross order management software in favor of Salesforce-based processes by late 2026 marks an important technological transition enhancing scalability but carrying execution risk if disruptions occur unexpectedly [S6]

Sales pipeline development through national distribution partnerships offers visibility into revenue trajectories as these channels mature across new U.S. markets.

Growth in battery storage adoption tied to the Enphase alliance will serve as a critical KPI measuring margin uplift potential balanced against hardware costs amid evolving regulatory incentives such as those shaped by recent legislation affecting tax credits post-2025 [S22]

Financial Summary

Fiscal year-end data as of December 28, 2025 reports approximately $300 million in revenue offset by an operating loss of $26.9 million and net loss of $45.4 million reflecting elevated investment spending for growth initiatives [F1]. Cash balances stood near $9.6 million against total debt approximated at $108 million recorded September 2024 resulting in net debt around $98 million. This leverage profile underscores the importance of ongoing capital management amidst tightening liquidity conditions where current liabilities exceed current assets yielding a sub-1 current ratio (0.73) [F1].

These financial realities align with disclosed plans emphasizing capital raises alongside headcount reductions aimed at improving cash flow profiles while positioning SunPower for sustainable growth leveraging integration synergies and platform enhancements.

This analysis is based solely on publicly filed SEC disclosures through mid-2026 supplemented by companyfacts data; it does not constitute investment advice but provides contextual insight into SunPower Inc.’s evolving position within the U.S. residential solar market.

Financial position in context

As of 2025-12-28, companyfacts shows $10mm in cash and equivalents [F1]. Current assets of $113mm and current liabilities of $155mm imply a current ratio near 0.73x for 2025-12-28 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments